Over the past decade, we can observe a global trend to combat tax evasion. If previous BEPS (Base erosion and profit shifting) plan, which was issued by the Organization for Economic Cooperation and Development (OECD) did not seem convincing, and many items seemed to be unachievable, now we see how lots of jurisdictions, including unexpected ones, read this plan with great enthusiasm and try to implement it in its reality.

The tax control bodies acquire more and more tools to identify and control creative taxpayers. For example, one of the most effective tools is the international automatic exchange of tax information, while the elegance of this tool lies in vesting the financial organizations (in particular, banks) with responsibility for the initial collection of information. Such organizations as a rule are well-informed of their clients, their activities, sources of funds, income, account managers, business managers and persons appointed as nominee managers, in some cases as customer managers, as well as of personal data, carefully collected over the years of working with the client in order to improve the quality of service.

Now working with a bank, the company is obliged to provide as much information as possible about its activities, not only officially filling out the client’s application form, but also confirming everything with documents. Previously, the company by default was considered a tax resident of the jurisdiction of its registration, the most thoughtful persons requested a tax residency certificate. Five years ago, the bank neither requested information on the place of business, the place of residence of the director, confirmation of the director’s qualifications (and if the director did not look qualified enough, then on the person who made the key decisions), nor pay attention to the account manager’s email address (it does not matter that it has domain extension .ru), phone number and certainly failed to consider this in a complex in order to analyze the entire management structure and determine the tax residence of the company.

Among other things, banks have black lists of jurisdictions with which they do not work because they are considered as high-risky, so if a client comes in, with a company registered in the Marshall Islands, the bank reviews its instruction, risk list and understands that the Marshals are blacklisted, then the bank refuses to open the account.

The inclusion by a bank of one or another jurisdiction in its black list may be due to various reasons, both political and economic, for example, state bodies of jurisdiction of a company incorporation do not provide an adequate level of control over their taxpayers (there is no reporting requirement, changes in the shareholders’ composition are listed only in the registry maintained by the company secretary).

In the light of the above, the so-called real substance or economic substance has recently become one of the most relevant trends. You can translate it into Russian as a real presence, economic entity, in the tax code of the Russian Federation, for example, this phenomenon is reflected as an actual recipient of income. If we simplify the explanations as much as possible, then the criterion “economic substance” is the presence or absence of real economic activity (it is the same as the economic presence) of the company in the territory of a particular jurisdiction.

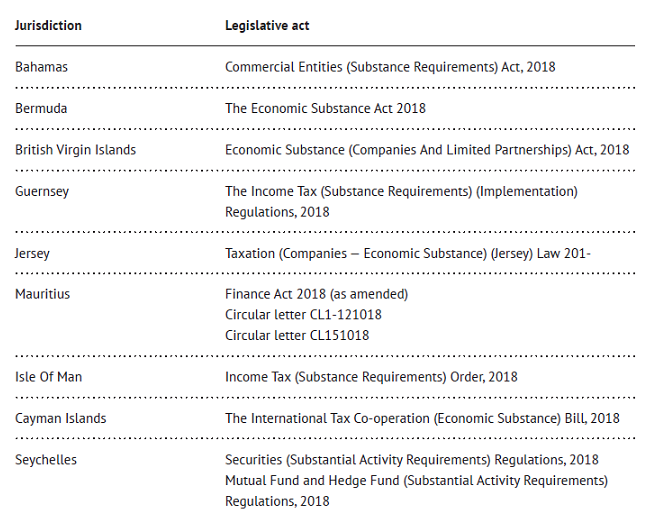

The requirement for economic presence reached the places, where no one expected it would even get a glimpse, namely, offshores, in particular Belize, the Seychelles, Mauritius, the Cayman Islands, Bermuda, Jersey, Guernsey and the Isle of Man adopted Economic Substance Law. Below is a table with legislative acts.

Economic Substance Law introduces requirements for economic presence for all companies and limited partnerships that are registered in and are tax residents of these jurisdictions.

So this year, companies and partnerships have to decide on their tax residency status. To become a tax resident of the offshore jurisdiction of the company, it is necessary to confirm the economic activity in the offshore territory and comply with the requirements established by law.

However, not all companies and partnerships are required to confirm the tax residency status of an offshore.

Companies that are subject to the law and which have to ensure an economic presence shall be deemed as the companies that carry out “relevant activities”, and defined as follows:

- Financial companies (banking business, insurance business, stock exchanges);

- Shipping business (shipping companies);

- Holding business;

- Intellectual property business;

- Distribution and service business.

The companies that claim themselves as tax residents of another jurisdiction, or companies that carry out activities other than those referred to as “relevant” are recognized as entities not covered by the law.

Requirements for the economic presence of companies are relatively abstract, it is assumed that the practice will show the exact criteria in numerical values. The following requirements are used:

- Staff in number appropriate to the scale of the company’s business, in this case the employees must have the education and experience necessary to perform their job duties corresponding to the declared main activities of the company;

- Availability of the office required for the placement of staff and for conducting the business of the company (we can assume this refers not only to rent of premises, but also to workplaces equipped with office equipment, telephone, internet connection);

- Accounting and preparation of financial statements on a regular basis (there is an obvious need to appoint a responsible person who performs this function and has the appropriate qualifications);

- Expenses incurred by the company must be adequate to the activities carried out by the company both in terms of volume and substance. Presumably, it means that the costs should be aimed at profit-making and correspond to the declared main type of the company’s activity.

Consistently ask who will administer the collection of information on the economic presence of the company.

Let’s look at the example of the BVI, the law requires that each corporate service provider (registered agent), that registers a company subject to the Law, has information on the place of tax residency of the company, and should be ready to transfer this information to the competent authorities of the relevant jurisdiction. For example, information (on the staff on BVI and abroad, financial statements, office address, etc.) on companies claiming to be BVI residents will be stored in the electronic system Beneficial Ownership Secure Search system (BOSS).

Registered companies and partnerships are required to have commitments regarding economic presence by June 30, 2019. If a company performs one of the “relevant activities”, then such a company must inform its registered agent and provide it with information on compliance with the requirements for its economic presence. Information must be submitted before June 30, 2020, and subsequently it will need to be updated annually. Today, specific requirements regarding this information have not been approved yet, so we don’t know the extent of detailed information on the fulfillment of requirements for economic presence that the companies have to describe.

The registered agent will upload the data obtained to the BOSSs information system. Tax authority of the BVI (International Tax Authority, ITA) will have the access to this information, which will monitor the completeness and relevance of the data and send additional requests to companies. Information may be also submitted to the competent authorities of a foreign jurisdiction, for example, if a company registered in the BVI stated that it is a tax resident of such foreign jurisdiction.

New companies in the BVI can be registered only if all the requirements for economic presence are met.

Legal entities that do not comply with the new requirements will be forcibly deleted from the Register of Companies or the Register of Limited Partnerships. For violations of the law, a fine will be imposed, the minimum amount of which is 5,000 US dollars. In the event of non-payment of this fine, a cascade system of increasing the amount of fines will become effective. Some violations may result in criminal liability in the form of imprisonment for up to five years. ITA requirements and fines can be appealed in court.

It is reasonable to suggest that with due time, as the new law is applied, the text of the regulatory acts on real presence will be refined, more detailed requirements, explanations and guidelines will appear that reduce the ability of businesses to hide behind formally minimum observable requirements. However, there remains an open question about the capabilities and resources of local infrastructure, statistics from various available sources suggests that companies that need to bring their activities in line with the new requirements set by the law far exceed the capabilities of the jurisdictions in which they are registered (this includes employees, office premises, and so on).

Taking into account the above, the business needs to review the capital structure and assess the need and cost of company maintenance in offshore jurisdictions, because in most cases the maintenance costs of a company bearing signs of a real economic presence, will even the benefits derived from tax savings. Perhaps you should pay attention to other jurisdictions where, on the one hand, the infrastructure allows for an economic presence at a lower cost, and on the other hand the tax burden is still low.

Other Articles on Topics