What changes for VAT payers in 2015:

Let’s consider in more details the procedure for control over deductions and consequences for taxpayers.

From 1 January 2015, submitting VAT returns, we’ll begin to upload there purchase ledgers and sales ledgers, the ledger of invoices issued and received for intermediaries. All information will be stored in “Big Data” system of the FTS of Russia. To work in this system, the special software “ASK VAT-2” is developed. How does the software work? All invoices will flow into a nationwide database. The software will itself compare data on each transaction in the chain of movement of goods. The system will show to inspectors the tax breaks in transactions with deductions, but on which VAT is not paid. By such discrepancies tax officers will be able to demand from companies invoices and primary documents. This right is given to them from 1 January 2015. Accordingly, if the taxpayer is engaged in relationships with the so-called unscrupulous contractors that do not assess VAT payable to the budget, all VAT deductions that do not correspond to VAT accruals will be visible in “Big Data” system. Further information about illegal deductions will be sent to the tax officials in the territorial inspectorates and it will be immediately clear what amounts of VAT are illegally reported as deductible or refundable. The result can be the field tax audit. In 2015, a special service will start to operate where the invoice number will show whether the supplier assessed VAT on transactions or not. The service starts working from 1 January 2015 and now can identify unscrupulous suppliers and each fact of their failure to pay VAT. After that, tax officers may send an inquiry to the organization, which did not report the sale and therefore did not pay VAT. It is very likely that tax officials will not receive any answer. Moreover it is likely that the tax officers will block the settlement accounts of that supplier and, on the other hand, if they get the answer that they did not sell anything to us, the taxpayer-buyer will have the amount of tax deductions reduced.

ASK VAT-2 functionality

The automated control system VAT-2 is designed for operation at RF FTS equipped facilities of all levels, up to the territorial tax authorities, and is not an autonomous system.

Functions

ASK VAT-2 is designed to perform the following functions:

- Acceptance of tax returns from taxpayer (obtaining of container, check of digital signatures, check with the scheme, transmission of the main VAT return to the EDP system, formation and transmission of the receipt).

- Uploading and processing of the ledgers of invoices issued/received.

- Sending of messages to the TP, including on refusal to accept tax return, results of the cross-audit, etc.

- Receipt and processing of updates to the VAT return. Including processing of additional sheets to the Ledgers.

- Check of the INN of the TR and counterparty by control figures.

- Processing of transactions involving intermediaries.

- Performance of audits, SF of previous reporting periods provided for deduction.

- Loading of data of VAT returns.

- Maintenance of information according to the data of Ledgers of VAT returns.

- Implementation of the format- logical control of data of VAT returns.

- Comparison of data of purchase ledgers with the data of purchase ledgers of counterparties.

- Reporting on the work of the System.

- Provision of data for visualization of information in the System of provision of results.

VAT return

The statements for the first quarter of 2015 shall include a new VAT return approved by the order of the Ministry of Finance of Russia from 29.10.14 No. MMV- 7-3/558 @.

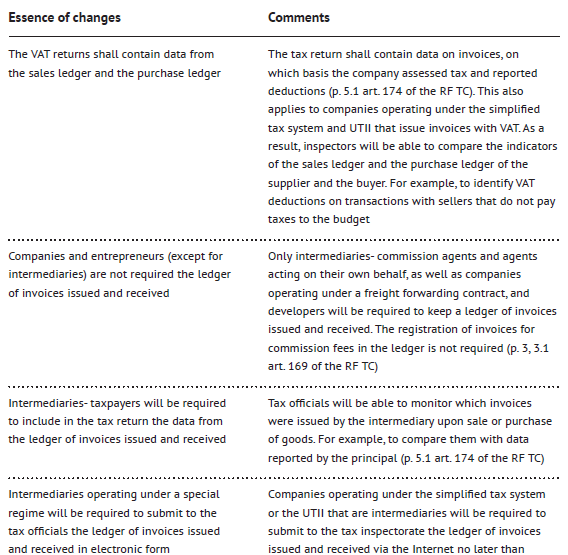

It is the new format of the tax return that allows tax authorities to obtain sufficient information to control secularity of accruals and deductions of VAT, as it contains information about all VAT accruals and deductions in terms of invoices.

The developed form differs significantly from the form from 2014. In particular, from 2015, the organizations will be required to include in the VAT return information from the purchase ledgers and sales ledgers. In case of the agency business the VAT return shall contain information specified in the ledger of invoices issued and received.

The tax return includes:

- The title page;

- The sections:

- “Amount of tax payable to the budget (recoverable from the budget), according to the data of the taxpayer”.

- “Amount of tax payable to the budget, according to the data of the tax agent”.

- “Calculation of the amount of tax payable to the budget for transactions subject to tax at the rates provided for in points 2-4 of article 164 of the Tax Code of the Russian Federation”, appendix 1 to section 3 of the tax return “Amount of tax recoverable and payable to the budget for the past calendar year and the previous calendar years”, appendix 2 to section 3 of the tax return “Calculation of the amount of tax payable on transactions of sale of goods (works, services), transfer of property rights, and amount of tax deductible, by foreign organization engaged in entrepreneurial activity in the Russian Federation through its subdivisions (representative offices, branches)”.

- “Calculation of the amount of tax on transactions of sale of goods (works, services), for which justification of application of the tax rate of 0 percent is documented”.

- “Calculation of the amount of tax deductions for transactions of sale of goods (works, services), for which justification of application of the tax rate of 0 percent was previously documented (not documented)”.

- “Calculation of the amount of tax on transactions of sale of goods (works, services), for which justification of application of the tax rate of 0 percent is not documented”.

- “Transactions not subject to tax (exempt from tax); transactions not recognized subject to taxation; transactions of sale of goods (works, services), the place of which is not recognized the Russian Federation; as well as the amounts of payment, partial payment against future supplies of goods (performance of works, provisions of services), which cycle of manufacturing is more than six months”.

- “Details from the purchase ledger on the transactions reported for the past tax period”, appendix 1 to section 8 of the tax return “Data from additional sheets of the purchase ledger”

- “Data from the sales ledger on transactions reported for the past tax period”, appendix 1 to section 9 of the tax return “Data from additional sheets of the sales ledger”.

- “Data from the ledger of invoices issued on transactions carried out on behalf of another person on the basis of commission contracts, agency contracts or freight forwarding contract reported for the past tax period”.

- “Data from the ledger of invoices received on transactions carried out on behalf of another person on the basis of commission contracts, agency contracts or freight forwarding contract reported for the past tax period”.

- “Data from invoices issued to persons referred to in point 5 of article 173 of the Tax Code of the Russian Federation”.

VAT return is submitted on a quarterly basis. The term of submission of tax return from 2015 is not later than the 25th day of the month following the expired quarter. In 2015, as in 2014, the document is received by tax inspectorates in electronic form only.

Let’s summarize. From 1 January 2015 relationships with dubious counterparties should be avoided, since the right to VAT deduction will be initially controlled by tax authorities not by means of desk audits in the event of VAT recoverable and not through field audits every three years, but much operatively due to the use of “Big Data” RF FTC.

The issue on how tax authorities will “remove” the VAT inappropriately reported as deductible, is not yet clear. But I believe that the practice will be based on evidence in court of the fictitiousness of transaction. As a result, besides the deprivation of the right to deduct VAT, costs taken into account when calculating the tax base for profits tax will be under the “blow”.

Igor Chaika

Ex-Managing Director

Audit Practice

Korpus Prava (Russia)

Other Articles on Topics

See Also Articles from the Issue

Deoffshorization or Come back! I’ll forgive everything

In December 2013 in the address to the Federal Assembly the president Vladimir Putin stated that Russia needs a system of measures for “deoffshorization” of the Russian economy. According to him, some estimates evidence that 9 out of 10 transactions, including transactions with state-owned companies, are not subject to the Russian laws.

January 16, 2015

Overview of Legislative Changes of Foreign Jurisdictions

We will speak about Cyprus, which adopted FATCA, the requirements for filing financial statements of Cypriot companies tightened, the rules of the regulator changed. In addition, we will mention the changes of the legislation of the British Virgin Islands.

January 16, 2015

Last Bow of the RF SAC

Starting to speak about the Resolutions of the Plenum of the RF Supreme Arbitration Court, they should be treated with a special respect, as these are the last Resolutions of the RF SAC. That is not the last in time, but the last in general. From 7 August 2014 the RF SAC ceased to exist.

January 16, 2015

What the Past Year Left: Tax Legislation Amendments

When there are disasters around such as law on controlled foreign companies, it is difficult to get distracted and to pay attention to anything else relating to taxes. However, the Tax Code sheds its editions like leaves and, whether we like it or not, we shall follow this process in order to not be trapped.

January 16, 2015

Amendments to the Russian Law on Individuals

The past year brought to the citizens of the Russian Federation, who have the legal right of permanent residence outside the Russian Federation, the obligation to notify the authorities of the federal migration service of the existence of this right.

January 16, 2015

Intellectual Life News

The civil law in Russia gradually evolves under the general roar of probably historically significant events. This also concerns the intellectual property rights: in March 2014 a package of amendments to part 4 of the RF Civil Code was adopted.

January 16, 2015

Corporate Law Reform

The past year 2014 is best remembered for its succession of important and significant changes that affected the foundations of the Russian civil law. The adopted innovations did not come by the part of the civil law, which regulates corporate relations as well.

January 16, 2015

Q&A: Specific Issues Related to the Implementation of CFC

The CFC law is not our invention. It’s a trend. And we now move with the time. However, when reading the law one thing is clear: in a first approximation our bill is a usual CFC law. If you look under a magnifying glass, the question: what were the goals of the legislator while adopting the law arises.

January 16, 2015