Literally, the subordinated debt means a debt subordinated to other credits, which is ranked lower than other credits in case of debtor’s liquidation or bankruptcy.

Such form of crediting is used worldwide by those, who are closely tied with the borrowing entity, but for one reason or another prefer to loan the funds rather than investing them in the borrower’s authorized capital (by purchasing the borrower’s shares). The subordination of the subordinated loan to other (regular) credits stipulates their higher riskiness, and therefore higher rates of return. Higher rate of return, in its turn, allows for such credits to be used for speculation purposes on the stock market.

The subordinated loan in Russia means a way of long-term monetary investment made in form of credit (deposit, loan, bonded debt), which the lending institution attracts to replenish its supplementary capital.

Previously, the definition of subordinated loan was stipulated in the by-laws, in particular in the Provision on the Methods of Measurement of Equity Capital of Lending Institutions (approved by Regulation No. 215-П of the Bank of Russia as of February 10, 2003).

However, the detailed definition of the subordinated loan (credit, deposit, bonded debt), as well as the legal regulation of such instruments has been formalized in Russian legislation not so long ago, namely concurrently with the approval of the Federal Law No. 432-FZ as of December 12, 2014 “On amendments to certain legislative acts of the Russian Federation and on declaration of some legislative acts (provisions of the legislative acts) of the Russian Federation as null and void”, which has introduced relevant amendments to the Law on Banks and Banking Activity, as well as to the Law on Insolvency (Bankruptcy).

At present the subordinated loans are legally regulated by the Law on Banks and Banking Activity, the Law on Insolvency, Provision on the Methods of Measurement of Equity Capital of Lending Institutions (Basel III). The subordinated loan (deposit, credit) agreements or terms of bonded debts are subject to the Rules of Civil Code of the Russian Federation on loan, credit, bank deposit or gift with due account of the aforementioned peculiarities.

As set forth in the applicable Russian legislation1 the subordinated loan (deposit, credit, bonded debt) means a loan (deposit, credit, bonded debt), which at the same time meets the following criteria:

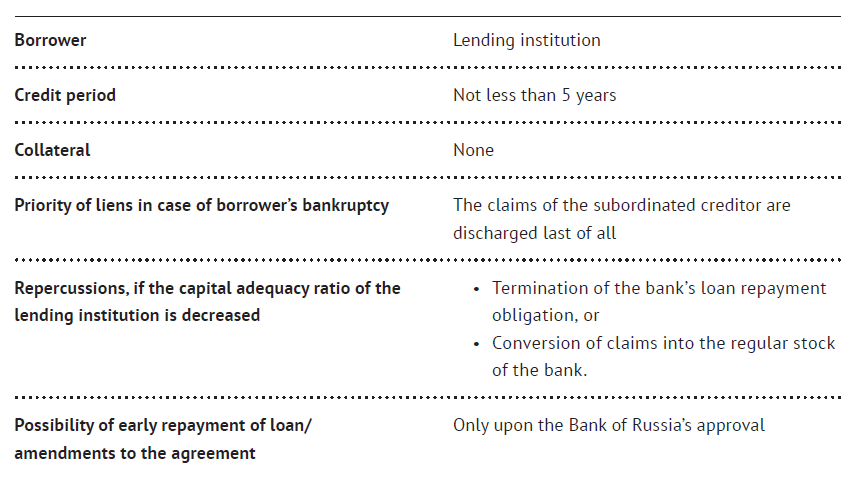

- A lending institution only can act as a borrower.

- The period of credit (deposit, loan) and the maturity of obligations should be not less than five years or there is no maturity date.

- The terms of credit (deposit, loan) or bonds issue stipulate that the following actions can be done only with the consent of the Bank of Russia:

- Full or partial early repayment of credit (deposit, loan) or part thereof, as well as early payment of interest thereon or redemption of bonds;

- Termination of credit (deposit, loan) agreement and (or) making amendments to the existing agreement.

- The terms of granting a loan (terms of bond issue) should not significantly differ from the market terms of granting of similar loans.

- The terms of granting a loan (terms of bond issue) should contain a provision that if a lending institution is insolvent the claims under such loan shall be discharged upon settlement of claims of all other creditors.

The distinctive feature of the subordinated loan agreement is the absence of any collateral from the borrower.

This being the case, the subordinated loan agreement may contain a provision on the right of a lending institution to refuse from payment of any interest under the subordinated loan (deposit, credit, bonded debt) agreement unilaterally without any subsequent penalties.

The main thing, which distinguishes the subordinated loan from other loans, is the ability to perform one of the following actions, if certain conditions occur:

- Termination of lending institution’s obligation to repay the amount of principal debt and to pay the interest and penalties accrued;

- To exchange or convert creditors’ claims under subordinated loans into ordinary stock (shares in the authorized capital) of the lending institution.

The aforementioned actions are permissible, if the capital adequacy ratios of the lending institution become lower than the level specified in the relevant normative act of the Bank of Russia. Such actions are applicable upon the Bank of Russia’s approval of the Plan of Engagement of the Bank of Russia in the measures to prevent the bank’s insolvency or approval by the Bank Supervision Committee of the Bank of Russia of the Plan of Engagement of the State Corporation Deposit Insurance Agency, which stipulate financial assistance from the Bank of Russia and Financial Aid Agency.

At the same time, termination of the bank’s obligation under the subordinated loan agreements or exchange (conversion) of the creditors’ claims under the subordinated loans is one of the terms of provision of financial assistance by the Bank of Russia to the lending institution in case of critical situation in the bank.

The distinctive feature of legislative regulation of the subordinated loans is that the claims thereunder, if the lending institution is declared insolvent, are discharged only upon discharge of claims of all other creditors2.

Find in the table below the main differences between subordinated and regular loans:

A particular attention should be drawn to the fact that the legislative provisions (including those stipulating an option of unilateral termination of obligations on the subordinated loans by the lending institutions, as well as those setting the priority of creditors in case of insolvency of such organizations) became effective on December 23, 2014. Nevertheless, paragraph 8 of Article 15 of the Federal Law No. 432-FZ as of December 22, 2014 reads that these provisions have a retroactive force and extend to the relations started before the law has come into force.

This means that the legal position of the creditors of financial institutions (holders of bonds, deposits, lenders) under the subordinated products issued before the date of the law, has significantly deteriorated and endangered.

This being the case, when the legislative framework regulating the flow of subordinated financial instruments came into being, the banks had already been terminating their obligations arising out of such agreements unilaterally (Trust, Uralsib, Peresvet, Yugra, upcoming amortization of debts under the subordinated obligations in Binbank and Otrkitie).

Meanwhile, Russian legal practice has not yet seen any positive outcomes of claims filed against the banks terminating their obligations under the subordinated products either from the individual lenders (Determination of the Supreme Court of the Russian Federation as of May 23, 2017 on the case No. 24-КГ17-3, Ruling of Nikulinskiy District Court as of July 4, 2017 on the case No. 2-4121/17, etc.) or from the institutional lenders (Ruling of Arbitral Court of North-Western Okrug as of July 29, 2016 on the case No. А56-36949/2015, Ruling of Arbitral Court of North-Western Okrug as of July 29, 2016 on the case No. А56-25411/2015).

It is obvious that the subordinated lending is rather a risky business for the junior creditor for several reasons:

- In case of bankruptcy of a lending institution, the subordinated creditors’ claims are discharged last of all, upon discharge of the claims of other creditors;

- The bank may unilaterally terminate its indebtedness to the subordinated creditors.

Nevertheless, the subordinated financial products have been rather of a high demand until recently. In most cases this is explained by the high interest rates the subordinated creditors get in return for the funds.

Summarizing the above, it is worth to mention that the analysis of ongoing changes in the normative and legal framework indicates a clear intention of a legislator to improve the regulation of subordinated instruments in Russia. Measures taken are timely as never before in the light of existing economic situation, which forces the financial market participants to attract additional sources of financing.

It goes without saying that the subordinated lending is a good tool for the participants of the banking sector, as it allows the banks:

- To attract additional long-term financing;

- To increase additional capital of the bank without dilution of shares of its owners;

- To plan the long-term business projects of the bank efficiently.

But it is evident that the existing legal support of the creditors is insufficient, which will be an obstacle for distribution of subordinated financial products on the banking services market.

- Article 25.1 of the Federal Law No. 395-1 as of December 2, 1990 (as amended as of June 18, 2017) “On Banks and Banking Activity”.

- Article 189.95 of the Federal Law No. 127-FZ as of October 26, 2002 “On Insolvency (Bankruptcy)”.

Alexey Oskin

Deputy Director

Tax and Legal Practice

Korpus Prava (Russia)

Other Articles on Topics