This article continues a series of publications about the system of imposition of value-added tax in the European Union. This issue is dedicated to a number of court decisions adopted by the highest judicial authority of the European Community regarding VAT imposition in 2013-2015.

The unified legislation requires unified application of legal norms within the entire united community, therefore the highest judicial authority – the Court of Justice of the European Union (hereinafter – the CJEU) – is placed at the top of judicial system of the European Union, which is authorized to interpret legal acts of the European Union and make final decisions on legality thereof1. Over the last years, the majority of decisions of the CJEU have been made as preliminary rulings, which empower any national court to submit any issue that it cannot resolve independently to the Chamber2. Formally, the decisions of the CJEU do not have a binding effect but in practice they are often effective not only for the parties to the dispute but also for third parties3. Below is a review of several decisions of the CJEU adopted over the recent years, which may have a significant influence on some aspects of VAT imposition in the European Union.

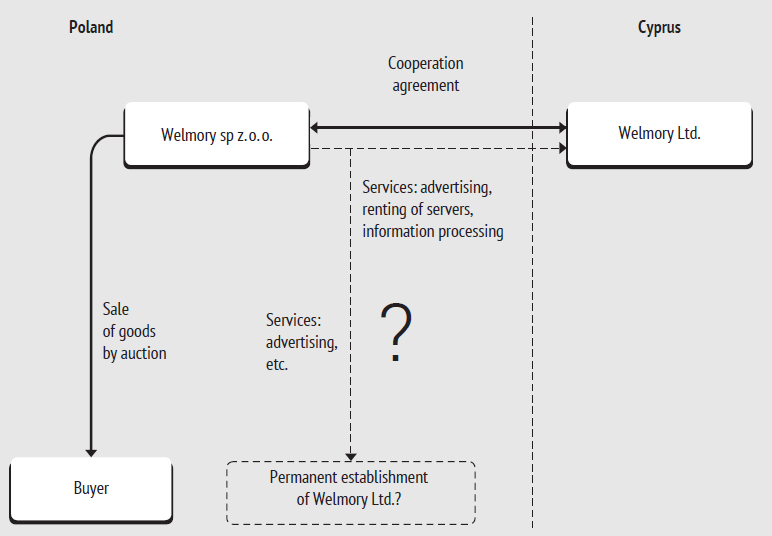

A Cyprus company Welmory Ltd. (hereinafter – Ltd) ran an online auction and sold packets of bids, i.e. the right to place higher bids for goods than the previous bids. In 2009, Ltd concluded a cooperation agreement with a Polish company Welmory spz. o.o. (hereinafter – Welmory), in the course of which Ltd undertook to run the Polish version of the online auction. For that purpose, the technical resources and personnel of Welmory were to be used. On its part Welmory undertook to render services regarding leasing of servers and demonstration of goods on the website. Goods were sold at the auction on behalf of Welmory. Therefore, the income of the Polish company included two parts: payment for the sold goods and remuneration for rendered services from Ltd. In 2010, the Cyprus company acquired 100% of shares of the Polish company. While issuing an invoice for the services Welmory decided that the place of a B2B operation was the customer’s location, i.e. Cyprus (as part of the mechanism of VAT deduction from the source). The Polish tax authority disagreed therewith having decided that the customer of services rendered to the Cyprus company by the Polish company was Welmory establishment in Poland, therefore the Polish VAT shall be subject to deduction4(Fig. 1). The issue on whether the permanent establishment shall be established, if the company uses technical and human resources of the counterparty, located in the other European Union member state in the course of its economic activities was submitted to the CJEU for review.

While identifying the signs of permanent establishment, the Court stated in its decision dated 16.10.2014 that it should be characterized by a sufficiently long and continuous existence and availability of the necessary infrastructure. In the current case this infrastructure must have provided an opportunity to receive and use the services rendered to the permanent establishment exactly in Poland.

However, the Court has not given a decisive answer about whether the permanent establishment of Welmory has been established, having noted that the issues about the fact, namely the availability of signs of permanent establishment, must be reviewed by the national court. According to the Court, if the equipment (server, software) necessary for the operation of the Cyprus company, which is the access of the Polish company to the online auction and the sale of auction applications to Polish buyers, was located outside Poland the permanent establishment was not established. However, the Court has not provided a universal rule in this decision. Nevertheless, the decision affects all economic entities of the European Union which:

- Effect taxable operations in a European Union member state different from their location and do not consider them as operations leading to establishment of a permanent establishment;

- Render services on the provision of infrastructure for conducting business in any other European Union member state without which the customer could not have carried out its activities.

Following the decision on Welmory case, it is likely that the national courts and tax authorities will review their position on permanent establishments and the said economic entities might face a duty to pay input VAT in the state where their earlier presence did not matter for the purposes of taxation.

In July 2015, the CJEU issued a decision on two united cases С-108/14 and С-109/14 related to the right to withhold VAT by a holding company. Larentia + Minerva mb H&Co. KG (hereinafter – Larentia + Minerva) rendered administrative and consulting services to two subsidiary companies. Larentia + Minerva reduced the payable tax amount by the amount of input VAT paid in the cost of services for fund raising necessary to acquire the shares of these subsidiary companies. Marenave Schiffahrts AG (hereinafter – Marenave) incurred expenses including VAT in the amount of € 373,347.57 connected with the increase of share capital. In the same year, the Company acquired the shares of 4 shipping partnerships, which it had been rendering management services to. Marenave deducted € 373,347.57 in full as input VAT from the VAT amount payable for the rendered services. In both cases, the German tax authority acknowledged the right of a partial deduction only.

According to the principles of VAT imposition in the European Union, VAT shall be deducted from entities carrying out economic activities5. Acquisition of equity stake in enterprises and ownership thereof is not an economic activity by itself6 and subsequently does not entitle to deduct the amounts of input VAT. Larentia + Minerva and Marenave carried out mixed activities: VAT-free (acquisition of shares of subsidiary companies) and VAT-taxed (services rendered to these subsidiary companies). Therefore, the CJEU raised an issue on what proportion the amount of deduction of input VAT for the services of capital procurement for the purchase of shares must be determined if the holding company subsequently renders taxable services to the subsidiary companies.

The CJEU determined that expenses regarding acquisition of shares of subsidiary companies by the holding company, which is their managing company and thus conducts economic activities, must be charged to expenses incurred in connection with taxable activities. VAT included in the cost of these expenses may be deductible in full.

If the holding company incurred expenses regarding the acquisition of shares of several subsidiary companies but renders management services only to some of them, input VAT may be partially deductible. The Court ruled to divide the input VAT related to economic (management and consulting services) and non-economic (shareholding) activities of the taxpayer. Criteria for determining economic and non-economic activities to which the input VAT is related are left to the discretion of national executive authorities and courts. The specified decision of the CJEU confirmed that the holding company should be entitled to deduct the VAT amounts paid in the cost of expenses regarding the acquisition of shares of subsidiary companies. The input VAT shall be subject to partial deduction if the holding company renders VAT-free services (supply services) to subsidiary companies.

According to the established practice, service operations effected between the head office and a branch within the European Union shall be tax-free7. In case С-7/13 the Court reviewed an issue whether the specified principle is applied if the branch is a member of a VAT group in the European Union member state where it is located. Skandia America Corp. (hereinafter – SAC), a company registered in the USA, purchased IT-services for Skandia group all over the world. Subsequently the purchased services were distributed to one of the group branches , Skandia Sverige in Sweden, which was a member of the local VAT group . The goal of Skandia Sverige was to use these services in order to receive the final IT-product, which was subsequently delivered to various Skandia group companies – both to those included in the VAT group in Sweden and to those, which are not. Sweden tax authority has registered SAC as a separate legal entity as the VAT payer in Sweden and has charged tax additional payable on IT-service operations between SAC and Skandia Sverige. Skandia Sverige appealed against this decision.

The CJEU determined that in a situation when a company, located outside the European Union (or in any other European Union member state), renders services to its branch, which is a member of a local VAT group like Skandia Sverige, the services must be deemed rendered to the group of VAT payers in general as a united economic entity. The head office and the branch must be viewed as one legal entity and the services must be deemed rendered to an independent counterparty – the VAT group, therefore the operation between SAC and Skandia Sverige was deemed taxable. The CJEU confirmed the position of the tax authority. The obligation to pay the tax on this operation was imposed to the buyer – the VAT group as a tax agent as the supplier is located outside the European Union.

The decision on Skandia case will probably have an impact on taxation of all operations between the head office and the branch in the EU member states. Before adopting this decision, the majority of the EU member states had not considered the operations between the head office and the branch as liable to VAT. Now a number of economic operations carried out within a single company are under the threat of being considered taxable. The consequences may be the following:

- Additional VAT amounts payable if the deductibility of input VAT is limited;

- Obligation to issue additional invoices and submit additional reporting;

- Requirement for registration of a separate subdivision of the company as the VAT payer in the country of location thereof.

In accordance with normal practice, theft of goods shall not be considered a delivery for the VAT purposes. In case С-494/12 the Court of Justice of the European Union was asked a question whether the supply of goods should be deemed taxable, if the payment was effected by a stolen credit card. Dixons Retail plc. (hereinafter – Dixons), the British electrical equipment retailer, concluded agreements with banks under which Dixons undertook to accept credit cards issued by these banks as means of payment from the client, and the banks undertook to pay the cost of goods purchased by this card to the retailer. After declaring and payment of VAT Dixons applied for refund of VAT amounts on sales in the amount of £ 1.9 mln., the payment of which had been effected by stolen credit cards, from the budget. The application was based on presumption that the person who used the credit card as a result of fraud could not provide a legal consideration for the goods, thus the operation was equated with theft. Dixons position was that the supply had not been performed in this situation, therefore, VAT shall not be imposed on this operation. HM Revenue & Customs refused the recovery.

The CJEU decided in disfavor of Dixons. The Judicial Chamber decided that the statutory definition of supply of goods as a transfer of a tangible asset to the other person/entity, which results in enabling that person/entity to dispose of it as owner8, carries objective but not subjective signs. The definition of supply is used regardless of the objectives of participants of the operation or the results thereof9. Illegal use of payment shall not change the classification of the operation as a taxable supply of goods: Dixons delivered the goods to the buyer voluntarily and for remuneration. The fact that the seller received the payment for goods not directly from the buyer but from a third person cannot change the amount of payable tax.

- Article 267 of the Treaty on the Functioning of the European Union (Treaty of Rome, 1958).

- Lang et al (Eds), CJEU- Recent Developments in Value Added Tax 2014, p. 9.

- C. Baudenbacher, The Implementation of Decisions of the ECJ and the EFTA Court, Texas International Law Journal, Vol. 40, 2005, p. 397.

- Welmory, C‑605/12.

- Article 4 of the Sixth Directive of the Council of the European Union 77/388/ЕЕС.

- Portugal Telecom, C‑496/11, EU:C:2012:557.

- FCEBank, C-210/04.

- Article 14 (1) of Directive 112/2006/ЕC.

- Optigen and Others, C‑355/03 and C‑484/03.

Yana Karausheva

Ex-Junior Lawyer

Tax and Legal Practice

Korpus Prava (Russia)

Other Articles on Topics