This article continues the series of publications about the system of taxation with value-added tax in the European Union. In this issue, we look into a matter of tax violations related to VAT evasion.

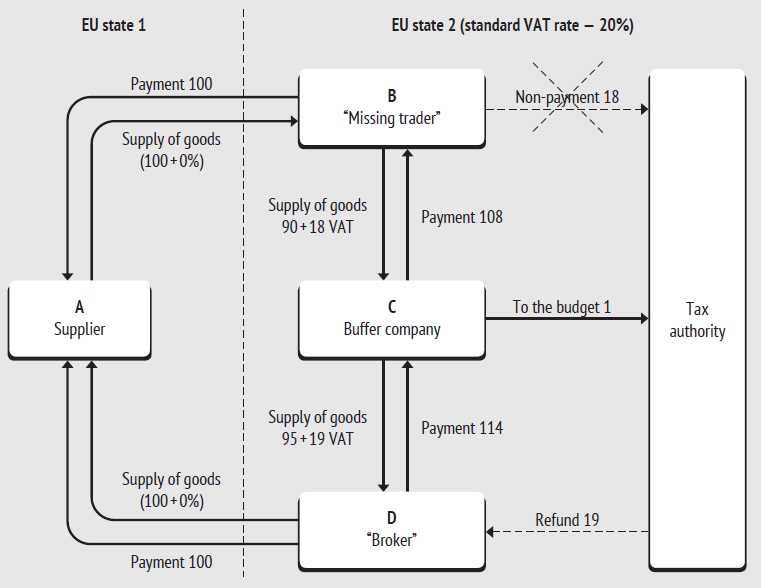

In most cases VAT evasion schemes exploit the privilege stipulated by law for transactions concerning cross-border supply of goods when goods are transported from one state of the European Union to the other (hereinafter – the IC supply). Such transactions are taxed at the rate of 0%1. At further resale, the cost of such goods does not include the amount of tax paid to the seller at the purchase of goods from the other state. It allows reselling them at the price more attractive than the current market prices. The participant of such fraud, who performed such resale, accumulates the amount of VAT paid by the buyer at the standard rate, fails to declare it and “disappears” by the moment tax authorities detect underpayment to the budget. Hence the name given to this type of fraud schemes – missing trader intra-community fraud (MTIC fraud)2. Apart from the “disappearing” intermediary, several firms acting as a “buffer” in the resale chain usually participate in the fraud before the goods are again exported from the country to the other EU state. The second IC supply is again taxed at the rate of 0%, therefore, the so-called “broker” carrying out the IC supply accumulates the input VAT, which is not set off against by the VAT amount charged to the buyer. The “broker” becomes entitled to VAT refund from the budget in the amount, which he/she has paid to the previous participant of the fraud.

To implement such illegal operations, expensive, but small-sized products, such as mobile phones, processors, and etc. are mostly used. Services are not a convenient instrument as expensive services involve a high degree of professionalism of the principal, who is not inclined to risk his/her reputation for the sake of short-term illegal profits3.

Carousel fraud has its name because goods, during the sale of which a tax violation is committed, are not sold to the ultimate consumer, but repeatedly “circulate” among the participants of the fraud, and thus increase the amount of tax underpaid to the budget.

A large number of buffer companies may be involved in the resale chain, and some of them may not even be aware that they are participating in the fraudulent scheme. By the moment the tax authority reveals the scheme, Company B (see Figure 1), which has not declared the supply, “disappears”, and tax authority can compensate this non-payment by two means:

- Reject the refund claim made by the “broker” who has carried out the IC supply;

- Contest the 0% rate used by the “broker” at the IC supply.

In 2006 the European Court of Justice (ECJ) passed a judgment on the joint cases C-354/03, C-355/03, C-484/03 Optigen Ltd, Fulcrum Electronics Ltd, and Bond House Systems Ltdv Commissioners of Customs and Excise [2006] ECRI-483, the subject matter of which was the right to refund VAT by the “brokers” who turned out to be the participants of a fraudulent scheme. The UK tax authority denied the refund citing the fact that illegal transactions, regardless of the presence or absence of fault of their participants, could not be deemed economic transactions subject to VAT taxation. The European Court of Justice took up a slightly different stance, which was that the right to VAT compensation could not be canceled because there was a tax violation committed in the supply chain, a part of which was the transaction under consideration, except the case when the taxpayer knew or should have known about such violation. Thus, the so-called knowledge test, which is aimed at revealing the negligence of the taxpayer as a basis for denial in refund, has been developed.

The same year the European Court passed a judgment, where it detailed its stance on this case (C-439/04 and C-440/04, Kittel v Belgian State and Belgian State v Recolta Recycling [2006] ECRI-6161). It was specified that the taxpayers taking all precautionary measures which could have been reasonably required from them to prevent their participation in the fraudulent scheme, may rely on the legality of their transactions without any risk of losing the right to the VAT refund. Thus, the role of the prior due diligence of the counterparty before the execution of an economic transaction has been strengthened. Moreover, the court ruled that the taxpayer who knew or should have known the fact that in the course of conclusion of the purchase transaction he/she was involved in the VAT evasion scheme, shall be deemed a participant of such scheme regardless of whether he/she received an economic benefit from such transaction or not.

If it is impossible to prove the taxpayer’s lack of diligence in the course of purchase of the goods circulating in carousel scheme and to deny the refund, the tax authority may question the 0% rate in case of the repeated IC supply. Reduced rates may be applied only on the condition that the goods have really been transported to the other EU state4. It was ruled that the burden of proving the legality of the application of the reduced rate shall rest upon the taxpayer who cannot refer to the system of interaction of the EU tax authorities, within which a request on actual transportation of goods across the border must be sent5. The European Court of Justice specified that if a tax authority of the state, where the goods were sent from, received a reply to the request containing the confirmation of the fact that the buyer has declared the transaction as IC purchase, it is not a proper evidence of transportation of goods across the border. Thus, in order to minimize the risks in the event of application of the 0% rate to an IC supply, the supplier must have confirmation of the fact of transportation of goods, for example, an international consignment note (CMR).

What are the limits of due diligence of the counterparty, which the taxpayer must carry out in order not to be deprived of the rights granted by law? The Court has drawn up a general principle of legal certainty and proportionality, according to which the application of legal regulations should be predictable for the taxpayer. Thus, the tax authority shall not be entitled to deny application of the 0% rate to the IC supply and credit additional taxes because the registration number of the counterparty as a VAT payer in the other state has been revoked with retroactive effect, but it has been valid at the time of the transaction6.

In most cases, at the detection of the “carousel scheme” the goal of the tax authority is to compensate the VAT amount, which has not been paid at the beginning of the chain by the supplier, who has “disappeared” by that moment, by denying the recognition of fundamental rights (whether it is the right to deduction or the right to apply the reduced rate) of the taxpayer standing “at the top or at the bottom of the chain”7.

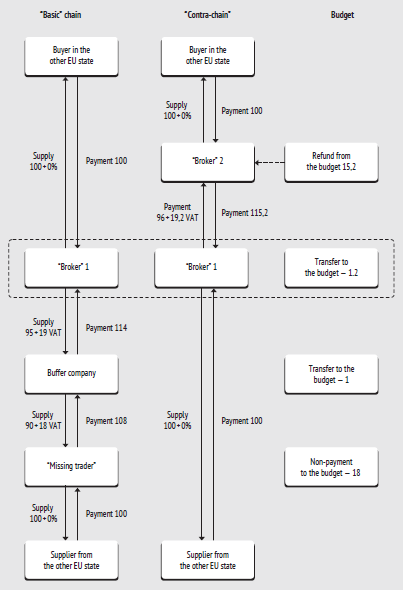

However, the schemes used in practice often include several such chains aiming at paying off the output VAT in one of them by the input VAT in the other chain. The “basic” chain, where the “broker” purchases the goods at the standard rate and accumulates the input VAT, and then sells them to the other EU state at the 0% rate, and a parallel contra – chain, where the same participant purchases the goods at the 0% rate and resells them further at the standard rate, thus generating the output VAT from this resale, are used.

The “contra-chain” is used if the tax authority denies refund of the input VAT in the “basic” chain on the abovementioned grounds. Then the “broker 1″ purchases the other batch of goods at the 0% rate in the other EU state and resells them to the ” broker 2″ at the standard rate, thus generating the output VAT, which is set-off against the input VAT in the “basic” chain. Now ” broker 2″ claims his/her right to compensation of the amount of tax paid by him/her for the purchase of “clear” goods, which have not been the subject matter of transactions of the “missing trader ” in the contra – chain”. There is a legal dispute as to whether the tax authority is entitled to deny the refund to the person not involved in the resale chain from the “missing trader”.

According to judicial practice, they are mostly entitled. There are no precedents of settling such disputes at the European Court of Justice level, which means that national courts do not consider them fundamentally new and unregulated by existing legislation, and thus settle them by analogy of law. In the Fonecomp Limited case8 the court of the first instance ruled that the company had not concluded transactions with the “missing trader” (Softlink Limited) and the “broker” that organized the “contra chain” (Klick Limited), but it was related to the “missing trader” as follows:

- The goods that Fonecomp Limited purchased (mobile phones) belonged to the same batch of goods, which Klick Limited was reselling;

- The output VAT was set-off against the input VAT in the returns of Klick Limited.

The Court of Appeal dismissed objections of Fonecomp Limited and did not find in the precedents of the European Court of Justice any indications to the fact that the principle of reasonable diligence of the participant in the transaction, developed in the Kittel v Belgian State case, should be interpreted narrowly in respect to the only supply chain where the party to the case participated. The Supreme Court of the United Kingdom dismissed the appeal of Fonecomp Limited. The Court took the position, under which the participant of the “anti-chain” can also be liable for events of the “basic” chain, if the real purpose of transactions concluded in the “anti-chain” is to hide the fraudulent scheme. The expression “knew or should have known about the violation” was interpreted in such a way that it is enough to be aware of the fact that the concluded transaction is related to the fraudulent VAT evasion to lose the right to refund.

The practice of fighting against the VAT evasion in the European Union has developed the principle that the rights granted by law of the European Community cannot be used for the purposes of abuse or fraud9. The key element of this approach is the “test” of knowledge of tax violation. If the taxpayer has failed to take reasonable measures to identify a fraudulent component of economic transaction, his/her right to compensation of the input VAT or application of the reduced rate may be contested by the tax authority.

- Article 138 (1) of Directive 2006/112/ ЕС.

- https://www.gov.uk/hmrc-internal-manuals/vat-fraud/vatf23520

- Joep Swinkels, Carousel Fraud in the European Union// International VAT Monitor, Mar.-Apr. 2008, p.103.

- Article 138 (1) of Directive 112/2006/ ЕС.

- Twoh International BV v. Staatssecretaris van Financien, C-184/05.

- Mecsek-GabonaKft. v. NemzetiAdó- ésVámhivatalDél-dunántúliRegionálisAdóFőigazgatósága, C-273/11.

- Bonik EOOD v DirektornaDirektsia ‘Obzhalvaneiupravlenienaizpalnenieto’, C-285/11.

- Fonecomp Limited [2015] EWCA Civ 39.

- Redmar Wolf,Mecsek-Gabona: The Final Step of the ECJ’s Doctrine on Reliance on EU Law for Abusive or Fraudulent Ends in the Context of Intra-Community Transactions// International VAT Monitor, Sep.-Oct. 2013, p.286.

Yana Karausheva

Ex-Junior Lawyer

Tax and Legal Practice

Korpus Prava (Russia)

Other Articles on Topics