For some time now legislators have tried to attract personal savings to the securities market. It may be explained by the fact that Russian companies desperately need financial injections, but many of them have no access to the market of cheap foreign credits.

The Russian investment market requires the so-called “long-term money”, therefore, tax allowances for investors are granted only in case of a long-term holding of securities.

Thus, one of the innovations introducing tax exemption of income from securities transactions is an implementation of a minimum holding period of securities.

This allowance is applied subject to the following conditions:

- Shares and bonds should be listed on the stock exchange;

- Securities should be bought after January 1, 2014;

- Holding period of securities should be not less than three years;

- Securities should be sold at a profit;

- Securities should not be accounted on the taxpayer’s investment account.

Provided all these conditions are fulfilled, a taxpayer shall be granted a personal income tax allowance which equals profit from securities sales.

But nothing is perfect, as the legislation sets out amount limitations. A profit subject to tax exemption may not exceed 3 million roubles multiplied by the number of full years of securities holding.

Example. Shares were bought in February 2014 and sold in April 2017.

The amount of 9 million roubles can be subject to tax exemption.

If the profit exceeds this sum, the remaining sum is due to taxation. For each year of securities holding the amount exempted from taxation grows by 3 million roubles.

Considering the terms for the application of this allowance, it may be granted for the first time in the upcoming 2018, if securities were bought in 2014 with a profit gain in 2017.

One more innovation is individual investment accounts aimed at increasing attractiveness of investments in stock market instruments for private investors by granting tax deductions.

Individual investment account is an internal balance account aimed at a separate accounting of individual client’s money, securities, obligations under contracts entered into on behalf of the said client. It is opened and managed in accordance with Article 10.3 of the Federal Law On the Securities Market. Any professional participant on the securities market is entitled to manage such contract. Each client may open only one such account.

Opening of such accounts for individuals is stimulated by the right to an investment tax deduction for the amount they has paid in (not exceeding 400 thousand roubles), or the amount they will get after closing the account.

Two types of tax deductions are stipulated for an individual investment account. Whereas a taxpayer may choose only one type of tax deduction. Combination of both types is impossible throughout the whole validity period of a contract for managing an individual investment account.

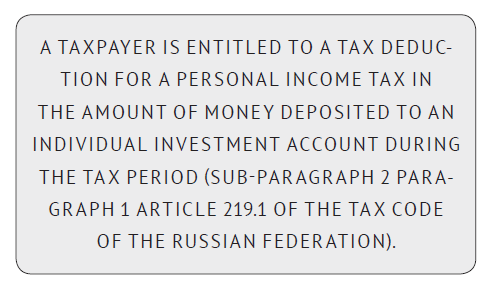

The first type of an investment tax deduction:

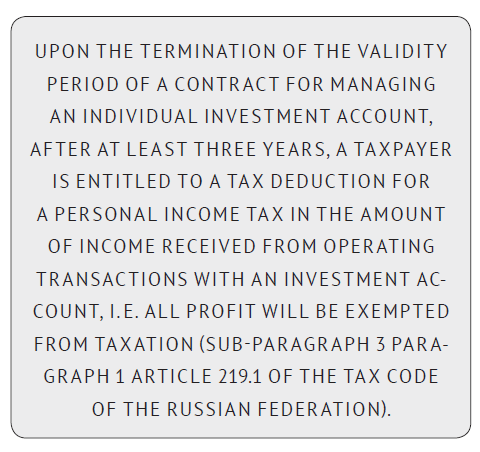

The second type of an investment tax deduction:

It’s important to remember that upon closing of an individual investment account earlier than three years all income tax deductions received must be repaid.

There are several limitations related to individual investment accounts for individuals:

- An individual is entitled to have only one contract for managing an individual investment account; in case a new contract is executed, the previous contract shall be terminated within a month;

- Under a contract for managing an individual investment account a client is allowed to transfer only money to a professional participant on the securities market;

- An aggregate amount of money that may be transferred under such contract during a calendar year shall not exceed 400,000 roubles.

An individual is entitled:

- To claim money and securities accounted on his/her individual investment account or their transfer to another professional participant on the securities market who is a party to a contract for managing an individual investment account;

- To terminate a contract for managing an individual investment account (brokerage agreement or securities trust agreement) of one type and enter into a contract for managing an individual investment account of a different type with the same or a different professional participant on the securities market.

In turn, a professional participant on the securities market shall enter into a contract for managing an individual investment account only in case an individual states in writing that he/she has no other contract for managing an individual investment account with another professional participant on the securities market or that such contract will be terminated not later than in one month.

Upon termination of a contract for managing an individual investment account a professional participant on the securities market shall submit information on an individual and his/her individual investment account to a professional participant on the securities market with whom a new contract is executed.

Calculation, charging and payment of a personal income tax for transactions with securities accounted on an individual investment account are carried out by an agent as of the termination date of a contract for managing an individual investment account, unless a contract is terminated with a transfer of all assets accounted on an individual investment account to a different individual investment account in the name of the same individual. If a contract is terminated with a transfer of all assets accounted on an individual investment account to a different individual investment account in the name of the same individual, for the purposes of tax base calculation an opening date of a terminated (initial) contract shall be deemed an account opening date.

A tax agent qualified as an income source for transactions accounted on an individual investment account shall notify a tax authority at its location on the opening or closing of this account within three days from the date of the relevant event.

One more easement of a tax burden for individuals is personal income tax exemption of coupon payments for corporate marketable bonds denominated in roubles and issued from January 1, 2017 to December 31, 2020.

It should be mentioned that previously interests on government treasury bills, bonds and other government securities of the former USSR, member states of the Common state and constituent entities of the Russian Federation, as well as bonds and securities issued pursuant to the resolution of local representative bodies, were exempted from taxation.

Now the legislation equaled taxation of payments for government and corporate loans, but one should remember that a major peculiarity of this allowance is the fact that the bond issue date is the date of their state registration.

Therefore, when determining whether this or that bond is covered by this law, one should consider the date of its state registration. The registration date and the placement date may differ by several months. For example, registration may have taken place at the end of 2016, but the placement may have begun at the beginning of 2017. Such bond is not covered by the law.

Furthermore, it should be mentioned that personal income tax redemption is provided for the income received from discount only upon redemption.

As for the coupon income, tax exemption is provided for a coupon that does not exceed a discount rate increased by 5%.

Now a discount rate equals a key interest and amounts to 8.5%, i.e. a coupon for more than 13.25% will be taxable at the rate of 35%. Coupon income interest is calculated par value.

It should be noted that the law comes into force 30 days after its official publication, but not earlier than on the first day of a new tax period for a personal income tax.

Therefore, coupons discharged in 2017 are taxable at the rate of 13%, but all the payments receivable by investors under the bonds of 2017 starting from January 1, 2018 to the redemption of the bond, are exempted from taxation. The bond may be redeemed after December 31, 2020, and all its coupons will be fully deposited on an investor’s account without 13% deduction.

Thus, bond income will be taxable pursuant to the regulations regarding interest income from bank deposits, and this situation definitely makes sense.

Other Articles on Topics