Life Insurance – Care for Your Loved Ones

The basis of life insurance began its formation in 1663 when English entrepreneur James Dodson collected all data on different London cemeteries, calculated the average age of deceased, their number per year and applied this statistics for calculation of insurance premium.

Since then insurance industry in Europe developed and blossomed. In 1994, the Single European Insurance Market has evolved, it unites 29 European countries: Austria, Belgium, the Great Britain, Hungary, Greece, Denmark, Ireland, Iceland, Spain, Italy, Cyprus, Latvia, Lithuania, Luxemburg, Malta, the Netherlands, Norway, Poland, Portugal, Slovakia, Slovenia, Turkey, Finland, Germany, France, the Czech Republic, Switzerland, Sweden, Estonia. Though insurance legislation in all countries has number of differences, it is based on the same principles, such as freedom to provide services and operation to the benefit of insured parties.

Life Insurance in Russia

Unlike Europe, life insurance in Russia has emerged quite recently, however, during formation of principles of insurance law experience and practice of European countries have been taken into the account and applied.

Life insurance is a set of actions of cooperation between the client (insured party) and the insurance company (insurer) aimed at financial and sometimes other security of life and health of an insured party or beneficiary in case of death of an insured party.

Among types of personal insurance life insurance stands out for the list of actions (insured perils) included into the insurance cover of the insurer and being the basis for insurance benefit, and also for the term of contract. Most types of life insurance are long-term.

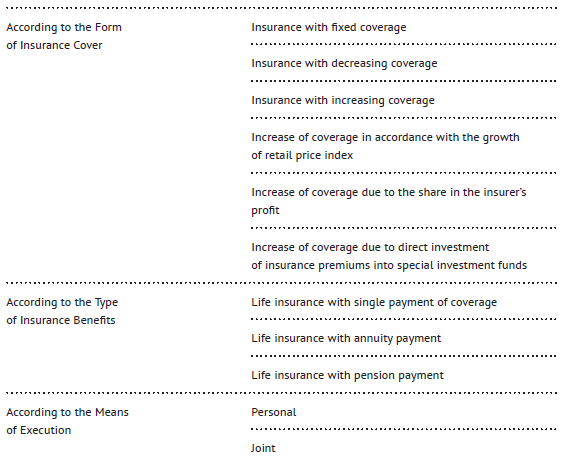

Life insurance may be classified according to the following types and criteria:

Life insurance embodies all those types of personal insurance where insurance coverage is assigned to the death of the insured party or his/her survival up to the certain moment of time.

Life insurance is executed as a contract, whereunder one of the parties, the insurer, undertakes liability to pay the specified insurance coverage, if within the term of insurance, the specified insured event takes place in the life of an insured party, provided he/she receives insurance premiums payable by the insurer. Life insurance contract is related to the life of a certain person, the insured party, thus, the insured party should be defined in the contract, so that it would be possible to estimate the probability of his/her death within the term of the contract.

There are personal life insurance contracts when the insured party and the policyholder constitute the same party, and third party life insurance contracts when the insured party and the policyholder are different parties, but the policyholder has insurance interest in the life of the insured party.

Third parties, beneficiary and the insured party, may be parties to insurance liabilities.

Beneficiary is an individual or legal entity, to which benefit the policyholder executed life insurance contract.

If life insurance contract does not expressly specify beneficiary, the contract shall be deemed executed to the benefit of the insured party. In case of death of the party insured under the contract where other beneficiary is not expressly specified, successors of the insured party shall be entitled to receive insurance coverage. In life insurance contract executed for the insurance of the insured party other than the policyholder beneficiary may be designated or amended only on the consent of the insured party or directly by the insured party himself/herself. In the absence of such consent, the contract may be invalidated at the suit of the insured party or in case of death of such party at the suit of his/her successors.

In accordance with Clause 956 of the Civil Code of the Russian Federation, the policyholder shall be entitled at own discretion to replace beneficiary specified in the insurance contract with the other party by notifying the insurer in written. If beneficiary fulfilled any liability under the insurance contract or made claims for insurance coverage against the insurer, his/her replacement is not possible.

The law does not lay obligations on the insurer for informing beneficiary on the insurance contract executed to his/her benefit. That’s why the policyholder shall himself/herself explain to beneficiary when, on what terms and under which documents beneficiary may receive insurance coverage.

In Russia, investment life insurance became recently popular.

Investment life insurance contract represents a combination of classic accumulative unit-linked life insurance in the form of investment assets, in terms of which the insurer may pay to the policyholder or other party, to which benefit life insurance contract is executed, part of investment income in addition to the insurance coverage as part of life insurance.

Under this contract, the policyholder’s insurance contributions are divided into two parts: one part constitutes secured coverage, which the policyholder or beneficiary receives in case of insured event, and the second part is invested by the insurance company into various investment products.

The ratio between two parts is not fixed. When the market grows, the insurance company increases the commercial part, which allows clients gain additional profit. When the market declines, most investments of clients evolve into conservatives of the stock market.

Unlike common accumulative life insurance, investment insurance stipulates possible additional proceeds not determined under the contract: if variation of prices and asset management policy prove to be relevant to the situation and investments become successful, there will be proceeds; if the situation develops adversely, the policyholder will receive only the amount specified in the contract.

Taxation and Special Status of Insurance Coverage

Under life insurance contract, in case of receipt of coverage related to the occurrence of the insured event, income shall be exempted of taxation: if under the terms of such contract insurance contributions are paid by the tax payer and (or) his/her family members and (or) close relatives in accordance with the Family Code of the Russian Federation, or if the amount of insurance coverage does not exceed the amount of paid insurance contributions plus the amount calculated by subsequent addition of products of sums of insurance contributions made from the day of insurance contract execution until the day of termination of each effective year of such voluntary life insurance contract (inclusive) and valid during the applicable year of annual average bank rate of the Central Bank of the Russian Federation. Otherwise, the difference between the said sums shall be recognized during determination of the tax base and shall be subject to withholding taxation Paragraph 1 of Clause 213 of the Tax Code of the Russian Federation.

Thus, in case of investment in the amount of 1,000 Rubles per month for a year, tax-exempt income shall equal 12,990 Rubles per year.

(10,000 Rub. х 12 months) + (10,000 Rub. х 8.25% х 12 months) = 129,900 Rubles.

In case of execution of life insurance contract for more than 5 years, the taxpayer shall also be entitled to receive social tax deduction in the amount of paid insurance contributions for a year within 120,000 Rubles Paragraph 4 of Clause 219 of the Tax Code of the Russian Federation.

In case of execution of insurance contract for 10 years with required insurance contribution in the amount of 10,000 Rubles per month, the policyholder shall be entitled to decrease the tax base for PIT annually by 120,000 Rubles receiving tax deduction in the amount of 15,600 Rubles. In case of receipt of insurance coverage upon termination of contract, the amount of tax-exempt income shall equal 1,299,000 Rubles.

Upon execution of life insurance contract, monetary funds paid as insurance contribution shall not be subject to seizure or custody, and also cannot be integrated into marital property in case of divorce because such monetary funds has actually been transferred to the insurance company, and the insured party’s or beneficiary’s right to dispose of the insurance coverage accrues only in case of occurrence of the insured event.

It is important to remember that if insurance contributions are paid by a legal entity for the benefit of an individual, tax exemptions shall not apply.

Execution of Documents

The list and procedures for submitting documents is defined under the insurance contract.

- In case of occurrence of an insured event, the following documents (common for all insured events) shall always be submitted:

- Application for coverage (in form certified by the department of insurance coverage and provided for completion by the employee of a branch or the head of the department of coverage of the Central Office);

- Insurance contract (copy, if the Contract remains valid);

- Identity documents (passport).

- In case of death of the Insured Party, the following documents shall also be required for submission:

- Notary certified copy of Death Certificate of the Insured Party (death certificate is given to relatives or interested parties. If beneficiary is not a relative, he/she needs to confirm his/her interest in receipt of death certificate by submitting to the civil registry office a copy of insurance contract);

- Medical report on the causes of death, autopsy results (if any);

- Certificate of the road traffic accident (if death occurred as a result of the road traffic accident).

- In case the Insured Party becomes disabled, the following documents shall also be submitted:

- Certified copy of certificate of the professional medical expert commission on the assessment of disability of the Insured Party;

- Documents confirming occurrence of an accident (if disability assessed as a result of accident).

- In case of accident involving the Insured Party, the following documents, which allow defining the amount of insurance coverage, shall be also submitted:

- Documents of a medical institution specifying consequences of the insured event for health and working ability of the Insured Party;

- Documents confirming the fact and circumstances of the accident issued by the official state authority (police, including the road police, fire service).

Other Articles on Topics