The world was told so many times about globalization, strengthening of international ties and blurring of boundaries between states in economic, social, cultural terms. Therefore let’s omit the due introduction about the relevance of knowledge about the European value-added tax. It’s enough to imagine that you (Russian company) own goods located in a warehouse in Bulgaria, and plan to sell them to a Belgian company, for example. Bulgaria is close, and should the VAT be levied on transaction or not? We’ll try to provide the answers to this and other inevitable questions below.

In 2007 the EU Council Directive 2006/112/EC on the common system of value added tax came into force. Approving the common system of VAT, the Directive left to the discretion of each EU member state the establishment of the national tax rate and the recognition criteria of a business as being VAT payer. Therefore, despite the unified European imposition of VAT, it is impossible to determine the amount of tax for each specific operation without recourse to the national legislation.

In the European Union four business transactions are subject to VAT:

- Supply of goods in a single EU member state;

- Acquisition of goods in the EU;

- Provision of services;

- Import of goods.

In this article we will address the features of imposition of VAT on the first two transactions.

Supply of Goods

Supply of goods for VAT purposes is the actual transfer of the right to dispose of tangible assets1, which does not necessarily coincide with the legal transfer of ownership. As shown by a number of judgments, for the supply of goods performed for a party to the transaction to be recognized, it is sufficient to authorize the other party to dispose of the goods as their own2. It should also be noted that the criterion of materiality in the context of the European legislation on VAT is key for the demarcation of the supply of goods and provision of services as two distinct taxable transactions. That is why the transfer of intangible assets such as copyrights, patents, franchises is classified as provision of services3.

The EU member states may for the VAT purposes consider as goods the following items:

- Share in the ownership to real estate;

- Proprietary right to use real estate.

Also, the issue of recognition as supply of goods for VAT purposes the use by taxpayer for their own needs of the goods produced, acquired or imported, if the VAT on such goods purchased from another taxpayer, would not fully be deductible, is to be addressed at the discretion of the national legislator.

Upon supply of goods without use of transport the place of supply is the place where the goods were transferred4.

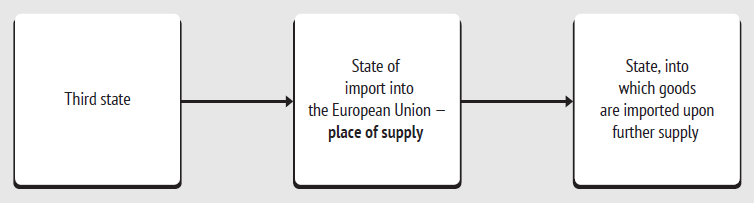

Upon supply of goods with transport the place of supply is considered the place where the transportation of goods started. If the transportation of goods begins in a state which is not member of the EU (hereinafter – the third state), the place of supply made by the importer, will be the state of import. The place of further supplies will also be the state of import5.

Acquisition of goods within the EU (hereinafter – IC acquisition)

The transaction of acquisition of goods within the EU means acquisition of the right to dispose of tangible asset, delivered to the seller in another EU member state, rather than in which the transportation began6. The use by the taxpayer for their own needs of the goods brought from another member state of the European Union, where they were produced, acquired or imported, for tax purposes equal to the IC supply, i.e. supply of goods within the EU.

The IC acquisition corresponds to the IC supply, which is taxed at a rate of 0%7 and entitles to deduction for goods and services that were acquired for the purposes of the IC supply8.

As a general rule, to apply the 0% rate to the IC supply the supplier shall provide to the tax authorities of its state the following information:

- Proof that the goods were shipped or will be shipped to another EU member state;

- Registration number of the buyer as VAT payer in the state of arrival of the goods.

In fact, the IC supply and IC acquisition are one and the same trade transaction. The exemption from VAT of the IC supply allows avoiding double taxation, on the one hand, in the state where the transportation began and, on the other hand, in the state where the transportation ended.

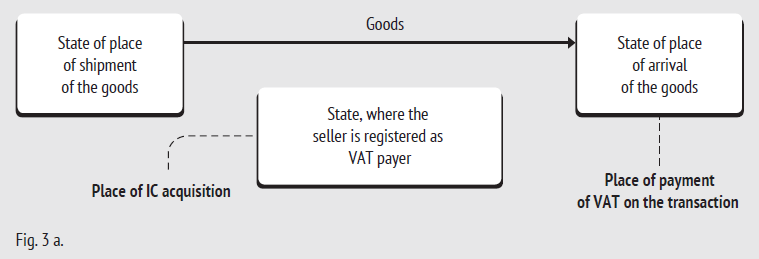

The place of the IC acquisition as a taxable transaction is the place where the transportation of goods ends9. By default, the end point of transportation is recognized the state, in which the buyer is registered as VAT payer. For example, the place of the IC acquisition is Sweden, if the invoice issued to the buyer specifies the VAT payer registration number assigned by Sweden, despite the fact that the supply was carried out, for example, from Germany to any other state (not Sweden). In any case, the VAT on the IC acquisition shall be paid in the state where the goods arrive10 (fig. 3a). If the buyer in the VAT return states that the tax on the IC acquisition was levied in the country where virtually the transportation ended, the tax base shall be reduced in the state where the buyer is registered as VAT payer.

The taxable event in respect of the IC acquisition occurs at the time when such acquisition is considered to be performed in the relevant EU member state. The VAT on the IC acquisition shall be levied from the 15th day of the month following the month in which such transaction was made. However, if the invoice for the transaction was already been issued prior to the 15th day of the month following the month in which the transaction was made, the VAT is chargeable on the date of invoice.

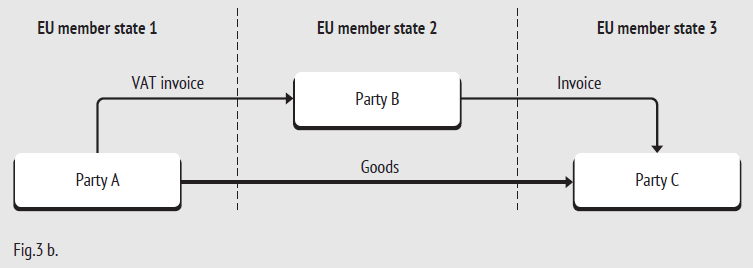

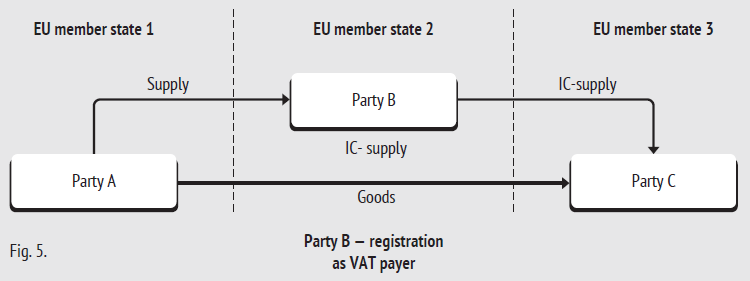

Tripartite transaction related to supply of goods

The EU Council Directive 2006/112 /EC provides for the mandatory compliance by all the EU member states with the rule on application of the 0% rate to the tripartite transactions of IC acquisition, which correspond to a number of conditions:

- All three transactions (Party A, Party B, Party C) are registered as VAT payers in different EU member states (the scenario under which the mediator – Party B – is registered either in the state of shipment or in the state of delivery of goods, so two parties to the transactions are registered in one EU member state);

- Party A sells goods to Party B, which in turn sells the goods to the Party C, but the goods are delivered directly from Party A to Party C11 (fig. 3).

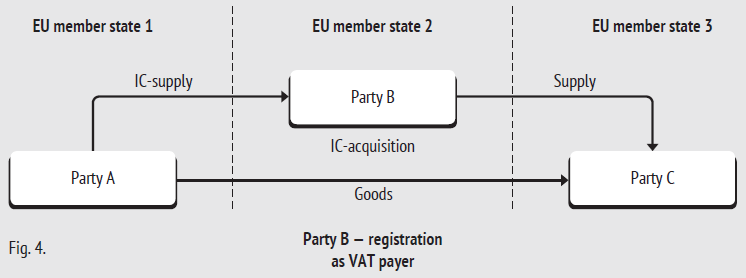

The scheme works as follows:

- Party B provides to Party A its VAT payer registration number in the EU member state 2 and the proof that the goods left or have to leave the territory of the EU member state 1, based on which Party A issues to Party B an invoice with zero VAT as part of the IC supply.

- The goods are sent directly from the EU member state 1 to the EU member state 3. As a general rule, Party B performs in this case the IC acquisition, the place of which is the EU member state 3 ( 2). If in accordance with the national legislation of the EU member state 3, the amount of the IC acquisition is such that the Party B shall be registered as VAT payer in that state, then upon such registration the Party B, supplying the goods to the Party C, performs the usual supply in a single state of the European Union. The simplified taxation of tripartite transactions exempts the Party B from the obligation to pay VAT on the IC acquisition in the EU member state 3: in this case VAT is charged and paid by the final buyer, the Party C.

- The Party B shall send to the Party C an invoice with reference to the application of the rule on taxation of tripartite transactions, on the basis of which it does not include VAT in the cost of supply, and the tax liability rests with the end customer.12

Not all states of the European community equally apply the provisions of the Directive 2006/112 / EC on taxation of tripartite transactions. Some of them allow using the above scheme to transactions that involve more than three members, while others do not.

In some states, the application of this scheme is not possible if the mediator – the Party B – is registered as VAT payer not only in the state of its location, but also in the state of supply of goods13. In this case, the transaction between the Party A and the Party B is IC supply with zero VAT, which corresponds to the IC acquisition. The transaction between the Party B and the Party C will be a common supply of goods within a single state. Weather in this case the obligation to pay tax relies on the Party C or not, depends on the features of the national legislation.

On the contrary, in a number of states the rules of taxation of tripartite transactions may be applied, if the Party B is registered as VAT payer not only in the state of its location, but also in the state of shipment of the goods. In this case, the transaction between the Party A and the Party B will be supply within one state, and the transaction between the Party B and the Party C – the IC supply, which corresponds to the IC acquisition.

When working with tripartite (or multipartite) transactions related to supply of goods, the parties must remember that if the goods cross the state once, the right to apply the 0% rate to the IC supply also occurs once,14 even if the goods were subject to several supply agreements between persons registered as VAT payers in different states of the European Union. Therefore, in practice, the question arises as to what kind of transaction in the supply chain the rate of 0% shall be applied. The European Union legislation does not contain specific guidance on this matter; the norm was developed by the European court in the course of law enforcement15. The transfer by the Party A of the right to dispose of the goods to the Party B in the EU member state 1 will be recognized as IC supply, provided the Party B conveys to the Party A the following information:

- Proof that the goods were shipped or will be shipped to another EU member state;

- Registration number of the buyer as VAT payer in the state of arrival of the goods.

However, if the Party A knows or should have known that the right to dispose of the goods will be transferred by the Party B to the Party C prior to transportation, the Party A shall issue an invoice with VAT of the state where the goods were shipped. In this event, the transaction between the Party B and the Party C will be taxed at the rate of 0% like the IC supply.

It worth mentioning that the court practice of the recent years allows certain derogations from the norms of the EU Council Directive 2006/112/EC on the registration of participants in tripartite transactions as VAT payers in the EU member states16. So if the Party B to the tripartite transaction is a person that carries out its main activity in a third country and is not registered as VAT payer in the European Union, the application of 0% rate to the IC-supply from the Party A to the Party B can not be denied merely on these formal grounds. The European court pointed out three essential conditions to be met to be entitled to apply the 0% rate:

- The right to dispose of the goods is transferred to the Party B;

- The goods are shipped from the EU member state to another EU member state;

- The Party B shall fall within the definition of VAT payer, that is to carry out such commercial activity.

At the end of the review of transactions related to the supply of goods it should be noted that the European Union established a system for the exchange of tax information (hereinafter – VIES), the purpose of which is preventing abuse of exemption from VAT of IC supplies and tripartite transactions. Under VIES each VAT payer shall quarterly or monthly provide to the tax authorities of its state a report containing the following information on:

- Contractors of the IC-supplies;

- Persons registered as VAT payers, to whom goods were supplied, acquired by taxpayers within the IC-acquisition;

- Persons registered as VAT payers, to whom services are rendered.

Right to deduct the paid VAT

The VAT payer may deduct the amounts of tax that are paid by it upon acquisition of goods and services used in its commercial activity, in the following cases:

- Acquisition of goods within the borders of one state;

- Payment for services;

- Acquisition of goods in another EU member state (IC-acquisition);

- Import of goods into the EU state.

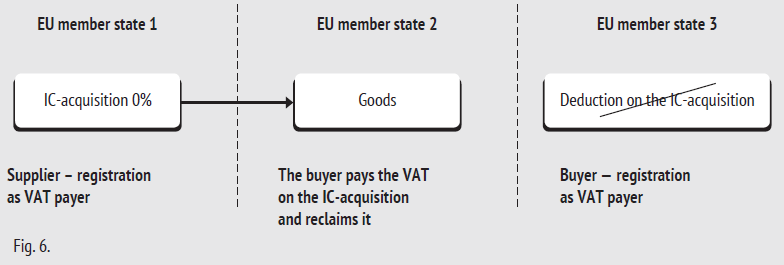

It should be remembered that the IC-acquisition, upon which the goods are supplied to another state other than that in which the buyer is registered as VAT payer, does not entitle to deduction in the state of registration, but entitles to reclaim the amounts of tax paid in the country of arrival of goods17 (fig. 6). To be eligible for a the right to deduction in the country of arrival of goods the buyer had to be registered as VAT payer in that state, or to organize the transaction in such so as the IC-acquisition to meet the condition for VAT exemption under the tripartite transaction.

The EU Council Directive 2008/9/EC of 12.02.2008 establishes the procedure for refund of tax amounts paid in the EU country in which the goods or services were delivered to the taxpayer from another EU member state, or in which it imported goods, but in which it does not carry out commercial activity. To be granted the right to refund in another EU member state the taxpayer shall meet the following criteria:

- Not have in this state official address;

- Not have in this state a permanent establishment;

- During the relevant period18 not to supply goods or provide services in that state19.

For the tax amount to be refunded in such state the taxpayer shall, no later than 30 September of the year following the relevant period, submit an electric application through the Internet resource designated for that purpose by the EU state where the taxpayer does business20. The state in which the refund is requested, shall no later than 4 months from the date of receipt of such application, notify of its consent or refusal to refund the paid VAT21.

Let’s return to the issue specified at the beginning of the article. VAT assessment by the Russian company that sells the goods from the warehouse located in Bulgaria to a Belgian company depends on where the goods are transported after sale. If the goods are delivered in Belgium or another EU member state outside Bulgaria, such transaction is subject to VAT at the rate of 0%. The Russian company becomes obliged to register as VAT payer in Bulgaria, if the transaction amount exceeds €25,56522, and file in due time to the tax authority of Bulgaria the VIES report on supply. If the right to dispose of the goods passes from the seller to the buyer in the warehouse, and transportation is not expected, the Russian company is obliged to issue an invoice to the buyer indicating the Bulgarian VAT.

- Article 14 of the EU Council Directive 2006/112/EU.

- Decision of the European Court of Justice 06/02/2003 C-185/01 in the case Auto Lease Holland. Decision of the European Court of Justice pf 14/07/2005 C-435/03 in the case British American Tobacco International Ltd.

- Decision of the European Court of Justice 21/10/1999 C-97/98 in the case Peter Jagerskiold v Torolf Gustafsson.

- Article 31 of the EU Council Directive 2006/112/EU.

- Article 32 of the EU Council Directive 2006/112/EU.

- Article 20 of the EU Council Directive 2006/112/EU.

- Article 138 of the EU Council Directive 2006/112/EU.

- Article 169 (b) of the EU Council Directive 2006/112/EU.

- Article 40 of the EU Council Directive 2006/112/EU.

- Article 194 of the EU Council Directive 2006/112/EU.

- Article 141 of the EU Council Directive 2006/112/EU.

- Chris Platteeuw, Quick Reference to European VAT Compliance, Kluwer Law International BV, The Netherlands 2010, p. 5-7.

- http://www.tei.org/news/Documents/TEI_comments_green_paper_future_of_VAT_.pdf

- Opinion of the Attorney General, Ms. Cocotte of 11/11/2005 in the caseС-245/04 EMAG, ECR [2006].

- Decision of the European Court of Justice 30/01/2010 in the case C-430/09 Euro Tyre Holding BV.

- Decision of the European Court of Justice 27/09/2010 in the case C-587/10 Vogtländische Straβen-Tief und Rohrleitungsbau GmbH Rodewisch.

- Decision of the European Court of Justice 22/04/2010 in the case C-536/08 и C-539/08, X and fiscal unity Facet-Facet Trading.

- The period for which the VAT may be stated for recovery is established by national legislation, but pursuant to article 16 of the EU Council Directive 2008/9/EU of 12.02.2008 can not be less than 3 months and more than 1 year.

- Article 3 of the EU Council Directive 2008/9/EU of 12.02.2008.

- Article 7, article 15 of the EU Council Directive 2008/9/EU of 12.02.2008.

- Article 19 of the EU Council Directive 2008/9/EU of 12.02.2008.

- Pursuant to article 96 of the Law of Bulgaria on VAT an must register as VAT payer if the sales turnover for the period of 12 consecutive months is over €25,565 or 50,000 levas.

Yana Karausheva

Ex-Junior Lawyer

Tax and Legal Practice

Korpus Prava (Russia)

Other Articles on Topics