Under constant development of economics and modern business relations it became urgent to introduce new legal constructions into Russian legislature (which includes the constructions of option contract). Worldwide practice shows that this type of contracts has been constantly used both in business and private life.

Thus, an extensive practice of option contract application has its own peculiarities in the Anglo-American legal system. For example, there is no such legal institution as “irrevocable offer” due to automatic consideration provisions in the legal relations of the Anglo-American legislation (Consideration).

The legal construction of option contract had not been provided by russian civil legislation, although similar constructions were mentioned in some legal regulatory acts, for example:

Russian civil legislation used to have no direct provisions for the option contracts, although similar legal constructions were mentioned in a number of legal acts. For instance, Legal Act #2383-1, dated 20.02.1992, on Commodity Exchange and Exchange trade (no longer in force) contained the term “option agreement” to describe the assignment clause for the transfer of rights and obligations at a later date in respect of exchange commodities. The Directive of the Central Bank of the Russian Federation # 3565-U, dated 16.02.2015, on Entrepreneurial Financial Instruments and the Federal Act # 39-FZ, dated 22.04 1996, on Securities Market also contained the term “option contract” and “issuer’s option”, respectively.

Additionally, in practice when similar legal constructions were required, a variety of legal mechanisms analogous to those of option contract were applied. Typically, legal mechanism of the preliminary contract was used to replace the option contract, even though legal implications of the preliminary contract were substantially different.

Preliminary contact is a model that is typically used, but it was completely different from option in the matter of the legal consequences. Following are the main differences between the option contract and the preliminary contract:

- A preliminary contract compels to make, not to perform, the basic/main contract in the future while an optional contact implies fulfillment of its obligations.

- The subject matter of preliminary contract is to conclude the main contract on the terms and conditions stipulated by the preliminary contract. The purpose of the option contract is to obtain the right to acquire some assets during the established period in the future.

- Under the preliminary contract both parties are obliged to enter into the main contract in a certain period of time. Under the option contract it is the Seller (Optioner) who is solely obliged to enter into the main contract while the Buyer (Optionee) has the right to enter into the main contract at his discretion.

- The preliminary contract excludes any payments in contrast to the option contract that is pecuniary.

Irrevocable offer was another legal mechanism widely used to substitute for the option contract. Despite all the similarities with the option contract, the irrevocable offer constitutes more of a base of the option contract, its “skeleton”. Application of this legal mechanism was bound up with a number of legal risks.

Federal Act # 42-FZ, dated 08.03.2015, amended the Civil Code of the Russian Federation by adding two more articles in respect of the option to enter into a contract (Article 429.2) and the option contract (Article 429.3).

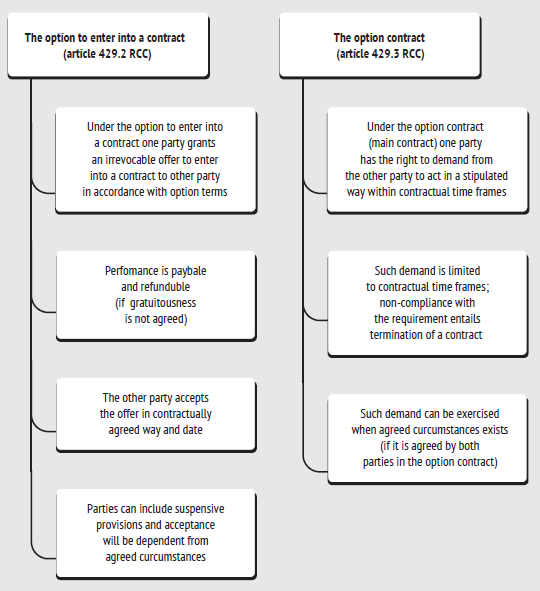

The aforementioned amendments that were introduced into the Civil Code led to the problem of differentiation between the two models. To choose the right mechanism one should gain the understanding of their legal nature (Fig 1).

Under Article 429.2, the option to enter into a contract is an agreement under which one party grants an irrevocable offer to enter into a contract and the other party pays the option price. The last provision is an optional clause.

Terms and conditions of the main/basic contract must be integrated into the agreement and such agreement must be concluded in the same form as the main contract. Modern legislation provides for suspensive conditions for the option that depend on the will of the parties.

Special attention should be paid to additional regulations of cession (assignment) under the option: direct legislative provisions set forth the general right of cession (assignment) under the option agreement as well as the right to prohibit such cession (assignment) if a corresponding provision is included into the agreement. Cession (assignment) is also prohibited if it is readily apparent from the essence of the option agreement.

The right of cession (assignment) under the option contract has a very important practical meaning. Failure to include the provision that prohibits cession (assignment) under the option may put one of the parties at a disadvantage (the subject matter of this legal issue will be discussed in section 2 of the article).

The second model – the option contract – is set forth in Article 429.3. Under the option contract (main contract), one party has the right to demand from the other party to act in a stipulated way. Such demand is limited to contractual time frames. Option contract has been covered by the legislator rather briefly. Thus, general rules in respect of obligations contained in the civil legislation should be applied to the option contract.

Option Contract Formation and its Peculiarities with Respect to Shares/Fractions of the Legal Entities

Options are usually used in two forms: Call (which gives the optionee the right to demand from the optioner to sell or convey assets to him at the agreed price) and Put (which gives the optionee the right to demand from the optioner to buy or receive assets at the agreed price).

The most vivid examples of option contracts formed in respect of shares/fractions of the legal entities:

- Investment agreements (direct investment and strategic investment) and contracts to formate;

- Merger/acquisition;

- Loan liabilities;

- Bonus award contracts, personnel incentive contracts and other in.

In case of usage of the model “the option to enter into a contract” (article 429.2 Civil Code), it is crucial to keep in mind the following conditions:

Time Clause (Terms)

Parties to a contract practically always specify the agreed period of time. Nevertheless, if such condition is not specified, it equal one year, unless this contradicts the legal nature of the contract or business turnover .

Russian legislation does not provide for legal classification of the time limits under the option contract, still based on the legal experience of foreign jurisdictions option contracts can be divided into two types:

- “American option” (the right can be exercised any time within the term of the option contract);

- “European option” (the right can be exercised on the exact contractually agreed date).

As we can clearly see the model of “European option” contains more privileges for the optioner/grantor and “American option” is more preferable for the Optionee.

Option price

One party pays “option price” to opposite party for the right to demand in future. Consequently, payment is made for entering into such an agreement and is not applicable for future payments under the main/basic contract. This payment is not reversionary, that`s why it is usually named “risk fee”.

Suspensive clause

Penal option is the common example of suspensive conditions used in case of shareholder` agreement breach, changes in management structure, etc..

“Covenants” or “restrictive” conditions

The aforementioned problem of cession (assignment) is extremely unfavorable for the Optionee (Buyer) especially when a considerable share holding is sold to a third party without prior notice to the Optionee (Buyer). To overcome this problem an additional restrictive clause (“Covenant”) can be included into the contract to restrain the Optioner (Seller) from cession (assignment). Failure to add this clause can put either party at disadvantage. It is a matter of economic relationship between the parties to the contract if to prescribe the restrictive clause: once the Optioner (Seller) is sure of the Optionee’s (Buyer’s) financial stability, he is not interested in the change of the parties that can cause new risks.

The option contract might contain a clause according to which the Optinee’s (Buyer’s) consent will be required for the Optioner (Seller) to proceed with the following changes: to amend the articles of association, to enter into a non-arm’s length transaction, to dispose of significant assets, to alter share capital etc.

Subject matter

The law requires the subject matter of the main contract to be described in such manner that will help to identify the subject at the time of irrevocable offer’s acceptance (paragraph 4 article 429.2 RCC).

Options in stock and shares relations become more complicated due to the need of notarial deed. The legislator stipulated that option contractual forms shall be equal to basic/main contract form. In case of the declared type of option this legal requirement (notarial form) is mandatory under article 21 Federal Act # 14-FZ, dated 08.02 1998, on Limited Liability Companies) in terms of transfer of shares in part or in whole to company members or third parties. Consequently, option agreement is subject to notoriety certification; non-compliance with the requirement entails nullity of a contract in accordance with paragraph 3 article 163 RCC.

Another legal innovation provided for in item 11 of article 21: regulates that the disposal of shares (in pursuance of the option to enter into a contract ) could be executed by notarization, this notarization can be done individually without consent of other party.

Such manner is more favorable for seller and provides more secure to buyer. Buyer can exercise his right individually and without any consent (it`s particularly significant in case of long term options).

Options are often applied by strategic investors: during purchase period seller holds his share, which will be sold afterwards on demand by buyer.

Stock option is a widely spread instrument with some peculiarities in investment field. In this case option is a derivative security, that have derived nature: the security derives its value from underlying assets expressed in the form of securities identified with generic characteristics.

The term “security option” refers to equity security granting its holder the right to buy a certain quantity of shares within a specified period and/or depending on the circumstances determined in security at determined price. “Security option” is a registered security.

Attribution of “security option” to investment securities is a controversial point. We hold the opinion that due to the legal nature of option it can not be referred to investment securities, because it creates a right, not an obligation to buy equities (an exchange assets). Moreover, performance takes place only on demand (by option holders). The right to buy securities on its own terms is only a legal prerequisite to investment, but not the investment in principle, implicated inputs with the purposes of property and non-property rights emergence.

On the basis of the above it can be concluded that the introduction of option as a legal notion was of great demand in Russian Law. Option can be used in different fields and relations by various types of contracting parties unless it contradicts the law. The lack of listed restrictions is the doubtless advantage of option model, providing an opportunity to create new legal relationships based on it.

Ekaterina Pazemova

Master of International Private Law

Legal and Tax Advisor

Saint-Gobain Group

Other Articles on Topics