For a long time, closed-end mutual real estate investment funds have been an effective legal tool of tax planning, which taxpayers used to defer profit tax or to avoid profit tax completely on quite legitimate grounds. Thus, today there is a quite common practice, when real estate located in the Russian Federation is transferred to the assets in trust of the closed-end mutual investment fund, and nonresident companies, which have bilateral agreements on the avoidance of double taxation with the Russian Federation allowing them to exempt income from the mutual investment funds at the source of payment in the Russian Federation, act as shareholders.

For a long time, companies registered in Cyprus were the most popular for the purposes of participation in the considered scheme. This was due to the fact that under the bilateral agreement on the avoidance of double taxation executed with Cyprus, income from mutual real estate investment funds was recognized as other income subject to taxation only in Cyprus (article 22 of the Agreement). And in accordance with the national law of the Republic of Cyprus, transactions with equities of investment funds are not subject to income tax in the Republic of Cyprus.

However, after Cyprus signed the Protocol to the agreement on the avoidance of double taxation (came into force on April 2, 2012 and became effective from January 1, 2013), Cyprus lost its reputation of an attractive and effective jurisdiction, which could be used for the purposes of structuring ownership of Russian real estate through mutual investment funds. The case is that in accordance with article 3 of the Protocol, income acquired through real estate trusts, mutual real estate funds or similar collective investment forms, established, first of all, for investments into real estate, are equaled to income from real estate. It means that income of a shareholder being the resident of the Republic of Cyprus acquired in the form of interim payment on equities of the mutual real estate investment fund, and also at redemption or sale of such equities is subject to taxation in the territory of the Russian Federation as income from real estate (i.e. at the rate of 20% according to subclause 10 clause 1 article 309 and subclause 1 clause 2 article 284 of the Tax Code of the Russian Federation). It is also confirmed by regulatory authorities in their clarifications (letter of the Ministry of Finance of the Russian Federation No. 03-08-05 dd. January 28, 2011).

After Cyprus receded from its leading positions, Russian business owners were concerned with finding an appropriate jurisdiction, which would be able to replace Cyprus properly, for registration of a shareholder of the Russian mutual investment fund.

For more than five years, the choice balanced among such European countries as Malta, Ireland, Bulgaria and Switzerland. However, none of the said jurisdictions could repeat the success of Cyprus and provide similar tax advantages. The use of the mentioned jurisdictions, certainly, optimized taxation of income from Russian mutual investment funds, but didn’t bring it to naught as easily as it was with Cyprus. It is fair to say that in such conditions for some business owners it was more profitable and easier to transfer equities of the fund to an individual being the tax resident of the Russian Federation and pay 13% without creating a foreign infrastructure of their business.

However, the black streak was surely to give way to the white one, and it finally happened. On January 18, 2016 the Russian Federation signed the agreement on the avoidance of double taxation with Hong Kong. The agreement was ratified on July 3, 2016 and shall apply to legal relations from January 1, 2017.

The agreement with Hong Kong expressly answered many questions of Russian business owners, including the question which jurisdiction to use at registration of a shareholder of the Russian mutual real estate investment fund.

This article provides analysis of jurisdictions, which for some time could be seen as an alternative to Cyprus (to various extents of conventionality) prior to execution of the agreement with Hong Kong, and also reveals advantages of Hong Kong.

It should be said that at analyzing and choosing the most favorable residency country for a future shareholder of the Russian investment fund, first of all, the following criteria should be taken into the account:

- This country should have the agreement on the avoidance of double taxation executed with the Russian Federation;

- The agreement on the avoidance of double taxation should stipulate possibility of qualification of income from mutual real estate investment funds in the Russian Federation as other income and absence of need for their taxation in the country of the source of payment of income (in the Russian Federation);

- There should be low tax rates on the tax on profit from such income in the country of residency of income recipient.

It should be also pointed out that in this article by speaking about income from mutual investment funds we imply income in the form of interim payments on equities regularly received by a shareholder.

Luxembourg

The Russian Federation has also signed with the Great Duchy of Luxembourg the Protocol introducing amendments to the existing Agreement on the Avoidance of Double Taxation between the countries, similar to amendments introduced in Cyprus. It came into force almost simultaneously with the Cyprus protocol (30.07.2013). According to the Protocol, income received from equities of mutual funds, established, first of all, for investments in real estate, is equaled to income from real estate. Therefore, income of a shareholder being the resident of the Republic of Luxembourg received from participation in the mutual real estate investment fund in the Russian Federation is subject to taxation in the territory of the Russian Federation as income from real estate (i.e. at the rate of 20%).

The United Kingdom

The United Kingdom is a quite attractive country for the purposes of taxation. Thanks largely to the fact that it has bilateral agreements on the avoidance of double taxation with more than one hundred countries. Companies registered in England are often used as an effective tool for minimizing taxes.

According to the provisions of the current Convention on the Avoidance of Double Taxation between the countries dd. 15.02.1994, unlike previously considered jurisdictions (Cyprus and Luxembourg), income received from the ownership of equities in the real estate investment fund in the United Kingdom are not expressly recognized as income from real estate.

However, article 21 “Other Income” of the current Convention has a clause, which stipulates that payments from trusts or property inherited due to the death cannot be recognized as other income. In view of the said clause, at first sight it seems impossible to qualify interim payments on equities of investment funds as other income. However, in fact everything is rather different. The term “trust” is a notion of the English law, and the Russian legislation has no such definition. Under the English law, the trust represents an obligation of some trustee to manage property transferred under his/her control for the benefit of third parties (fund beneficiaries), which may include the trustee him/herself and the party entrusting management of the property. In accordance with the Russian legislation, a mutual investment fund is a separate property complex consisting of property transferred by the trustor (trustors) in trust of the management company, provided such property is unified with the property of other trustors, and from the property acquired during such management, and the share in the title for such property is certified by the security issued by the management company (article 10 of Federal Law No. 156-FZ “On Investment Funds” dd. 29.11.01). As we can see, the terms “trust” and “mutual investment fund” are not identical in their legal nature. Moreover, at application by the Russian Federation of the Convention any term not defined in it has the meaning assigned to it in the law of the Russian Federation (clause 2 article 3 of the Convention).

In relation to the abovementioned, we believe that interim payments on equities of the mutual real estate investment fund located in the Russian Federation in favor of the shareholder being the resident of the United Kingdom must be qualified as other income in the country of residency of the shareholder (in the United Kingdom). Profit tax rate in the United Kingdom is relatively low in comparison to other European countries (France, Belgium, Italy, Spain, Germany and other), however, it is much higher than the profit tax in the Russian Federation, equaling from 20% to 25% (the rate amount varies depending on the size of annual net profit of the company).

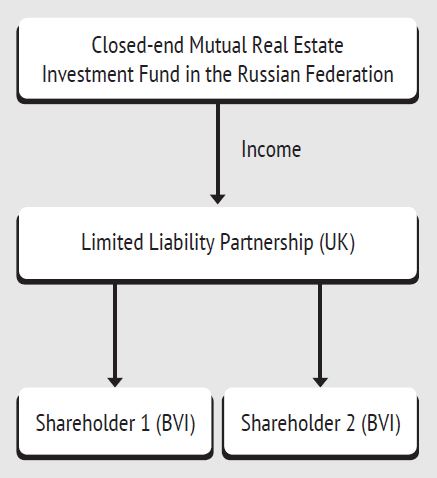

It should be noted that at present time many experts claim that it is possible to optimize the “Mutual Investment Fund in the Russian Federation – shareholder in the United Kingdom” scheme by using as a shareholder of such form of a legal entity a Limited Liability Partnership (LLP), which members are residents of an offshore zone (for example, British Virgin Islands). According to some experts, it will allow significantly optimizing taxation of the shareholder’s income.

In the United Kingdom a special feature of such form of a legal entity as LLP is that under the British law income of LLP is not subject to taxation, if its members are not residents of the United Kingdom, do not carry out any activity there, and the commercial activity of the partnership is not carried out in the territory of the United Kingdom, and there are no sources of its income there. In such case members of the partnership must pay taxes in the state of their residency, and given that in the territory of the British Virgin Islands there is no corporate tax or income tax for individuals, it results in the allegedly tax free organization scheme for the receipt of income from the Russian mutual real estate investment fund.

However, in our opinion, in practice such scheme cannot be implemented due to the following reasons. Within analyzed circumstances, LLP will not be recognized as the resident of the United Kingdom, thus, provisions of the Convention on the Avoidance of Double Taxation shall not apply to it, and therefore income of a shareholder of the Russian mutual real estate investment fund shall be subject to taxation at source of payment in the Russian Federation (clause 6 article 309 of the Tax Code of the Russian Federation). Thus, the use of such form of a legal entity as LLP does not fit the financial activity with the countries, where there is a tax at source of payment, including the Russian Federation.

Netherlands

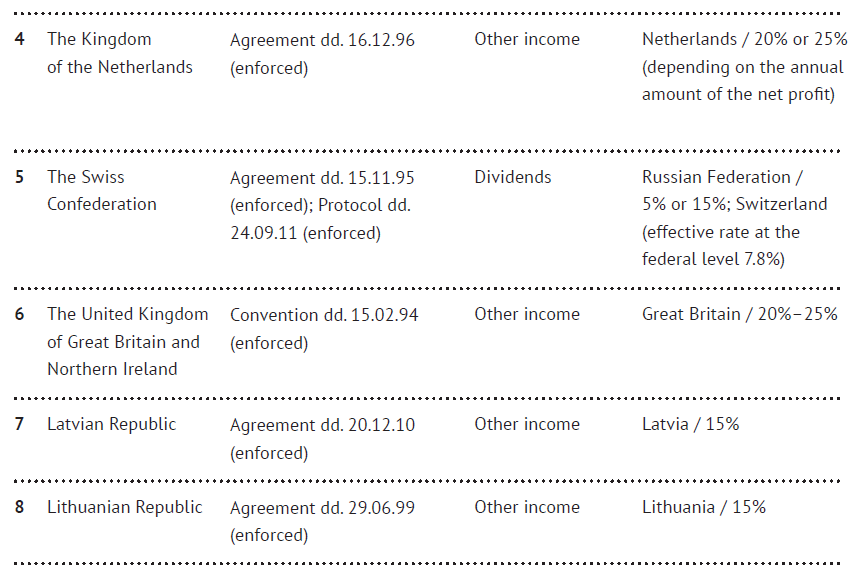

There is also an Agreement on the Avoidance of Double Taxation executed between Russia and the Netherlands simultaneously with the Protocol to it. Based on the provisions of such Agreement, income received by the Dutch shareholders from the Russian mutual real estate investment funds may be qualified as other income subject to taxation only in the territory of the Kingdom of the Netherlands. In such case, there is no taxation at source of payment in the Russian Federation. In the Netherlands the profit tax rate is differentiated as it depends on the annual size of the net profit of the company and equals 20% (if the annual net profit of the company is less than € 200 000) or 25% (if the size of the annual net profit exceeds € 200 000).

In accordance with the provisions of the Agreement on the Avoidance of Double Taxation, it is impossible to qualify such income as dividends because the protocol stipulates that the term “dividends” includes profit transferred from Russia and received by the resident of the Netherlands from participation in joint enterprise with Russian and foreign investments, which for tax purposes is considered a corporate entity or a legal entity (which according to the Russian law does not include the mutual investment fund).

Malta

Governments of the Russian Federation and Malta has signed the Convention on the Avoidance of Double Taxation and Prevention of Tax Evasion in respect of income taxes in Moscow on December 15, 2000, however, until now the Convention has not been ratified by the Russian Federation and has not come to effect (comes to effect in 30 days from the date of the last notice on the fulfillment of national procedures by the Parties).

The Convention on the Avoidance of Double Taxation executed between the Government of the Russian Federation and the Government of Malta does not provide details on the procedures for the taxation of income received from Russian mutual investment funds. Therefore, such income should be also qualified as “other income”, which according to the provisions of the Convention is subject to taxation only in the state of residency of the party receiving such income (i.e. in Malta). The profit tax rate in Malta is one of the highest in Europe and equals 35%.

In Malta imputation tax system is applied, and it stipulates possibility of tax refund equaling from 2/3 to 6/7 of the paid tax.

For example, income received from investments is allocated by Maltese companies as dividends. The tax paid by a Maltese company is subject to refund provided such dividends are allocated from income assigned to a foreign account, on which such income accrues. Income assigned to a foreign account means income received outside Malta, for example, dividends, income from capital investments and other. Income from participation in the mutual real estate investment fund is not directly specified, but in our opinion, it will be also accounted on the foreign account of a Maltese company.

Tax refund is calculated based on the tax paid above the required amount in accordance with bilateral agreements on the avoidance of double taxation, unilateral tax reliefs and agreements on the reduction of the income tax within the Commonwealth of Nations. It means taxes paid abroad may also be taken into the account at calculation of the tax refund provided the general tax refund does not exceed the tax amount paid in Malta. If calculated under the flat rate FRFTC, tax refund is calculated on taxes paid in Malta.

If a Maltese company requests the flat rate FRFTC, which under the Maltese tax law is one of the 4 forms of relief from double taxation, any tax refund shall be limited by 2/3 of Maltese taxes, which results in maximum effective tax rate of 6.25%.

Switzerland

Previously, the Agreement with Switzerland was unclear in respect of payments on equities in the mutual real estate investment funds as taxable or exempt income, and also unclear in respect of applied rate of tax at source. Such ambiguity was in a way eliminated by the Protocol to the Agreement, which was signed on September 24, 2011 (came into force on November 9, 2012).

As a result of negotiations between Russia and Switzerland, unlike Protocols to the Agreements on the Avoidance of Double Taxation between Russia and Luxembourg and Cyprus, it was resolved to leave the definition of “income from real estate property” unchanged in respect of taxation of income from mutual investment funds established for investments mainly in real estate property. This is good news for taxpayers because such type of income as income from mutual real estate investment funds is no longer subject to unlimited taxation in the country of origin of such income. In contrast, after the Protocol came to force, such income is deemed dividends subject to taxation at source under applicable rates of 5% from the total amount of dividends (if the company receiving dividends owns at least 20% of assets of the mutual real estate investment fund, and the foreign capital invested in the fund exceeds two hundred thousand Swiss francs) or 15% of the total amount of dividends (in all other cases). It should be noted that any payments on equities of the investment funds (not being real estate funds), acquiring more than 50 percent of their income due to shares, are now deemed dividends.

Article on methods of eliminating double taxation (article 23 of the Agreement) stipulates method of exclusion of double taxation for all types of income taxable in Russia for Swiss residents. If a Swiss company receives income, which in accordance with the provisions of the Agreement may be taxable in Russia, the tax amount in respect of such income subject to payment in Russia may be deducted from the tax charged in Switzerland. Regarding federal taxation in Switzerland, dividends received by a Swiss company are included in the tax base (the effective tax rate on the federal level is 7.8%). Thus, withheld tax at source in the Russian Federation may be accounted at calculation of tax in Switzerland. However, it should be noted that in Switzerland on the level of cantons a company must also pay taxes, and also in certain conditions may have tax benefits and discounts (depending on the canton).

Denmark

The Convention on the Avoidance of Double Taxation executed between the Russian Federation and Denmark (Convention dd. 08.02.96) allows to qualify income of a Danish company from interim payments on equities of the mutual real estate investment funds in the Russian Federation as other income subject to taxation only in Denmark (article 21 of the Convention). However, such state as Denmark is by no means famous for the low profit tax rate, at present time the profit tax rate in Denmark equals 22%. At the same time, the law of Denmark provides opportunity to register and use in their activity companies with zero tax rate. It refers to companies of K/S type, which every year become more popular among business people. Companies of K/S type represent a partnership consisting of at least two founders, one of which has the status of the General Partner, and other founders have the standard status (Limited Partners).

Danish K/S companies with foreign founders, which do not carry out any commercial activity in Denmark, are not tax residents of Denmark. According to the Danish tax law, K/S company is not regarded as a separate subject of taxation (due to this, K/S company is not assigned with a taxpayer’s number in Denmark), and taxes on profit received by K/S company are paid by founders (General Partner and Limited Partner) at place of their residence pro rate to shares owned by them in K/S partnership.

However, another circumstance is also important: as K/S companies are not taxpayers in Denmark, they accordingly are not subject to cross-border agreements on the avoidance of double taxation executed by Denmark. Thus, income of a Danish K/S company from participation in the Russian mutual investment fund shall be subject to tax at source of payment in the Russian Federation.

At the same time, the Danish law gives opportunity to Danish holding companies to transfer dividends received abroad further to their parent company in countries, which have tax agreements executed with Denmark, without any taxation. Given that under the agreements on the avoidance of double taxation there is preferential treatment for the transfer of dividends to Denmark from many countries, a Danish holding company is an efficient tool for using it as a founder of resident companies in other countries (including Russia). However, such scheme is attractive, as it was mentioned before, for the allocation of dividends received abroad. But under the Russian law interim payments on equities of mutual investment funds cannot be recognized as dividends, as it was noted previously.

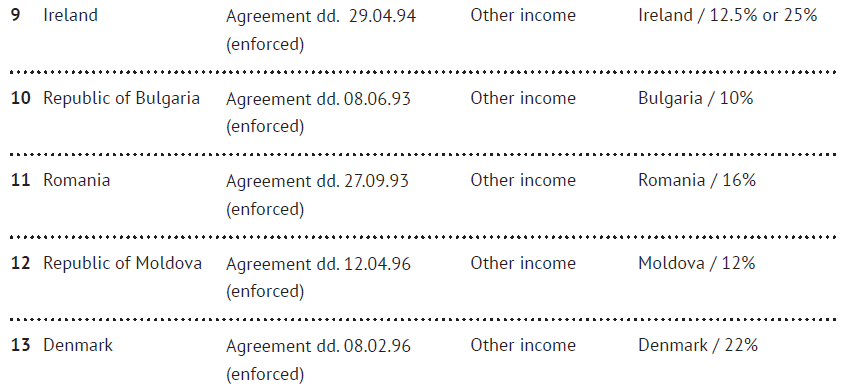

The Russian Federation and a number of other countries have also executed agreements on the avoidance of double taxation, which at present time came to force and are applied to tax relations of the parties. Moreover, texts of the Agreements with such countries as Latvia (Agreement dd. December 20, 2010), Lithuania (Agreement dd. June 29, 1999), Ireland (Agreement dd. April 29, 1994), Bulgaria (Agreement dd. June 8, 1993), Romania (Agreement dd. September 27, 1993), and Moldova (Agreement dd. April 12, 1996) contain quite similar to each other provisions, according to which income of a shareholder being not a resident from participation in the Russian mutual real estate investment fund should be qualified as other income and should be subject to taxation in the state of residence of the shareholder (income recipient). Only profit tax rates applied in the said countries differ. Thus, the profit tax rate in Latvia and Lithuania equals 15%, in Ireland – 12.5% for trade companies (25% for other), in Bulgaria – 10%, in Romania – 16%, and in Moldova – 12% accordingly.

Hong Kong

As it was mentioned before, from January 1, 2017 the agreement on the avoidance of double taxation executed between the Russian Federation and Hong Kong comes to force, and under such agreement payments from the Russian mutual investment funds in favor of the Hong Kong shareholder shall not be subject to tax at source in the Russian Federation. Regarding taxation in the territory of Hong Kong, corporate tax (profit tax) rate in Hong Kong equals 16.5%. However, only profit received from sources in Hong Kong, so called onshore profit, is subject to profit tax. Therefore, income on the investment equity of the Russian mutual investment fund shall not be subject to taxation in the territory of Hong Kong.

For the purposes of systematization of provided information, special features of taxation of income of companies being residents of the abovementioned countries from participation in the Russian mutual real estate investment fund can be represented in the following table:

As it is seen from the carried out analysis of bilateral agreements on the avoidance of double taxation executed between the Russian Federation and other countries, and also from the provided summary table, Hong Kong is the most efficient and single option jurisdiction for optimization of taxation of income from mutual real estate investment funds in Russia.

Please, be aware that within the framework of this article we did not consider special features of structuring business using foreign companies related to current requirements of the tax law of the Russian Federation (in particular, requirements on the disclosure of information and taxation of controlled foreign companies, the concept of the actual income recipient) and upcoming automated information exchange (CRS). That is why at making final decision on structuring your business, we recommend you to request preliminary explanations and consultations of experts.

Alexey Oskin

Deputy Director

Tax and Legal Practice

Korpus Prava (Russia)

Other Articles on Topics