Exchange differences arise in accounting and tax accounting, and also affect the amount of taxes of the organization. The purpose of this article is to consider the procedure of the impact of exchange differences on values of assets and liabilities in accounting, on the VAT tax base and the tax base for income tax as well as on the profit of CFCs.

Let us compare the regulations established for the calculation of exchange differences in accounting and tax accounting

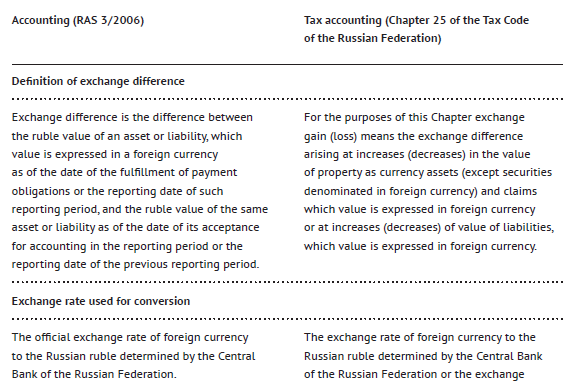

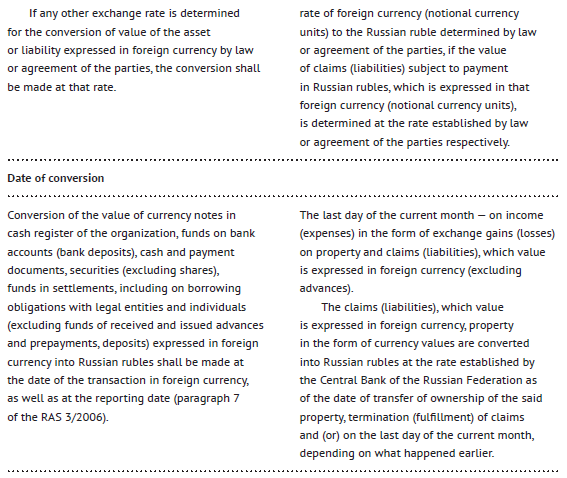

What are the differences?

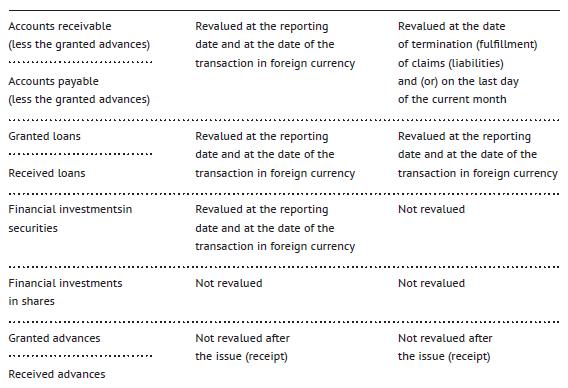

Thus, as of the beginning of 2017 there is only one significant difference between the procedure of formation of exchange differences in accounting and in tax accounting. In tax accounting, the value of securities denominated in foreign currency is not revalued, while the same (except shares) is revalued in accounting.

It is also possible to determine the difference in the date of periodic revaluation. In tax accounting, the periodic revaluation is carried out for the last day of the current month, while the same is made for the reporting date in accounting. The date on which the accounting (financial) statements are made (the reporting date) is the last calendar day of the reporting period.

The reporting period for annual accounting (financial) statements the (reporting year) is the calendar year – from January 1 till December 31 inclusive, except the cases of incorporation, reorganization and liquidation of the legal entity.

The reporting period for interim accounting (financial) statements is the period from January 1 till the reporting date for which the intermediate accounting (financial) statements are prepared, inclusive.

There are currently no general requirements for preparation of the interim accounting statements, therefore periodic revaluation of the value of assets and liabilities, the value of which is expressed in foreign currency, may be basically made once a year. But usually the revaluation is made monthly, just like in tax accounting (less often – quarterly), although the accounting policy does not stipulate the interim accounting statements.

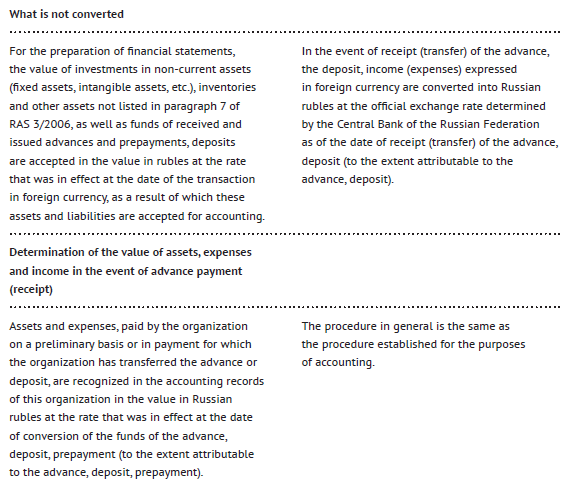

Comparison of the need for revaluation of various assets and liabilities, as well as the procedure of formation of income and expenses in accounting and tax accounting

Exchange differences and profit of controlled foreign companies

When calculating the profits of the CFCs the exchange differences are not taken into account. It follows from the recent explanations of the Ministry of Finance of the Russian Federation No. 03-12-11/2/7395 dated February 10, 2017.

According to the Ministry of Finance of Russia, in calculation of the share of the income specified in paragraph 4 of Article 309.1 of the Tax Code of the Russian Federation for the period, for which the foreign organization prepares financial statements for the fiscal year, the amounts of exchange differences on purchase and sale of foreign currency and the exchange differences resulting from revaluation of assets and liabilities of the controlled foreign company, which are recognized in the Statement of Profit and Loss according to applicable standards of preparation of financial statements, are not taken into account in the total amount of the corporate income according to such financial statements.

VAT from exchange differences

The exchange differences do not participate in the formation of the VAT tax base. Let us consider the example of how it works.

Let us consider the transaction of purchase of goods which costs 118 euros, including VAT 18 euros. The payment is made at the exchange rate of euro on the date of payment. The agreement stipulates the 50% prepayment. Euro exchange rates:

- As at the date of prepayment – 70;

- As at the date of shipment from the seller’s stock – 71;

- As at the date of delivery to the buyer’s stock – 72;

- As at the date of payment after the delivery – 68.

- Transfer of prepayment debit 60 credit 51 – 4,130 RUB (118*0.5*70).

- Shipping:

- The invoice will be issued for 4,130 RUB + (118*0.5*71) = 8,319 RUB, including VAT 1,269 RUB.

- Delivery of the goods:

- Debit 10 credit 60 = 7,100 RUB (100*0.5*70) + (100*0.5*72);

- Debit 19 credit 60 = 1,269 RUB (under the invoice).

- Revaluation and additional payment:

- Debit 60 credit 91 – 227 RUB – revaluation of accounts payable (7,100+1,269-4,130) – (118*0.5*68);

- Debit 60 credit 51 – 4,012 RUB – additional payment to the supplier.

According to Paragraph 4 of Article 153 of the Tax Code of the Russian Federation, if in sales of goods (works, services), property rights under agreements, the payment obligation of which is provided in RUB in the amount equal to a certain amount in foreign currency or notional currency units, the moment of determination of the tax base shall be the day of shipping (transfer) of the goods (works, services), property rights, when determining the tax base, the foreign currency or notional currency units shall be converted to RUB at the exchange rate of the Central Bank of the Russian Federation as at date of shipping (transfer) of the goods (works, services), transfer of property rights. In subsequent payment of the goods (works, services), property rights the tax base is not adjusted. The differences in the tax amount arising with the taxpayer-seller in subsequent payment the goods (works, services), property rights are taken into account as non-operating income according to Article 250 of the Tax Code of the Russian Federation or as non-operating expenses according to Article 265 of the Tax Code of the Russian Federation.

For the purposes of applying VAT, the date of shipment of the goods shall be the date of the primary execution of the initial document executed in the name of the buyer or transporter of the goods (Letter from the Federal Tax Service of Russia No. ЕД-4-3/21217@ dated December 13, 2012).

When determining the tax base on the day of shipping of goods (performance of works, provision of services) against the earlier full prepayment in RUB, the tax base shall be determined on the basis of the received full prepayment in RUB without conversion at the rate of the Central Bank of the Russian Federation as at the date of shipping (Letter from the Ministry of Finance of Russia No. 03-07-15/70 dated July 06, 2012).

Thus, VAT is not adjusted in revaluation of debts.

Igor Chaika

Ex-Managing Director

Audit Practice

Korpus Prava (Russia)

Other Articles on Topics

See Also Articles from the Issue

Subsidiary Liability of Controlling Persons at Bankruptcy

The notion of a "controlling person" established by the Federal Law "On Bankruptcy" is quite broad, and its definition, with a sufficient evidence basis, may include a wide range of persons - participants, shareholders, general director, its deputies, members of the board of directors, chief accountant, beneficial owner, as well as other persons.

April 10, 2017

Minorities of All Countries, Unite!

As it is known, in the system of corporate relations the central player is the shareholder. In fact, all corporate legislation is, to one degree or another, aimed at ensuring the shareholder's rights for the development of a healthy corporate climate in Russia. Russian corporate legislation is currently experiencing a period of rapid development. Numerous innovations in the field of protection of the shareholders’ rights confirm this fact.

April 10, 2017

Same Old Story. Unified Social Tax

As we all know, from 2017 tax authorities have resumed the administration of insurance premiums, for which reason budget classification codes and the form of insurance premiums calculation have been changed. There are many questions indeed, because any changes create a misunderstanding between the administrative authority and the payer.

April 10, 2017

Reconnaissance in Force

It has been three years since the Law On Controlled Foreign Companies was adopted. The law has become an integral part of the Tax Code of the Russian Federation. Many things have changed for the past three years. In the course of adoption of amendments to the law, certain provisions of laws on controlled foreign companies had to be changed.

April 10, 2017

Inheritance of Property Abroad

Modern civil law system provides two options of transfer of property of the deceased owner to his/her heirs. If the person has not made any will, his/her property will be transferred to his/her heirs in the manner provided for inheritance by law.

April 10, 2017