Syndicated credit (loan) is a financial instrument, which provides for getting loan-based funding from several persons and sharing rights, obligations and risks attributable to lending among them. Federal Law No. 486-ФЗ dated 31.12.2017 “On Syndicated Credit (Loan) and Changes to Particular Legal Acts of the Russian Federation” became effective as of February 1, 2018, and basically laid the legal groundwork for its implementation in the Russian legal environment.

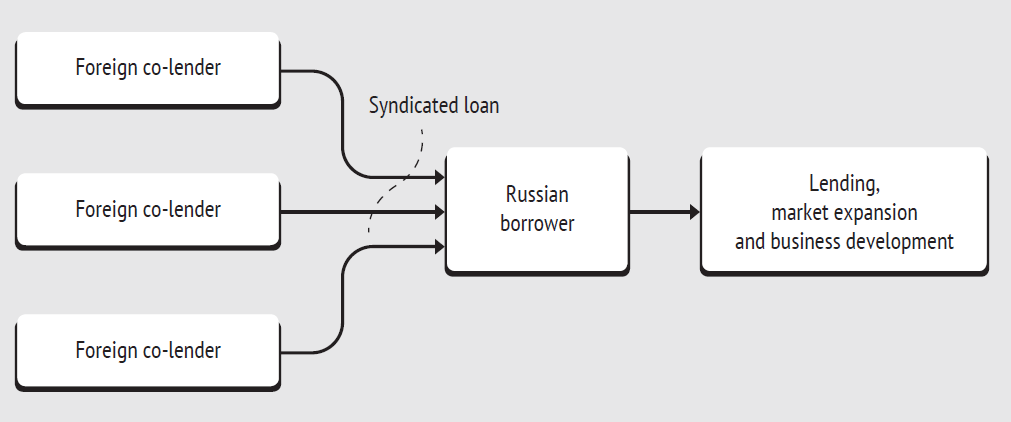

Syndicated loans and credits are granted to borrowers whose needs exceed financial resources of separate lenders.

Although loan granting by a group of lenders has never been banned as such, and was governed by the general law, granting of syndicated loans in accordance with the laws of the Russian Federation was considered an exception rather than a general rule.

Russian market of syndicated loans

In recent years, syndicated loans were granted on an active basis, but they were mainly governed by international agreements and foreign legislation. Participants of relevant legal arrangements were primarily large raw materials monopolies and banks with prevailing or full state participation. According to experts, Russian entities generally get syndicated loans either directly from foreign investors, or by integrating a specifically established foreign company into the funding plan.

The largest most renowned syndicated loans granted in recent years to Russian business representatives were as follows:

- Syndicated loan for USD 2 billion with the maturity of 5 years granted to OJSC Mechel in 2010;

- Syndicated loan for EUR 3.1 billion with the maturity of 16 years granted to NordStream consortium to implement Nord Stream project in 2010.

In 2017, grantees of the largest syndicated loans in Russia included such monopolies as Russian Railways, Norilsk Nickel, Uralkali, Siberian Coal Energy Company, RUSAL, Metalloinvest Holding Company. Significant grantees include only one commercial bank incorporated in Russia – Credit Bank of Moscow, and one IT-related representative – foreign members of VimpelCom-VEON group.

Russian commercial banks and large production holding companies are often granted syndicated loans by foreign investment banks and other financial institutions. They attract such funding for more efficient principal activities and expanding their network or business upgrade1.

In 2017, according to CBONDS ranking data, the largest arrangers of syndicated loans in CIS countries were Sberbank of Russia and Gazprombank. Thus, Sberbank holding its position in TOP-20 for seven years managed to arrange nine syndicated loans for the total amount of USD 645 million, which made up 4.11% of the total market of syndicated lending. Gazprombank made the ranking for the first time and forced out two other representatives from Russia, i.e. VTB and Alfa-Bank. During this period, it managed to arrange five deals amounting to USD 458 million, or 2.92% of the total amount of granted syndicated loans. For reference, ranking leader ING Bank arranged eighteen deals amounting to USD 1.383 billion, or 8.81% of the total market of syndicated lending2.

Growing attention to syndicated lending in Russia and under Russian legislation may have resulted from imposition and further expansion of sanctions against Russia. Sanctions made it significantly more difficult or even impossible for a number of entities to get funding from foreign banks. However, RBK experts agree that large borrowers will continue to get funding from foreign entities, though they will refocus on Chinese and other Asian lenders3. Nevertheless, this restriction of funding from European banks empowers Russian banks to enter the pool of arrangers or co-lenders for syndicated loans.

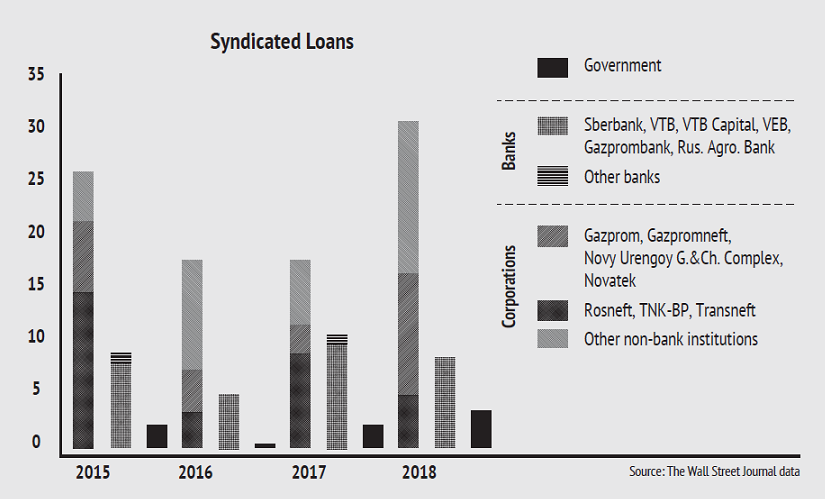

According to The Wall Street Journal estimates, in 2018, with the new Law effective the share of non-bank institutions possibly related to the private sector of the economy in this business shall significantly increase. The volume and proportion of participants in the Russian market of syndicated lending from 2015, and estimated figures for 2018 are presented in the chart below.

Legal regulation of syndicated lending before February 1, 2018

Up until recently, the Russian legislation had no law provisions governing rules and terms of such financial instrument as a syndicated loan. Syndicated lending was governed solely by general provisions of the Civil Code related to loan and credit agreements. However, it did not stop the Bank of Russia to adopt guideline regulations clarifying the procedure of relevant financial transactions4.

The key risk, as seen by experts in this case, deals with the qualification of relations between co-lenders as relations of partnership (cooperation), “and consequently, the risk of applying rules governing simple partnership agreements”. While describing major difficulties participants of lending syndicates may face in the legal vacuum environment, Dentons specialists note that “In this case a borrower could make claims against one of syndicate participants for the total loan amount granted by all its participants. Besides, there is no doubt that special rules for participants’ withdrawal from the partnership would hinder the development of the secondary market for credit claims, and imperative rules governing activities of partners would limit flexibility of lenders when making decisions”5. Considering total loan amounts granted in the relevant markets, even potential risks identified by analysts should be taken into account. However, we should note that we failed to discover any evidence verifying feasibility of these concerns. Despite everything, the absence of any legal base for the syndication of debts made it difficult to use their advantages in full.

Rules for syndicated lending since February 1, 2018

The new law provided regulation for legal arrangements of the largest and most significant syndicated loans and credits. Their significance is determined by the parties of legal arrangements, as well as the total amount of funding.

The law determines major differences between the syndicated credit (loan) and other types of loan-based funding. They include:

- Multiple persons acting as the lender.

- Coherence of lenders.

- Individual terms and conditions for loan granting by each lender.

- Specifics of the borrower and co-lenders.

- Obligatory interest charges and payments.

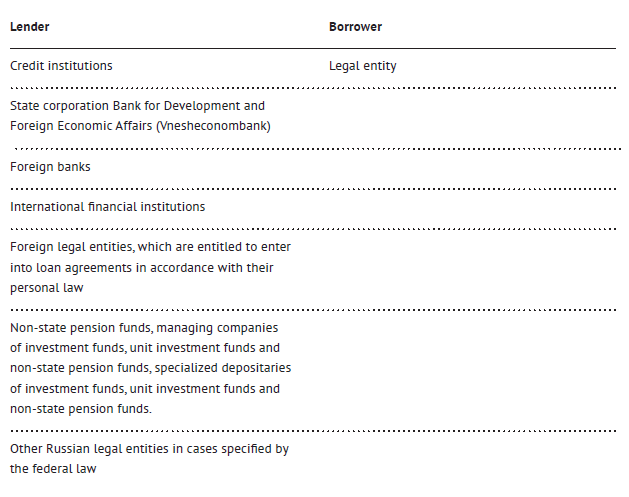

Parties of syndicated lending6

As seen from the list above, syndicated loan relations may be established only between legal entities, i.e. this instrument may be deemed strictly professional by default. Besides, it should be noted that it cannot be used for transactions with lenders registered in Russia, but not included in the list above. The last clause regarding other Russian legal entities is worded in a way that requires a special law reference for a particular legal entity to be able to grant syndicated loans. As of the date of this article, no such references were introduced, therefore, we may only speculate what items the legislator plans to include in this clause. Those are likely to be residents of any special economic zones or organizations of certain value as investment sources. However, we should note that foreign funding may be attracted from any foreign organizations, with sufficient legal capacity being the only requirement.

The law provides for several specific participants of syndicated loan agreements:

- Arranger of the syndicated credit (loan) is the future co-lender that bears fee-based liabilities for the preparation of a syndicated loan agreement. One or more persons may act as the arranger, and each of them will further become a lender7.

- Loan manager is one of the co-lenders that keeps the register of syndicated lenders, records all amounts of money granted to the borrower by each syndicated lender, communicates with the borrower, and performs any other organizational and technical functions required to exercise rights and obligations of the parties. Thus, it is the manager that receives on its account amounts of money from the borrower as the repayment of the principal amount and interest thereon, and distributes them among co-lenders in accordance with the requirements of the agreement. Unlike the arranger, the manager shall be appointed for any syndicated loan However, only a credit institution, state corporation Bank for Development and Foreign Economic Affairs (Vnesheconombank), foreign bank or international financial institution may act as the loan manager8. Therefore, it is impossible to enter into a syndicated loan agreement in the absence of at least one professional participant of the financial market.

- Pledge manager is the person acting for and behalf of all lenders which entered into the agreement, that undertakes to enter into the pledge agreement with the pledgor and/or exercise all rights and obligations of the pledgee under the pledge agreement9. The loan manager may act as the pledge manager, if it is duly authorized by the syndicate of lenders10.

The future of syndicated lending

According to the statistics presented in this article, analysts detect growth tendencies for the syndicated lending market primarily due to Russian commercial banks, which by acting jointly may partially satisfy loan-based funding needs of large business. Therefore, in the nearest future credit institutions will start offering new and objectively more advanced lending instruments to their clients. Besides, a part of Russian banks legal entity clients may be involved as direct lenders in projects that prioritize domestic funding.

Law provisions now do not come across as regulations that will cover a significant part of entities. Nevertheless, the national legal system received a modern instrument that may make it possible to transfer a part of large financial projects to the Russian jurisdiction. This fact gives Russian-speaking lenders and borrowers a chance to make such guarantee-based deals, and with no involvement of foreign lawyers, consultants and attorneys required for their structuring, execution and dispute settlement.

In any case, we hope that the Russian legislator will also give a chance to use similar regulations for funding with no participation of credit institutions.

- Article 3 of Federal Law No. 486-ФЗ dated 31.12.2017 ” On Syndicated Credit (Loan) and Changes to Particular Legal Acts of the Russian Federation”.

- Article 4 of Federal Law No. 486-ФЗ dated 31.12.2017 ” On Syndicated Credit (Loan) and Changes to Particular Legal Acts of the Russian Federation”.

- Article 356 of the Civil Code of the Russian Federation.

- Clause 3, article 4 of Federal Law No. 486-ФЗ dated 31.12.2017 ” On Syndicated Credit (Loan) and Changes to Particular Legal Acts of the Russian Federation”.

- Article 2 of Federal Law No. 486-ФЗ dated 31.12.2017 ” On Syndicated Credit (Loan) and Changes to Particular Legal Acts of the Russian Federation”.

- For example, the term syndicated loan was widely used in Regulation of the Bank of Russia No. 139-И dated 03.12.2012 “On Bank Statutory Requirements”.

- https://www.dentons.com/ru/insights/alerts/2018/march/7/syndicated-loans-march-ahead.

- http://loans.cbonds.info/rankings/volume/243#cis.

- https://www.rbc.ru/finances/18/04/2016/57109e219a79474c7fba44af.

- For example, PJSC Credit Bank of Moscow has been using this instrument of financing since 2003: https://mkb.ru/investor/debt/syndicated-loans.

Olga Kuramshina

Ex-Leading Lawyer

Tax and Legal Practice

Korpus Prava (Russia)

Other Articles on Topics