VAT without Borders

In edition No. 3 for 2014, we have told how goods delivery activities are subject to VAT in the European Union. There, we have also promised a sequel on two other activities subject to VAT: rendering of services and import of goods into the European Union. In this article, we keep our promise.

The European law understands rendering of services as any activity, which does not constitute goods delivery, including the following activities:

- Transfer of intangible assets;

- Obligation to refrain from any action or permit any action;

- Rendering of services under the law or the order of the government;

- Temporary use of goods for personal goals of a tax payer not related to his/her business activity, if VAT for these goods was fully or partially declared for deduction;

- Free of charge rendering of services by a tax payer for purposes not related to his/her business activity1.

For determining location for service rendering it is essential who is the client: a party being the VAT payer or not. If a client is the VAT payer (hereinafter we shall refer to such operations as B2B), location for service rendering shall be deemed his/her location. If services are rendered to permanent representative office of the client, then it shall be the location of such representative office2.

Example 1: a company located in Bulgaria renders accounting services to a company located in Austria. VAT calculated in accordance with Austrian rates shall be levied.

Example 2: a Polish company renders legal services to permanent representative office of Swedish company in Finland. VAT calculated in accordance with Finnish rates shall be levied.

If a VAT payer acquires services for personal use not related to business activity, location of service rendering shall be the location of the seller.

Example 3: a Portuguese company renders educational services to a company located in Denmark. VAT calculated in accordance with Portuguese rates shall be levied.

The same rule applies if the client is not a VAT payer (hereinafter, B2C activity)3.

Example 4: a company located in Greece renders consulting services to a private party living in Romania. VAT calculated in accordance with Greek rates shall be levied.

Thus, each time at rendering of services the contractor defines whether it will B2B or B2C activity. Generally, the VAT payer is any party performing business activity4. In practice, the number of registration as the VAT payer is the best evidence of business activity of a contracting party. The problem resides in the fact that almost in each state of the European Union there is a threshold level for annual turnover of small entities, without exceeding which economic subjects are not obliged to register as VAT payers.5 If a contracting party cannot provide the number of a VAT payer, the service provider may demand other documents confirming B2B activities: certificate of a tax authority, official letter on the letterhead and other.

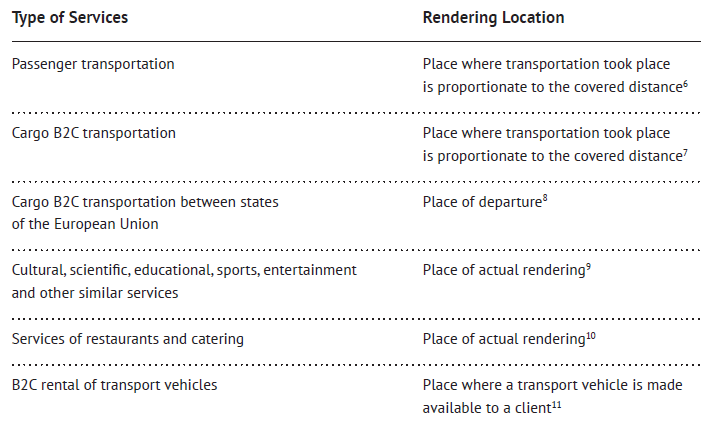

Classification according to B2B and B2C activities is not enough for defining location for service rendering. The European Union law specifies a number of services, in respect of which the place of rendering is recognized not as the location of the contractor or the client, but as the location of their actual rendering. The list of such services is set forth in the table:

There are special regulations for defining location for implementing services rendered to private parties and non-commercial organizations through electronic communication channels (hereinafter, electronic services).

- Telecommunication services;

- Radio and TV broadcasting services;

- Provision of websites, web hosting;

- Software provision and upgrade;

- Granting access to data bases and provision of music, video, games and texts;

- TV broadcasting;

- Distance learning12.

If a consumer of electronic services lives or is situated in the state of the European Union other than the seller, the state of the consumer shall be recognized as the location of rendering (unlike other B2C activities). This rule also applies, if the provider of electronic services is located outside the European Union.

Example 5: an English company granted access to electronic book to a person living in Spain. VAT calculated according to Spanish rates shall be levied.

Obligation to pay VAT from the activity is placed on the seller, if the client and seller are in the same state of the European Union13. But there is an exception. If the client and the provider of B2B activities are in different states, VAT shall be paid by the client in accordance with the mechanism for the payment of VAT at source of income (reverse charge mechanism, hereinafter, the RCM)14. Actual obligations for transferring money to the budget does not accrue: the client credits his/her VAT account with the amount of the output tax calculated out of the cost of the received service, and at the same time debits his/her account with equal amount of the input tax15.

However, if the service provider registered in EU state 1 has acquired any goods or services (or imported goods) for the performance of activity subject to the RCM in EU state 2 and as a result has paid VAT to the third party in EU state 2, the amount of paid VAT shall be repaid from the budget of EU state 216.

If a company, which is the consumer of services in another state of the European Union, is not registered as VAT payer, it means its annual turnover does not exceed threshold level specified in the country of its location, input and output VAT for the client is not charged. The provider issues invoice with VAT; the cost of received services is added to the cost of services rendered by the client itself, depending on which it is required or not required to register as VAT payer.

Service provider subject to RCM shall monthly or quarterly submit to tax authority of its state a report specifying the following information:

- Number of registration as VAT payers of consumers of the foregoing services;

- Total cost of services rendered during the report period17.

RCM is not applied in relation to services rendered to private parties, so providers of electronic services are not in a favorable position: they have to register as VAT payers and pay tax in each state of the European Union where they render services to private parties. States solve this problem in different ways. In Great Britain, for example, there is Mini One Stop Shop service, which allows registered users to report VAT for payment in all states of the European Union; tax service of Great Britain sends tax returns and payments to authorities of applicable states.

Import of Goods

Import of goods for taxation purposes means import to the territory of the European Union of goods, which are not fully tradable in accordance with the treaty establishing the European Union (Treaty of Rome in 1957). It should be remembered that unified rules for taxation of activity on import of goods are not applied in certain territories included as a part of member states of the European Union, namely:

- Mount Athos;

- The Canary Islands;

- The French Overseas Territories;

- The Aland Islands;

- The Channel Islands;

- Heligoland;

- Busingen (Germany);

- Ceuta and Melilla;

- Livigno and Campione d’Italia;

- The Italian territory of Lake Lugano18.

A party registered in the System of Registration and Identification of Economic Operators (EORI scheme) may act as the importer of goods to the European Union.19 Not only the party located within the customs territory of the European Union may receive EORI number, but any party, which intends to submit entry or customs declaration to tax authorities of the state of the European Union.20 Application for the receipt of EORI number may be submitted upon the first transaction at the customs of the European Union.

According to the general rule, location of sale shall be deemed the state where goods are located right after import to the territory of the European Union.21 However, if goods are imported under certain customs procedures, the location of sale shall be deemed the state where goods are released into free circulation.22 Customs procedures, which grant delay of VAT payment, are stipulated in the national law of each state. For example, in Great Britain these are the following procedures:

- Processing within the customs territory;

- Temporary import with complete exemption customs duties;

- Processing under customs control;

- Procedure for customs warehouse;

- External or internal transit;

- Procedure for temporary storage.

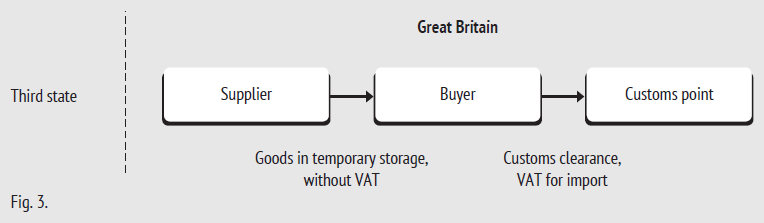

The national law may stipulate that delivery of goods, in respect of which one of preferential customs procedures is applied, shall be released of VAT23. For example, according to the law of Great Britain, import of goods already delivered to the territory of such state, but not yet delivered to the customs point and temporary stored, shall be released of VAT.

However, acquisition of goods under one of the said customs procedures in the other state of the European Union (IC-acquisition) implies obligation to pay VAT from transaction on acquisition, regardless that delay applies to VAT from import.

In order to define exactly which reliefs may be obtained upon placement of imported goods under any other customs procedures the general European law is not enough. Each time we should refer to the national law of the country of import.

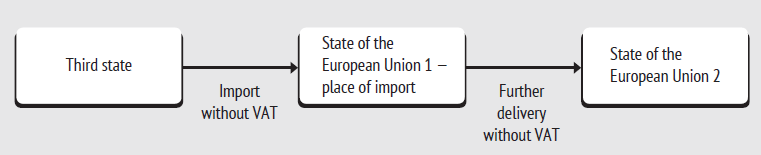

However, the following rule is the same for all countries. If transfer of imported goods ends in the state other than the state where goods are located right after import to the territory of the European Union, then in such last state VAT from import is not levied24 and goods are immediately released into free circulation:

The importer may enjoy the said relief provided he/she submits to tax authorities of the state of import the following information:

- Number of registration as VAT payer in the state of import or the number of its tax representative;

- Number of registration as VAT payer of the seller in the state where the goods are subsequently imported;

- Evidence that goods are sent or will be sent to other state of the European Union25.

As it was already mentioned in the previous article dedicated to VAT in the European Union import of goods involving crossing of borders with the states of the European Union shall be released of VAT. Tax on this activity shall be paid by the buyer in the state of final destination of goods; and he/she acquires the right for deduction in the amount of payment.

Deduction of VAT paid for Import of Goods

VAT payer shall be entitled to submit for deduction VAT amounts26 paid for import of goods used for taxable activity,27 and also:

- Cross-border import of goods in the European Union (IC-import);

- Set of activities for acquisition of goods released of taxation (IC-acquisition);

- Export operations;

- Import of goods, in respect of which customs procedures granting release of VAT are applied.

Deduction may be specified in tax return for the period when import is made.

- Clauses 24, 25, 26 of Directive 2006/112/ЕС of the European Union

- Clause 44 of Directive 2006/112/ЕС of the European Union

- Clause 45 of Directive 2006/112/ЕС of the European Union

- Paragraph 1 of Clause 9 of Directive 2006/112/ЕС of the European Union

- Clauses 287, 288 of Directive 2006/112/ЕС of the European Union

- Clause 48 of Directive 2006/112/ЕС of the European Union

- Clause 49 of Directive 2006/112/ЕС of the European Union

- Clause 50 of Directive 2006/112/ЕС of the European Union

- Clauses 53, 54 of Directive 2006/112/ЕС of the European Union

- Clause 55 of Directive 2006/112/ЕС of the European Union

- Clause 56 of Directive 2006/112/ЕС of the European Union

- Clause 58 of Directive 2006/112/ЕС of the European Union

- Clause 193 of Directive 2006/112/ЕС of the European Union

- Clause 196 of Directive 2006/112/ЕС of the European Union

- Clause 168(a) of Directive 2006/112/ЕС of the European Union

- Clause 170(b) of Directive 2006/112/ЕС of the European Union

- Clause 264(b,d) of Directive 2006/112/ЕС of the European Union

- Clause 6 of Directive 2006/112/ЕС of the European Union

- Paragraph 1 of Clause 41 of the Regulation (EEC) 2454/93 of the European Commission

- Paragraph 3 of Clause 41 of the Regulation (EEC) 2454/93 of the European Commission

- Clause 60 of Directive 2006/112/ЕС of the European Union

- Clause 61 of Directive 2006/112/ЕС of the European Union

- Clauses 156, 157 of Directive 2006/112/ЕС of the European Union

- Paragraph 1d of Clause 143 of Directive 2006/112/ЕС of the European Union

- Paragraph 2 of Clause 143 of Directive 2006/112/ЕС of the European Union

- In accordance with the law of the European Union activity released of VAT shall be entitled to deduction as in accordance with the Russian law activity charged at 0% rate

- Clause 169(b) of Directive 2006/112/ЕС of the European Union

Yana Karausheva

Ex-Junior Lawyer

Tax and Legal Practice

Korpus Prava (Russia)

Other Articles on Topics