On entry into force of Article 269 of the Tax Code of the Russian Federation, interest rate setting became difficult for accountants. Meanwhile, legislators update the procedure for rate setting on an annual basis and create new criteria and reasons to exclude part of paid charges interest that decrease the taxable base for the corporate profit tax.

The procedure for interest rate setting for controlled transactions is reasonably described and explained by legislators, whereas the procedure for interest rate setting for controlled indebtedness remains unclear.

Thus, controlled indebtedness is outstanding indebtedness of a Russian company taxpayer regarding the following debt obligations of this taxpayer:

- Debt obligation to a foreign person affiliated with a Russian company taxpayer on the following basis:

- A foreign company debtee directly or indirectly participates in a debtor company and has its share of more than 25%;

- A foreign natural person debtee directly or indirectly participates in a debtor company and has its share of more than 25%;

- Foreign companies and foreign natural persons are consequent shareholders of a Russian company debtor (a foreign person is one of them), and direct interest share of every preceding person in every following company equals more than 50%.

- Debt obligation to a person affiliated with the abovementioned foreign person on the following basis:

- A company or a natural person directly or indirectly participates in a foreign company and has its share of more than 25%;

- The same person directly or indirectly participates in a debtor company and a foreign company and has its share in each company of more than 25%;

- Companies and natural persons are consequent shareholders of a foreign company (a debtee is one of them), and direct interest share of every preceding person in every following company equals more than 50%.

The abovementioned outstanding indebtedness is not considered controlled indebtedness for a Russian company taxpayer on simultaneous fulfilment of the following conditions:

- Debt obligation to a Russian company or a natural person that are tax residents of the Russian Federation arose during the accountable (taxable) period;

- A Russian company debtor or a natural person debtor does not have any outstanding indebtedness for comparable debt obligations to a foreign person mentioned in clauses 1 or 2 during the accountable (taxable) period.

Therefore, in case an affiliated foreign person independently provides a Russian company with a loan (does not act as an intermediary between a foreign person and a Russian company), this indebtedness is not considered controlled and interests for such indebtedness are not subject to rate setting.

- Debt obligation for which a foreign person debtee mentioned in clause 1 and/or its affiliated person mentioned in clause 2 serve as warrantors, guarantors or otherwise guarantee to secure this debt obligation of a Russian company taxpayer.

The mentioned outstanding indebtedness is not considered controlled for a Russian company taxpayer on simultaneous fulfilment of the following conditions:

- Debt obligation arose to a company which is a bank (including organizations considered as banks in accordance with legislations of foreign countries) non-affiliated either with a taxpayer or persons that act as warrantors, guarantors or otherwise guarantee to secure a debt obligation of a taxpayer;

- From the date of taxpayer’s debt obligation no termination (fulfilment) of the mentioned debt obligation occurred either for the principal amount or for the interest payment on behalf of persons that act as warrantors, guarantors or otherwise guarantee to secure the mentioned debt obligation.

Thus, if an affiliated person is a guarantor of a bank loan, but a Russian company fulfills its loan obligations, indebtedness is not considered controlled and interests for such indebtedness are not subject to rate setting.

To sum it all up, if a company gets a loan from an affiliated foreign person or an affiliated person of such a foreign person, or in case such persons act as warrantors or guarantors of a transaction (excluding the abovementioned specific cases), it is required to analyze the necessity for payable interest rate setting.

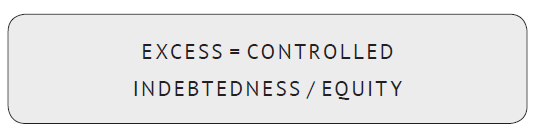

In case the amount of controlled indebtedness of a taxpayer is more than 3 times larger than a difference between total assets and total obligations of this taxpayer (total equity) as of the last day of an accountable (taxable) period, one shall calculate and use capitalization rate in order to define interest limit due to be recognized in expenses.

In order to calculate the amount of controlled indebtedness of a taxpayer, one shall consider amounts of controlled indebtedness for all obligations of this taxpayer in total.

Thus, if a company has several debt obligations that qualify as controlled indebtedness, in order to calculate the excess of indebtedness over total equity one shall not calculate the amount for each obligation, but summarize all controlled indebtedness.

For calculation purposes total equity is taken from entry 1300 of Balance sheet (Equity) at the reporting date.

In case the amount of controlled indebtedness of a taxpayer is less than 3 times larger than company’s equity, one shall not perform payable interest rate setting.

In case the amount of controlled indebtedness of a taxpayer is more than 3 times larger than company’s equity, one shall calculate interest limit due to be recognized in expenses.

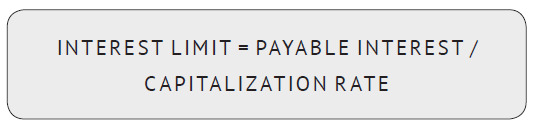

Interest limit on controlled indebtedness due to be recognized in expenses is calculated by a taxpayer as of the last day of each accountable (taxable) period by dividing interests charged by this taxpayer in each accountable (taxable) period from controlled indebtedness by capitalization rate calculated as of the last day of the relevant accountable (taxable) period.

Furthermore, in case of changes in capitalization rate in the following accountable period or according to the results of a taxable period in comparison with preceding accountable periods, interest limit on controlled indebtedness due to be recognized in expenses for the preceding period is not subject to changes.

It is worthwhile noting, that the abovementioned ban of interest changes for preceding periods appeared in the Tax Code only at the beginning of 2016 (entered into force from 2017). Previously the procedure for interest limit calculation was described in the Tax Code in fewer details and many people recalculated interest limit for preceding periods according to the decrease of controlled indebtedness.

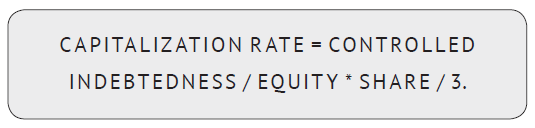

Capitalization rate is calculated by dividing the relevant outstanding indebtedness by the equity proportionate to the share of an affiliated foreign person, and dividing the resulting number by 3.

Thus, capitalization rate formula is as follows:

Meanwhile, equity in the abovementioned formula differs from the initial one. Upon the calculation of equity one shall not include debt obligations on taxes and duties, as well as current obligations on tax and duties, set-offs, installment payments and investment tax credit. It means that equity shall be decreased by tax and duties liabilities.

Expenses include interests on controlled indebtedness at the amount not exceeding interest limit, but not more than accrued interests.

Thus, payable interests are partially not subject to profit taxation. However, it doesn’t cover the whole additional tax burden.

Positive difference between accrued interests and interest limit for taxation purposes is recognized as dividends paid to a foreign person. Thus, a taxpayer shall act as a tax agent in relation to a foreign company and pay the corporate profit tax from the “dividends” paid.

The abovementioned legislative provisions are designed to prevent Russian business from large foreign loans. Unlike general provisions of Article 269 of the Tax Code, interest limit on controlled indebtedness is not calculated on the basis of interest rate of loan obligations, but from the amount of loan and the correlation between equity and debt capital.

Interest limit calculation is a multi-step and complicated procedure. However, considering the fact that legislators do not exclude it from the Tax Code and actually try to elaborate and explain it, the procedure for interest rate setting for controlled indebtedness must be followed.

Other Articles on Topics