IP Box in Cyprus: Old Friends Are Best

Since December 2013, deoffshorization of Russian business has been one of the most popular tax topics. At the beginning of the previous year, the Ministry of Finance published a letter describing prevailing schemes of tax mitigation using advantages stipulated in agreements for double taxation. The Ministry of Finance paid special attention to the fact that in case of application of international agreements in the area of granting right for the use of tax reliefs (decrease of rates and exemptions) for certain types of income from sources in Russia, it should be estimated whether the party seeking tax reliefs (reduced rates and exemptions) specified in the agreement is the actual receiver (beneficiary owner) of the applicable income.

However, for a party to be recognized as the actual income receiver (beneficiary owner) not only legal grounds for the actual receipt of income are required, but this party should also be an actual beneficiary, it means a party, which actually benefits from the received income and determines its following economic benefit. At determining the actual income receiver (beneficiary owner), performed functions and accepted risks of an international organization seeking tax reliefs in accordance with international agreements for the avoidance of double taxation should also be taken into the account.

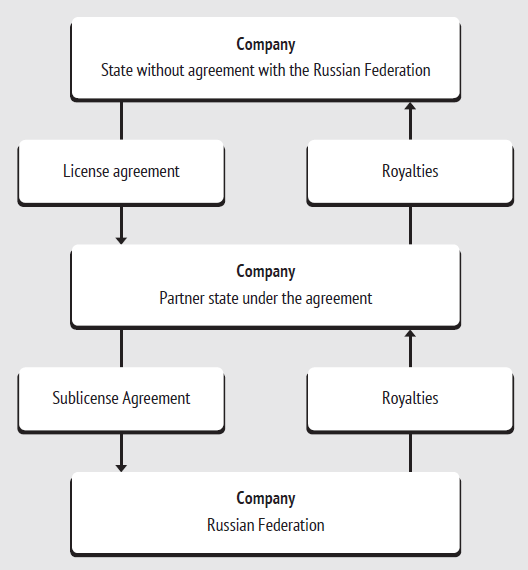

Tax reliefs (reduced rates and exemptions) in relation to payable income from the source in the Russian Federation are not applicable, if they are paid within transaction or series of transactions performed in such manner that a foreign party seeking tax reliefs as reduced rate on dividends, interest and royalties pays, directly or indirectly, all or almost all income (at any time and in any form) to the other party, which would not have had any tax reliefs (reduced rates and exemptions) under the applicable agreement for the avoidance of double taxation, if such income would have been paid directly to such party.

According to the Ministry of Finance, conduit transactions include without limitation the following:

Resident of the partner state under the agreement receiving income from copyright from sources in the Russian Federation under the sublicense agreement transfers all or almost all such income to a party, which is the resident of the state without the relevant agreement with the Russian Federation (or the state, with which the agreement stipulates less favorable taxation terms) under license agreement executed between the first mentioned foreign resident and this other resident of the third foreign state being the owner of exclusive rights for intellectual property asset1.

Thus, the risk of adverse consequences of the use of the abovementioned scheme within the structure of a company has significantly increased.

Such term as real substance is tightly related with the concept of actual income receiver. Among tax lawyers, this term is used in English and sometimes can be found as “priority of contents above form”. Generally, in an attempt to get maximum profit from the use of various schemes for tax mitigation most try to save on everything, including maintenance of a conduit company (intermediate company), which is used only for withdrawal of funds to an offshore company with minimum tax liabilities. Such companies rarely have office, staff, archive or assets held.

However, taking into the account recent trends in the national tax law, the Russian business will have to restructure its capital; otherwise, it might face serious consequences and not only penalties.

One of the most obvious solutions is execution of contract directly with the company holding assets, however, at first, it might seem that it is highly impractical because in such case either the right for the use of the agreement for the avoidance of double taxation will be lost, or it will be required to pay tax on profit from royalties at high rate within the jurisdiction, wherewith such agreement is executed. In such situation IP Box regime comes to help. This regime exists in several European countries and it allows significantly reducing the effective profit tax rate in relation to profit gained from rights for intellectual property.

European countries are known for their liberal attitude towards IT area, which is confirmed by application of so-called IP Box regime, which means granting partial exemption of profit tax for income from intellectual property. Such preferential tax treatment is stipulated in the law of the Netherlands, Luxemburg, Cyprus, etc.

Besides tax advantages of registration of an operation company in the foreign jurisdiction, attention should be paid to the goals of long-term planning. Specified jurisdictions also have preferential treatment in respect of holding structures, at payment and receipt of dividends and royalties. And at reasonable combination of jurisdictions the structure will allow not only optimizing expenses for taxation, but also protecting assets and rights for intellectual property.

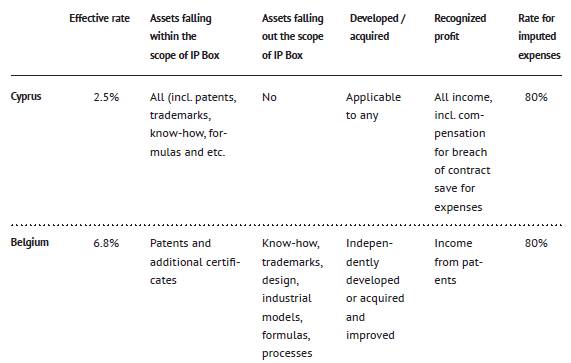

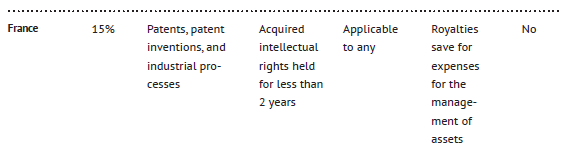

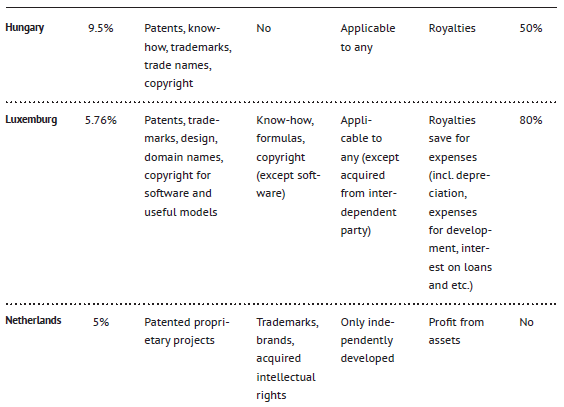

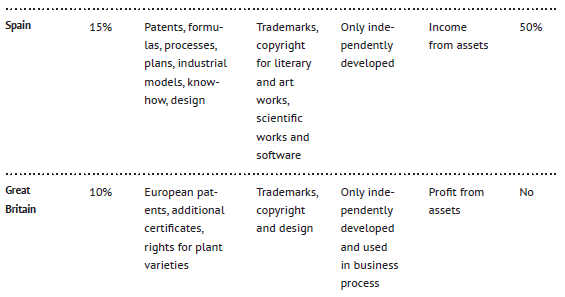

The following is the comparative table of application terms for IP Box regime in some countries.

The foregoing table underlines the distinct advantage of Cyprian IP Box regime, which includes the extensive list of objects of intellectual rights and allows applying the lowest effective rate equal to only 2.5%.

During the last two decades, Cyprus bills itself as the leading jurisdiction in the area of intellectual property after the introduction of favorable tax regime in relation to income received from any type of intellectual property. The new scheme represents an attractive legal and financial basis for the use of objects of intellectual property rights.

Taking into the account the abovementioned, it seems reasonable to look more closely at application terms for IP Box regime in Cyprus.

Cyprus is not the place where the idea of introducing so-called Intellectual Property Box Concept or IP Box was implemented for the first time. It was previously used in some other EU countries: in Belgium, Switzerland, Ireland, Netherlands, Luxembourg and Malta. However, Cyprus has successfully incorporated their experience. Here, IP Box preferences are applied with maximum flexibility without such disappointing limitations present in other countries as:

- Requirement for active participation of employees in the creation of intellectual products;

- Limitation of preferences, if intangible assets are created outside jurisdiction;

- Limited list of intangible assets falling within the scope of IP Box regime.

The lowest profit tax rate in the EU equal to 12.5% and wide network of current international tax agreements easily secure leadership of Cyprus in competition of jurisdictions applied for the purposes of tax optimization using advantages of the international law.

Cyprian IP-Box regime was introduced in May 2012 and has been applied since January 2012. According to the tax law:

- In accordance with revised Clause 9 (1)(e) of the law On Income Tax, 80% of profit from the use of intangible assets (including royalties, compensation for unlawful use and etc.) and profit from the sale of intangible assets shall be deemed imputed expenses reducing the tax base for income tax on such activity;

- Imputed expenses reduce taxable base in addition to other expenses (for R&D, depreciation and etc.). The rest 20% of income received from intangible assets are subject to taxation at standard rate equal to 12.5%;

- Profit shall constitute the base for calculation of “imputed expenses” after all direct expenses for acquisition, development and depreciation of such objects of intellectual property are withheld from applicable income;

- This rule applies to all patents, copyright for various intellectual property and trademarks. The law does not stipulate definition or the list of intangible assets governed by new regime. Instead, the law specifies that regime applies to intangible assets as they are defined under the Patent Law, Law On the Rights for Objects of Intellectual Property and Law On Trademarks. These laws govern the following types of objects of intellectual property: trademarks, patents, rights for objects of intellectual property (scientific, literary, musical, art works, cinema, data bases, sound records, transfers, publications). In any case, if there are doubts whether any intangible assets are governed in accordance with new taxation regime, it may be inquired in advance in written at tax authorities of Cyprus through the “system of tax explanations”;

- Capital expenses for acquisition, creation and development of the object of intellectual property now reduce profit as a result of depreciation of the object of intellectual property in equal shares within 5 years starting from the year when they were produced (it means, annually 20% are allowed for deduction).

Let us consider IP Box regime through the example:

- Expenses for the development of trademark equal 100,000 Euro.

- Royalties annually paid by the Russian company equal 30,000 Euro.

- Annual depreciation (within 5 years) equals 100,000 Euro/5 years=20,000 Euro.

Thus:

- Tax base for the first 5 years shall equal (30,000-20,000)-80%=2,000 Euro.

- Profit tax shall equal 2,000 Euro*12.5=250 Euro.

- Tax base for the following years shall equal 30,000-80%=6,000 Euro.

- Profit tax shall equal 6,000 Euro*12.5=750 Euro.

Taking into the account the foregoing and data of the comparative table, the decision of Cyprus to introduce the special taxation regime in respect of objects of intellectual property proved to be quite modern. Reduction of the effective income tax rate for transactions with various intangible assets to 2.5% has to improve attraction of Cyprus for foreign investors holding objects of intellectual property.

In addition to abovementioned advantages, there are also other advantages of this jurisdiction, which make it an ideal place for registration of objects of intellectual property. These advantages include: high level of professional services, executed agreements for the avoidance of double taxation (for example, double taxation with Russia: 0% tax rate on royalties charged at source in the Russian Federation) and geographical location.

- Letter of the Russian Ministry of Finance No. 03-00-RZ/16236 On the Application of Tax Reliefs Stipulated in International Agreements for the Avoidance of Double Taxation dd. 09.04.2014

Other Articles on Topics