It has been three years since the Law On Controlled Foreign Companies was adopted. The law has become an integral part of the Tax Code of the Russian Federation. Many things have changed for the past three years. In the course of adoption of amendments to the law, certain provisions of laws on controlled foreign companies had to be changed. Other provisions had a variety of unclear explanations of regulatory bodies which contained conflicting opinions.

As a result, according to the provisions of tax laws and the latest explanations, the duties of a tax resident of the Russian Federation regarding participation in a foreign company are as follows:

Submission of notices of participation in a foreign structure

Tax residents of the Russian Federation are under obligation to inform a tax authority of the Russian Federation about their participation in foreign organizations and foreign structures with no corporate status (trusts) not later than within 3 months from the date of occurrence or change of such participation interest. Please be aware that the deadline for submitting the notice has changed, previously it was “not later than within 1 month from the date of occurrence or change of such participation interest”. The notice shall be submitted only at the moment of occurrence or change of the participation interest (including termination of participation).

Failure to submit such notice within the established deadline as well as submission of false information is punishable by the fine of 50 000 Russian rubles concerning each foreign organization.

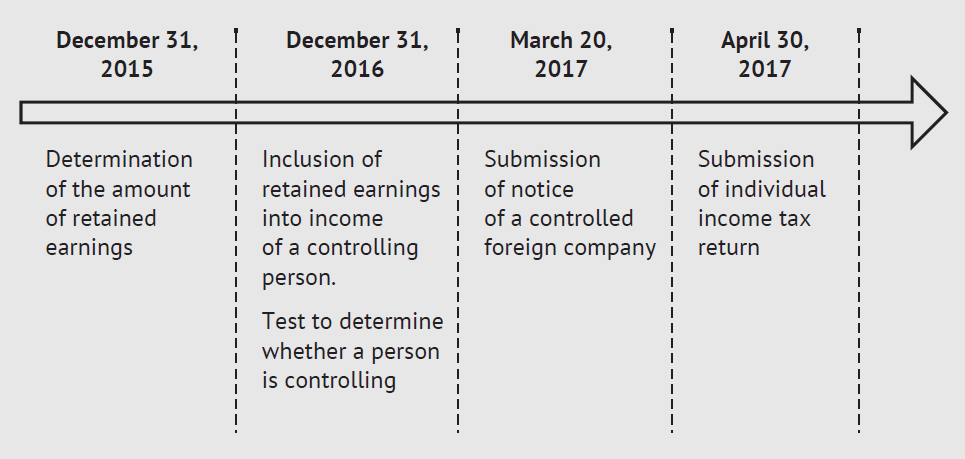

Submission of notice of controlled foreign company

If a foreign organization, which a tax resident of the Russian Federation is a direct or an indirect participant in, is deemed controlled according to the Tax Code of the Russian Federation, in addition to a single notice of participation, the resident of the Russian Federation shall submit annually a notice of a controlled foreign company.

The following persons/entities – tax residents of the Russian Federation – shall submit the notice of CFC:

- Individuals or legal entities whose participation interest in a foreign organization is more than 25%, or

- Individuals or legal entities whose participation interest in this organization (for individuals – jointly with their spouses and minor children) is more than 10%, if the participation interest of all entities deemed to be tax residents of the Russian Federation in this organization is more than 50%.

The notice of CFC shall be submitted not later than on March 20 of each year following the tax period when retained earnings of the CFC is taken into account at determining the tax base for a controlling person.

Also please be aware that the position of the Ministry of Finance is that taxpayers shall inform a tax authority on controlled foreign companies in respect of which they are controlling parties, regardless of the amount of income received by them as profit of the respective controlled foreign companies.

Failure to submit such notice within the established deadline as well as submission of false information is punishable by fine of 100 000 Russian rubles concerning each foreign organization.

Payment by a controlling person of tax from retained earnings of a controlled company

If the profit of a controlled foreign company is more than 10 000 000 Russian rubles (profit of the controlled foreign company for 2015 is 50 000 000 Russian rubles, and 30 000 000 Russian rubles for 2016 under transit provisions), the profit of the controlled foreign company shall be taken into account when determining the tax base for the tax period on the relevant tax.

At determining the profit of the controlled foreign company, income as dividends paid out by Russian organizations are not taken into account, if the controlling person of this controlled foreign company has an actual right to such income.

Thus, when the income of the controlled foreign company includes the amount of dividends, the amount of such dividends does not reduce the profit of the controlled foreign company for the purposes of applying threshold values1.

Concerning loss it has been established that if a loss is determined according to the financial statements of the controlled foreign company prepared in accordance with its personal law for a fiscal year, the specified loss may be carried forward without any restrictions and taken into account at determining the tax base of this company.

In addition, the loss incurred by the controlled foreign company before January 1, 2015 according to the financial statements prepared in compliance with its personal law may be carried forward in the amount not exceeding the amount of the loss for the three financial years preceding January 1, 2015 and may be taken into account when determining the tax base of this company.

In view of the fact that the carry-forward of the loss incurred by the controlled foreign company is the right of the controlling person, the specified losses do not reduce the amount of profit of the controlled foreign company for the purposes of applying threshold values.

At the same time, it is not uncommon when the company’s fiscal year does not coincide with the calendar year. In this case, if the period, for which the financial statements of a controlled foreign company is prepared, begins, for example, on October 1 of each year and ends on September 30 of each year:

- The profit of the fiscal year from October 1, 2014 to September 30, 2015 is not taken into account in determining the profit of the organization (income of an individual) received by the taxpayer recognized as the controlling person of the relevant controlled foreign company;

- The profit of the financial year from October 1, 2015 to September 30, 2016 is taken into account when determining the profit of the organization (income of an individual) received by a taxpayer recognized as the controlling person of the relevant controlled foreign company in 20172.

The following explanation has been given concerning documentary proof of the amount of profit (loss) of the controlled foreign company.

The taxpayer-controlling person shall submit a tax return on tax, when determining the tax base on which the profit of the controlled foreign company is taken into account, together with the following documents:

- Financial statements of the controlled foreign company for the period, for which the profit is taken into account when determining the tax base for corporate income tax, in respect of which the tax return is submitted, or other documents in the event of absence of the financial statements;

- Audit opinion on the financial statements of the controlled foreign company, if, in accordance with the personal law or the constituent (corporate) documents of this controlled foreign company, compulsory audit of these financial statements is established or the audit is carried out voluntarily by the foreign organization. However, the audit opinion shall not be submitted if the profit of the controlled foreign company is determined by the data of its financial statements in accordance with Chapter 25 of the Tax Code of the Russian Federation.

According to the Ministry of Finance of Russia, the taxpayer-controlling person’s responsibility regarding the submission of tax reports of the controlled foreign company together with tax declaration on the tax, which reflects the profit of the controlled foreign company, to a tax authority is not established since the documents attached to the tax declaration are established by Article 25.15 of the Code. The specified provision of Article 309.1 regulates the procedure for confirming the profit of the controlled foreign company in the event of tax control measures.

In addition, the documents confirming the calculation of the profit of the controlled foreign company are subject to translation into Russian to the extent necessary to confirm the calculation of the profit (loss) of the controlled foreign company. Moreover, the Code does not contain provisions concerning the need to obtain and submit to tax authorities notarization and apostilization of copies of documents confirming the existence of control, exemption of profit of the controlled foreign companies from taxation in the Russian Federation and calculation of their profit3.

Both tax authorities and taxpayers have worked in terms of explanations and a deeper understanding of the norms of tax laws, respectively, for the past three years. However, there are still many open issues as well as issues that are yet to arise, since business processes are very dynamic substance and it is difficult to predict what new challenges we will face in the future.

- Letter from the Ministry of Finance of the Russian Federation No. 03-12-10/1290 dated January 16, 2016.

- Letter from the Ministry of Finance of the Russian Federation No. 03-12-11/2/7395 dated February 10, 2017.

- Letter from the Ministry of Finance of the Russian Federation No. 03-12-11/2/7395 dated February 10, 2017.

Other Articles on Topics