When making a decision to purchase property (fixed assets) under the financial lease (leasing) agreement, a business owner rarely thinks about peculiarities of accounting and tax consequences that this method of acquisition will entail.

In the financial lease agreement, it is necessary to indicate on whose balance sheet a leased asset is accounted, as this affects accounting and tax accounting of the purchased car.

Rules of accounting of leased assets are determined by Order No. 15 of the Ministry of Finance of the Russian Federation dated 17.02.1997, and rules of tax accounting are determined by Articles 256-258 of the Tax Code of the Russian Federation.

Order No. 15 was last amended in 2001, that is why it contains many outdated issues (for example, numbers and titles of accounts). Nevertheless, there is no other “instruction” on leasing accounting published.

The procedure of accounting and tax accounting for the acquisition of non-current assets under financial lease (leasing) agreements should be set in the accounting policy.

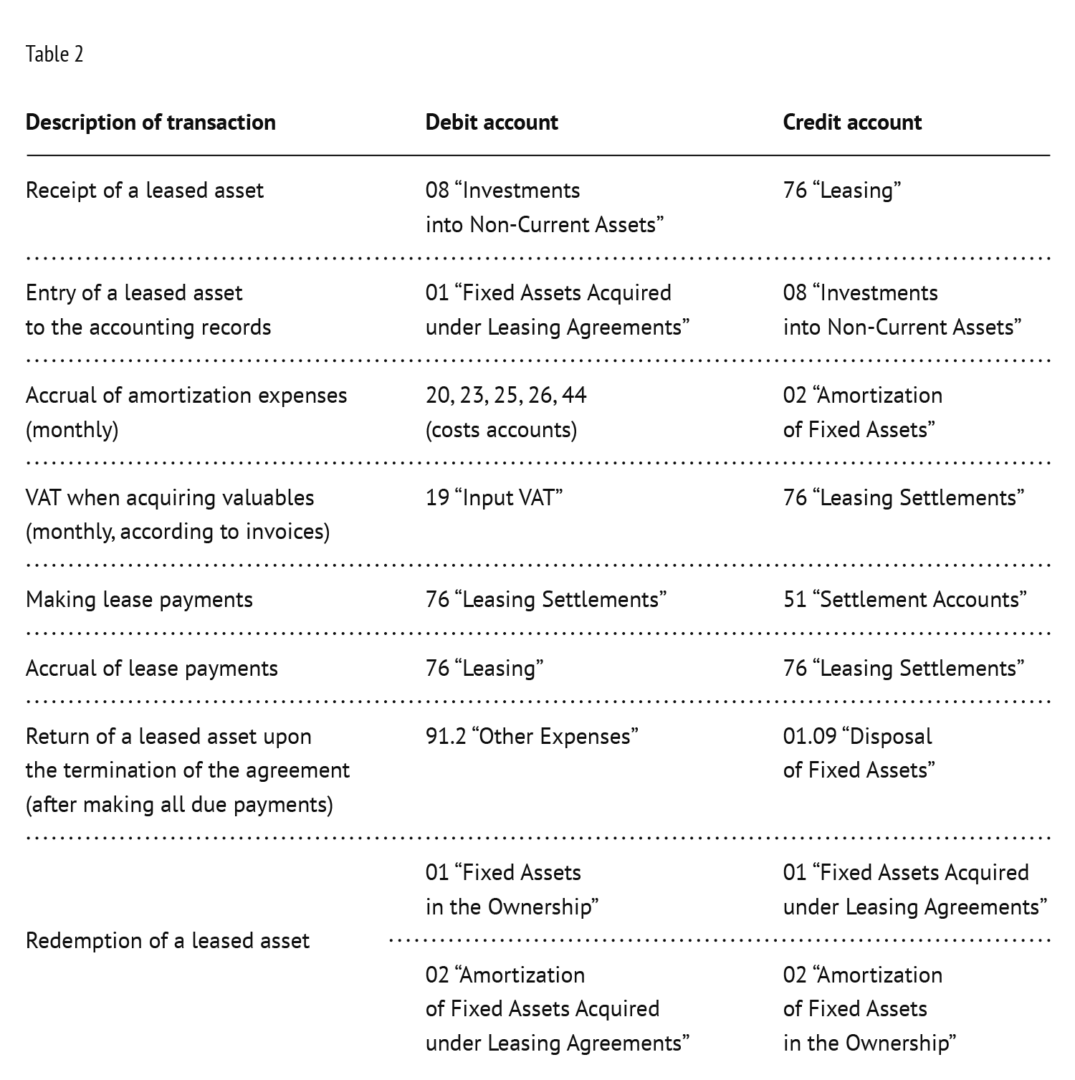

Balance sheet of the lessor

In this case, the buyer (lessee) cannot record a purchased car on the balance sheet accounts until the full redemption. The value of the leased property received by the lessee shall be recorded on off-balance sheet account 001 “Leased Fixed Assets” as in the case of an ordinary lease.

In accounting and tax accounting, the lessee shall record monthly lease payments and VAT deductible.

In case a leased asset is returned to the lessor (in practice, it is very rare), the asset is written off from off-balance sheet account 001 “Leased Fixed Assets” (see table 1).

In this case, tax accounting expenses coincide with accounting expenses, i. e. there are no differences (neither temporary nor permanent).

Balance sheet of the lease

If under the agreement a vehicle is recognized on the balance sheet of the lessee, accounting and tax accounting of such asset is carried out in different ways, i.e. there are some differences.

Accounting

Acquisition of a leased asset shall be reflected in the accounting records under the sale and purchase agreement.

The cost of the asset shall be determined as the sum of all expenses on the asset acquisition, namely, as the sum of all lease payments in total accruable under the schedule (term of the agreement)1.

Useful Life (UL) shall be determined on the basis of:

- The expected period of use (classification of fixed assets included in amortization groups is often used2);

- Regulatory and legal restrictions (e. g. leasing period);

- Expected physical depreciation;

- All write-off methods of amortization expenses specified in RAS 6/01 “Accounting of Fixed Assets” may be applied to leased assets. In practice, the straight-line amortization method is mostly applied (see table 2).

In order to separate objects in the ownership from those acquired under financial lease (leasing) agreements, the lessee is recommended to open additional sub-accounts to accounts 01 “Fixed Assets” and 02 “Amortization of Fixed Assets”.

Tax accounting

For the purposes of profit taxation (to determine the depreciation rate), the value of a leased asset is the amount of expenses of the LESSOR for the acquisition of a leased asset. Such value shall be specified in the agreement or annexes thereto. In practice, a copy of the sale and purchase agreement under which the lessor has acquired a leased asset is usually provided. Based on the above, the value in tax accounting is always lower than in accounting.

The useful life is determined in accordance with the classification of fixed assets included in amortization groups3.

The lessee has the right to provide for an increase in the multiplying factor not exceeding 3 for some assets, provided that the asset being acquired belongs to first-third amortization groups4.

In tax accounting, lease payments are recognized in the amount exceeding the amount of accrued amortization within the amount of lease payments stipulated by the agreement5.

Differences between accounting and tax accounting (RAS 18/02)

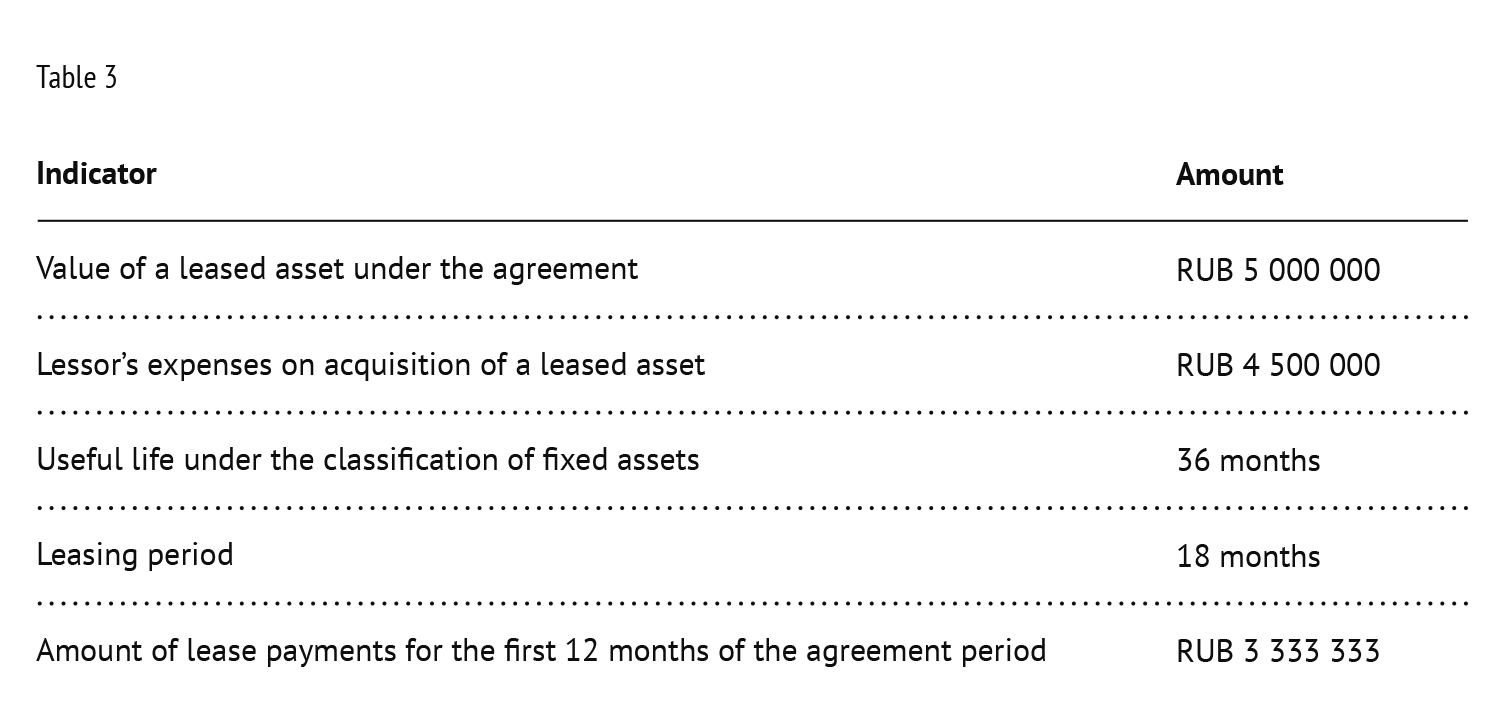

The procedure for the generation of differences between accounting and tax accounting is illustrated by the example of the acquisition of a vehicle under the following terms (see table 3).

In total, the lessee recognizes expenses in the amount of RUB 5,000,000 related to the acquisition of a vehicle under the financial lease (leasing) agreement in accounting (A) and tax accounting (TA). Differences arise only during the period of recognition and allocation of expenses between amortization and lease payments. Let us compare the amounts of expenses that will be recognized in the first 12 months of the leasing agreement with different accounting methods.

Option 1

The useful life of a leasing asset for accounting and tax accounting is the same in accordance with the classification of fixed assets included in amortization groups. The organization applies multiplying factor 3 to the depreciation rate (see table 4).

Monthly amortization in tax accounting exceeds the amount of monthly amortization in accounting. Since the reason is the different value of a leased asset in accounting and tax accounting, the difference is permanent. In the first year of ownership of a leased asset, a permanent tax asset (PTA) shall be formed in the account records.

Since multiplying factor 3 is applied to the depreciation rate, the actual amortization period in tax accounting shall amount to 12 months instead of 36 months. When amortization is no longer accrued in tax accounting, the difference will be reversed. In accounting, amortization will continue to be accrued, and there will be no amortization expenses in tax accounting, i. e. a permanent tax liability (PTL) will be formed.

In the current reporting period, the amount of amortization in tax accounting exceeds the amount of lease payments, so lease payments in the amount of RUB 500,000 may be recognized only in the following reporting period. Upon the recognition of lease payments in expenses, a permanent tax asset (PTA) is formed, because in accounting amortization expenses are recognized instead of lease payments.

Option 2

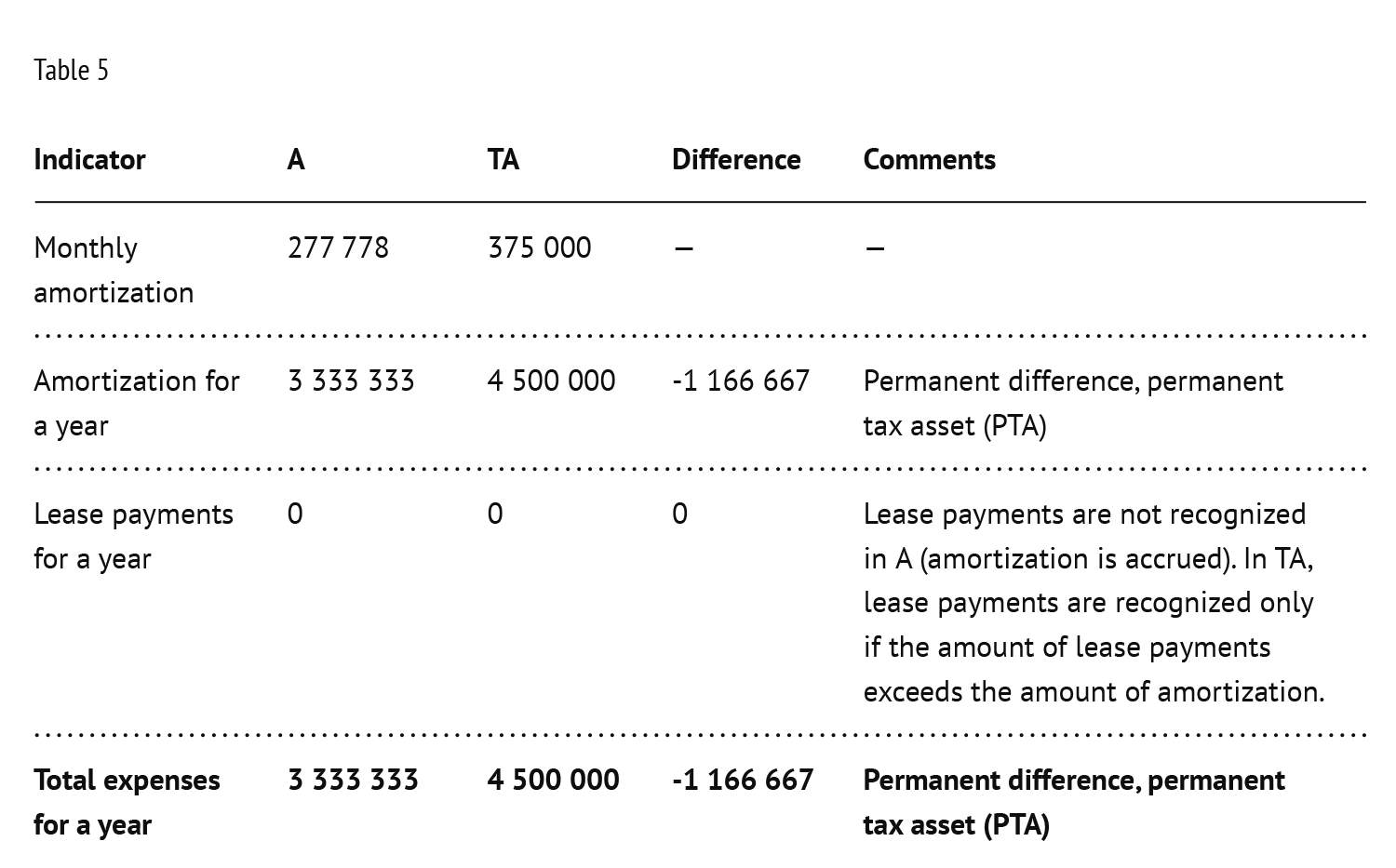

The useful life of a leased asset for accounting is set in accordance with the leasing period — 18 months, and for tax accounting purposes — in accordance with the classification of fixed assets included in amortization groups. The organization applies multiplying factor 3 to the depreciation rate (see table 5).

Amortization expenses for a year in tax accounting exceed amortization expenses for the leased asset in accounting; therefore, a permanent tax asset is formed.

Moreover, as in the first option, the actual amortization period in tax accounting shall amount to 12 months, while in accounting — 18 months. A year after the acquisition of the leased asset a permanent tax liability (PTL) will be formed instead of PTA.

In the current reporting period, the amount of amortization in tax accounting exceeds the amount of lease payments, so lease payments in the amount of RUB 500,000 may be recognized only in the following reporting period. A permanent tax asset (PTA) will be formed.

Option 3

The useful life of a leased asset for accounting is set in accordance with the leasing period, and for tax accounting purposes — in accordance with the classification of fixed assets included in amortization groups. The organization applies no multiplying factors (see table 6).

In this case, amortization expenses in accounting are more than two times higher than amortization expenses in tax accounting. A permanent tax liability (PTL) is formed. After the termination of the financial lease (leasing) agreement, the reverse difference and permanent tax asset (PTA) will be formed in accounting, since amortization expenses will be recognized in tax accounting for 36 months.

Since the amortization amount for the reporting period in tax accounting is less than the amount of lease payments for the same period, the lessee is entitled to recognize expenses on lease payments in excess of the amortization amount.

No procedure for recognition of lease payments in excess of accrued amortization is set in the tax legislation (lump sum or straight-line basis). Therefore, it is acceptable to recognize the entire difference in the amount of RUB 500,000 in one reporting period (within the excess of lease payments over accrued amortization). The lessee may decide to recognize lease payments on a straight-line basis during the leasing period. A permanent tax asset (PTA) is formed.

It should be noted that it is required to recognize lease payments in excess of the recognized amortization in tax accounting to minimize risks of disputes with tax authorities during the period of the financial lease agreement (leasing), but not after its termination.

Option 4

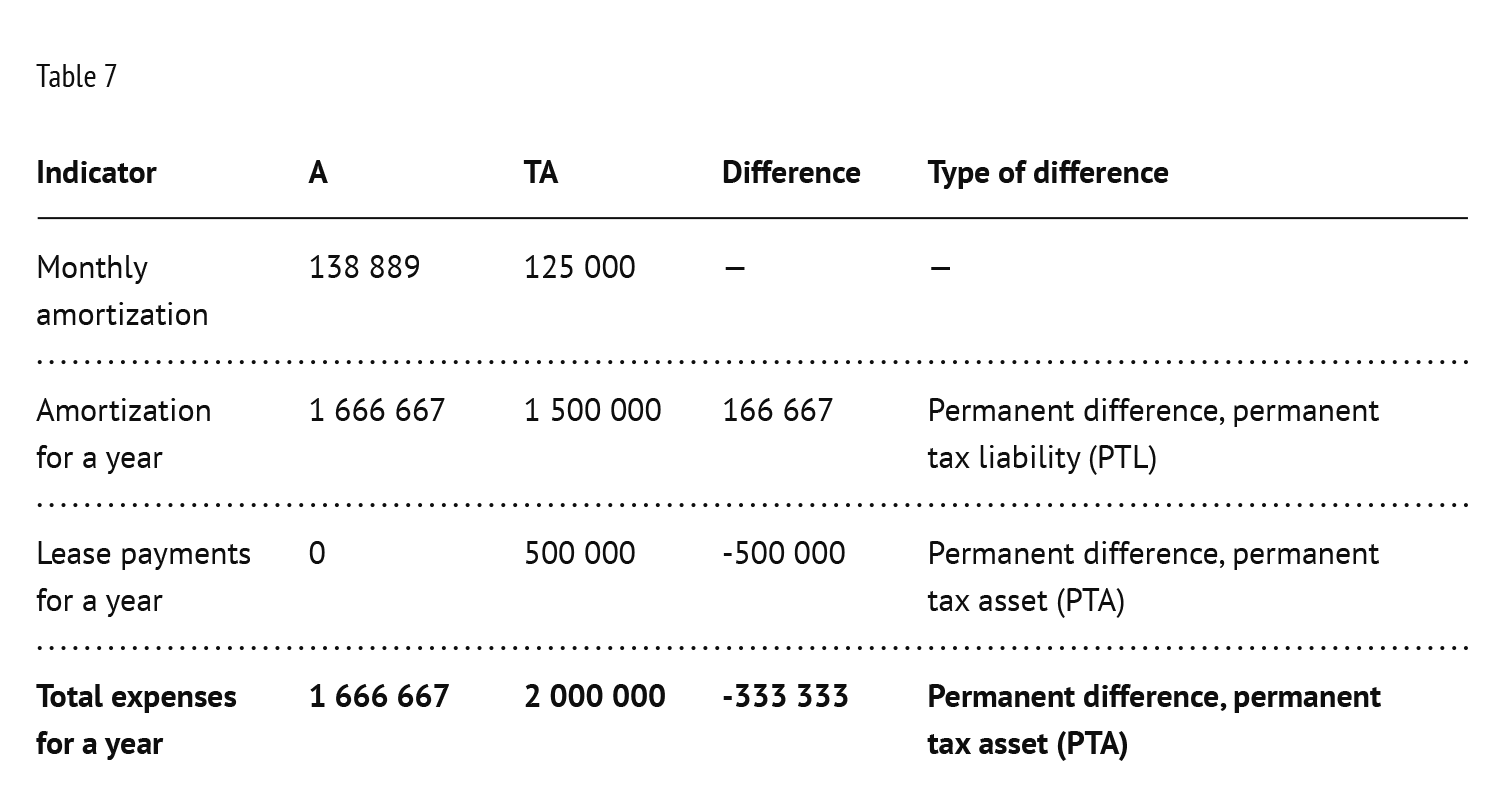

The useful life of a leased asset for accounting and tax accounting is the same in accordance with the classification of fixed assets included in amortization groups. The organization applies no multiplying factors (see table 7).

In this case, amortization expenses in accounting exceed amortization expenses in tax accounting. A permanent tax liability (PTL) is formed.

Since the amortization amount for the reporting period in tax accounting is less than the amount of lease payments for this period, the lessee is entitled to recognize expenses on lease payments in excess of the amortization amount. A permanent tax asset (PTA) is formed.

What is the difference?

By choosing one of the options above, the lessee may reduce the tax burden in the current and/or subsequent periods.

It is particularly important to make a preliminary calculation of the tax burden for all periods covered by the financial lease agreement (leasing) in case of significant investments in the acquisition of leased assets.

Redemption value

As a rule, financial lease (leasing) agreements provide for a minimum redemption value at the end of the leasing period.

Accounting

In the legislation on accounting, there are no instructions on the accounting of the redemption value of the leased asset.

Generally, the redemption value may be recognized as expenses on the acquisition of fixed assets and, accordingly, should determine the initial cost of the asset. However, if at the end of the leasing period the leased asset is returned to the lessor, the lessee will have to make adjustments to the accounting.

Tax accounting

In the Tax Code of the Russian Federation, there are no instructions on recognition of expenses in the form of the redemption value of the leased equipment.

According to the Ministry of Finance of the Russian Federation6, such expenses determine the initial cost of the depreciable property upon the transfer of ownership of the leased asset to the lessee.

If the redemption value exceeds RUB 100,000, the lessee should determine the initial cost of the fixed asset, set the useful life and recognize expenses by amortization accrual.

If the redemption value is less than RUB 100,000, expenses shall be recognized as a lump sum.

Advance under the financial lease agreement

If the financial lease (leasing) agreement provides for advance payments, such advance shall be recognized as expenses during the entire leasing period, but not as a lump sum upon its payment (distributed evenly throughout the entire leasing period).

VAT deductible from the amount of advance payment may be recognized, provided there is an invoice for advance payment. Upon recognition of expenses on lease payments, VAT on the advance payment is restored pro-rata to recognized expenses (to the extent of the distributed advance payment).

Things are about to change

For the purposes of accounting of leasing operations, Federal Standard of Accounting 25/2018 “Accounting of leasing” has been developed,

and since January 1, 2022, it shall terminate Order of the Ministry of Finance of the Russian Federation No. 15 dated 17.02.1997 “On Reflection of Operations under the Lease Agreement in Accounting” analyzed in this article.

- Clause 8 of the Russian Accounting Standard (RAS) 6/01 “Accounting of Fixed Assets”.

- Order No. 1 of the Government of the Russian Federation “On Classification of Fixed Assets Included in Amortization Groups” dated 01.01.2002.

- Clause 10 of Article 258 of the Tax Code of the Russian Federation.

- Sub-Clause 1 of Clause 2 of Article 259.3 of the Tax Code of the Russian Federation.

- Sub-Clause 10 of Article 264 of the Tax Code of the Russian Federation.

- Letter of the Ministry of Finance of the Russian Federation No. 03-03-06/1/4571dated January 28, 2019; Letter of the Ministry of Finance of the Russian Federation No. 03-03-06/2/79754 dated November 6, 2018; Letter of the Ministry of Finance of the Russian Federation No. 03-03-06/3/7617 dated February 12, 2016.

Other Articles on Topics