In the upcoming several years radical revision of accounting standards valid in the Russian Federation is planned.

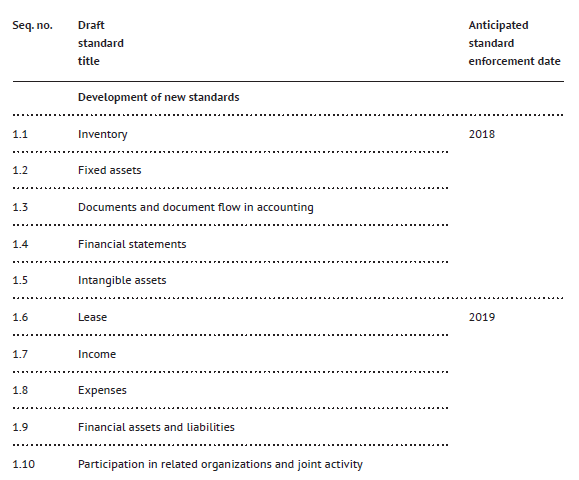

On the website of the Ministry of Finance of the Russian Federation there is a program for the elaboration of new accounting standards for 2016-2018. It stipulates both the development of new federal accounting standards and modification of current accounting provisions.

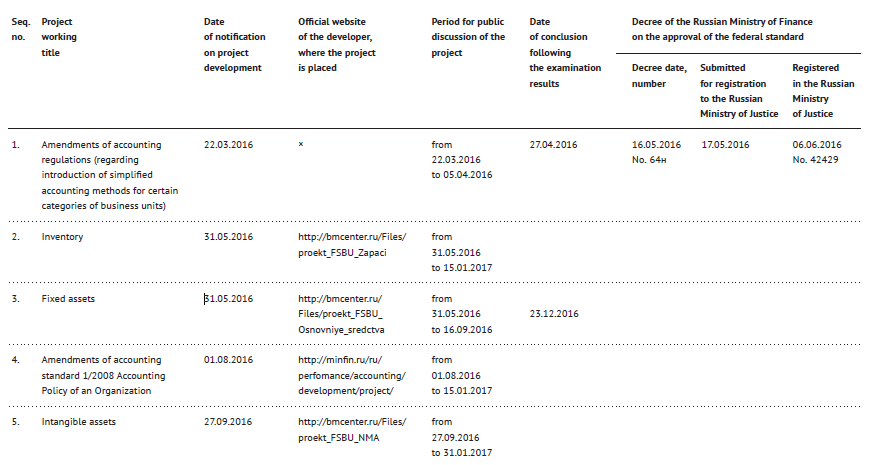

On December 27, 2016 on the website of the Ministry of Finance of the Russian Federation there was information placed on the status of the accounting standards development.

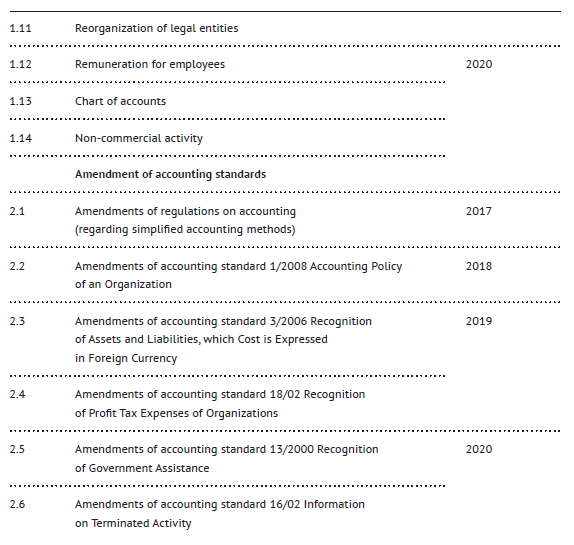

In November 2016 on the website of the Russian Ministry of Finance there were draft amendments of accounting standard 1/2008 Accounting Policy of an Organization published.

The draft stipulated introduction of the following rules:

- If a business unit having subsidiaries elaborates and approves its own standards binding upon such subsidiaries, a subsidiary chooses accounting methods based on such standards.

- An organization, which discloses consolidated financial statement drawn up in accordance with International Financial Reporting Standards or financial statement of an organization without a group, is entitled to follow federal accounting standards at developing accounting policy subject to the International Financial Reporting Standards. If application of an accounting method set forth in the federal accounting standard leads to inconsistency of the accounting policy of the organization with the requirements of the International Financial Reporting Standards, the organization is entitled to refrain from using such method.

- If there are no accounting methods specified in federal accounting standards regarding a certain issue, an organization elaborates an applicable method based on the International Financial Reporting Standards. If there is also no accounting method specified in the International Financial Reporting Standards for such certain issue, an organization elaborates an applicable method based on federal accounting standards for similar and (or) related issues. If there are no federal accounting standards for similar and (or) related issues, an organization elaborates an accounting method independently.

- If an accounting regulation specifies an opportunity of its voluntary application by organizations prior the maturity date of its mandatory application (early application), an organization applying such regulation early shall disclose such fact in its financial statement.

New standards shall be adopted in 2017: Inventory, Fixed Assets, Documents and Document Flow, Financial Statement and Intangible Assets. Application of standards is scheduled from 2018.

New accounting standard Fixed Assets shall replace accounting standard 6/01.

In respect of property with shelf life above one year, a company shall be entitled to resolve independently whether to recognize it as fixed assets or not. It will allow considering property with the cost above 100 000 rubles as in tax accounting, i.e. eliminating discrepancy.

In respect of other standards, it is too soon to speak about amendments because they have not passed public discussion and examination yet.

Moreover, standards will be adopted, which were previously absent from the accounting law of the Russian Federation, but were part of IFRS.

Igor Chaika

Ex-Managing Director

Audit Practice

Korpus Prava (Russia)

Other Articles on Topics

See Also Articles from the Issue

Audit Under Russian and International Rules

Until last December there had been a threat of monopolization of the audit market by creating a single self-regulatory organization controlled by the Ministry of Finance of the Russian Federation. Fortunately, it did not happen. Two self-regulatory organizations retain control over the activities of auditors.

January 20, 2017

Q&A: Specific Issues of Common Reporting Standard (CRS)

Automatic information exchange suggests automatic transfer of certain information from the disclosing party of a foreign state to Russian authorities. Then the authorities will work with such information in ordinary course using administration measures and methods set forth in the national law of the Russian Federation.

January 20, 2017

Latest Changes in the Legislation of Foreign Countries

In 2006 The International Business Companies Act 2016 (hereinafter – the Act) superseding The International Business Companies Act 1994 was published in the Seychelles. This act has introduced a number of changes, among which there are two main requirements – submission of information about directors and ultimate beneficiary owners – beneficiaries.

January 20, 2017

Complicated Life of the “Simplified” and Other Changes in the Tax Legislation

The year 2016 was full of events in the field of geopolitics, which partly shaded the considerable effort that our legislator applied throughout the year in an effort to create a legal framework that meets today's challenges and trends in Russia. Such efforts can be indeed considered significant, because this year the State Duma set a record: 6 165 bills were considered.

January 20, 2017

Search for the Actual Income Recipient Continues

The supervisory authorities are paying more attention to the practical application of the concept of the actual income recipient. Everyone has heard the recent cases against such companies as "Northern Kuzbass" (A27-7455/2010), "Naryanmarneftegas" (A40-1164/2011), "OriflameCosmetics" (A40-138879/2014), etc.

January 20, 2017

Even If You Sit on the Stream Bottom, You Cannot Be a Fish

On July 5, 2016, the European Commission published a document-proposal with amendments to the Fourth EU Directive on the prevention of the use of the financial system for money laundering or terrorism financing purposes, known as 4AML.

January 20, 2017