Since 2013, when the OECD published its report on combating corporate tax base erosion and profit shifting to low-tax jurisdictions, commonly known as the BEPS plan, we have repeatedly returned to issues associated with the implementation of the BEPS plan in the pages of “Korpus Prava.Analytics”. One of the topical subjects of the current year is the requirements of offshore jurisdictions for the organization of economic substance. In this article, we will try to answer the questions as to what it means, what is the reason for their introduction, whether they should be observed and what to do next.

Causes for the emergence of the economic substance concept

So, let us remember what the BEPS plan is actually aimed at. The BEPS plan combats non-taxation, which is achieved through moving profit centers away from production centers (the places where such profit is actually earned) and transferring the added value to low-tax or tax-free jurisdictions by legal and illegal means (as well as by abuse of the law). Such targeted actions of a taxpayer lead to the situation when profit calculated to determine the tax base is not formed in companies that have all prerequisites for profit generation. On the contrary, it is accumulated in other companies of the taxpayer which have neither assets nor resources necessary for profit-making and which often have nothing but instruments of incorporation. The BEPS plan is precisely aimed at combating such effects. According to the BEPS plan, fundamental changes are required for effective prevention of double non-taxation and also of cases of low taxation associated with the practice when taxable income is artificially separated from the activities that generate it.

The creators of the BEPS plan say that the use by taxpayers of double taxation agreements, aimed at providing mutual benefits to tax residents of these countries and enhancing interaction between the countries participating in it, has turned into the situation when taxpayers expand their opportunities by adding to that scheme shelf companies from third countries, which are not parties to double taxation agreements, but which, as the chain links, allow paying no taxes at all and thus abusing the provisions of the agreements. Countries that have entered into double taxation agreements cannot influence the legislation of such third countries since the latter has no contractual relations.

According to the creators of the BEPS plan, abuse of agreements is not advisable for several reasons, including the following:

- The benefits of the agreement agreed between the parties to it economically extend to residents of the third jurisdiction, although it is not a party to these agreements. Thus, the principle of reciprocity is violated and the balance of concessions that the parties make changes;

- Income may become completely tax-free or be subjected to inadequate taxation, which is far from the way the parties to the agreement intended to;

- Residence jurisdiction of the ultimate beneficiary has fewer incentives to conclude a tax agreement with the jurisdiction of the source of income since residents of the beneficiary’s residence jurisdiction may indirectly receive benefits from the jurisdiction of the source of income without the need of the beneficiary’s residence jurisdiction to ensure mutual benefits.

Therefore, the OECD has repeatedly explained in the BEPS plan and other documents that it is necessary to supplement the existing standards designed to prevent double taxation with tools that prevent double taxation in areas not previously covered by international standards and which address cases of non-taxation associated with the practice when taxable income is artificially separated from the activities that generate it as well as the fact that international means of putting pressure on third countries and international mechanisms that would limit the abuse of agreements and the ability of taxpayers to separate profit from the places where it arises must be developed.

Since 2013, the OECD has succeeded in implementing its plan and objectives, which has been repeatedly stated in reports that can be found on the organization’s website. Automatic information exchange has been introduced, requirements for controlled foreign companies have been strengthened, control over transfer prices has been tightened, conduit schemes have been restricted, certain preferential tax regimes have been abolished. The pressure is being put on jurisdictions by virtue of including the countries that provide low-tax regimes into blacklists, restrictions on transactions with them. In addition, the OECD has made the banks and other financial institutions that also actively contribute to the implementation of the BEPS plan both its allies and hostages.

The substance concept became one of such steps. Declaring the need to limit abuse of agreements and profit shifting, the OECD first used the term shelf company meaning a company that has few or no signs of actual existence (actual presence) in the sense of the company having office space, material assets and employees.

Through the provisions of the BEPS plan, particularly through implementing step 6 Prevention of Abuse of Tax Agreements, the OECD has declared war on the companies and schemes in which they are used. Through changes in national legislation and introduction of the concept of actual income recipient as it happened, for example, in Russia, through banks and their refusals to open accounts for companies without the minimum actual presence, the possibilities of using shelf companies have become largely limited. The next major victory on the path of the OECD in combating shelf companies was the implementation of the idea to introduce requirements for economic substance in tax-free jurisdictions.

The essence of economic substance

Economic substance is the minimum set of requirements established by national legislation that a company should meet in order for the country to perceive it as actually existing in its jurisdiction if such company plans to maintain its tax residence in that jurisdiction.

It has already been noted above that a shelf company is a company with a lack of office space, material assets and employees. On this basis, the minimum amount of requirements for economic substance has been formed (fig. 1):

- The company director should be local;

- The company should have employees, whose qualifications should be in line with the activities of the company and who should be local;

- The company has local expenses;

- The company has an office sufficient to carry out profit-generating activities;

- The company carries out activities generating profit in the jurisdiction.

This means that companies registered in the territory, where economic substance legislation is adopted, are required, if they acknowledge their status of a tax resident of such country, to either provide evidence of compliance with the requirements of the legislation or confirm that they are tax residents of another country. In practice, this means that now taxpayers using companies registered in countries that have implemented economic substance legislation are required either to make the company actual and, most importantly, to start carrying out profit-generating activities through it or voluntarily acknowledge their status of a tax resident of another country, that is, start paying taxes in such other country.

Thus, the introduction of economic substance legislation basically became the final logical step on the path of the OECD in combating artificial separation of taxable income from the activities that generate it.

Key elements of economic substance

At the end of 2018, economic substance legislation was adopted by the British Virgin Islands (as of today, BVI even published draft economic substance code), Belize, the Cayman Islands, Mauritius, the Bahamas, the Seychelles, the Islands of Bermuda, the English Channel islands of Guernsey and Jersey, the Isle of Man. This list continues to be updated. Basically, low-tax jurisdictions are forced to adopt such legislation since this is a condition for exclusion of such jurisdictions from the list of countries that do not interact and exchange information on tax issues or otherwise simplifies the interaction of companies from these jurisdictions with the outside world. One of the latest countries to speak about adopting economic substance so far is the UAE. On April 30, 2019, the UAE Government issued the resolution introducing the relevant regulation. Jurisdictions such as St. Vincent and the Grenadines, the Antilles and others also discuss the possibility of changing their legislation to meet the requirements of the EU.

In general, regulatory acts of different countries concerning economic substance are similar to each other. The provisions differ in terms of timing of the introduction, consequences of violation of the legislation, requirements concerning the substance elements which should be observed.

As for the types of activities of the company for which economic substance should be confirmed, all jurisdictions look to the list of the relevant types of activities recommended by the OECD with rare exceptions. These activities include:

- Banking business;

- Insurance business;

- Fund management activities;

- Financing and leasing;

- Activities as a parent organization;

- Shipping business;

- Holding activities;

- Activities in profit-making from intellectual property;

- Activities of distribution and service centres.

Such a list was used in the BVI, the Cayman Islands, the Islands of Bermuda, the Bahamas, the UAE and in other jurisdictions. Exceptions are found, for example, in legislative regulations of the Seychelles or Mauritius where the requirements apply only to licensed financial institutions so far (in Mauritius, the substance requirements apply to companies with the Global Business Licensed Company status, in Seychelles — to almost all licensed players on the securities market including activities of investment advisers and portfolio managers). Then, the legislative regulations clarify which specific actions are recognized as relevant (principal types of activities that generate profit). Thus, for instance, ownership of a yacht used for personal purposes is not a relevant activity as well as granting interest-free loans since no receipt of income is stipulated for that matter.

The list of substance elements that a company with relevant activities should have is also unified across almost all jurisdictions. As noted above, the key elements of economic substance are:

- The actual implementation of profit-generating activities;

- Place of effective management;

- Current local expenses;

- Office rental;

Full-time employees, whose qualification is in line with the company’s activities.

The requirement concerning profit-earning at the company’s place of residence is common to all jurisdictions and fundamental to the concept of the BEPS plan. Other elements are combined. For example, in the BVI, the conditions for holding companies are relaxed. The companies are only required to confirm the existence of their employees and office. Companies with other relevant activities are required to have all elements except assets. However, assets (equipment) are required when it comes to managing intellectual property, the use of which involves the use of equipment. Legislative regulations of Guernsey and the UAE contain all the abovementioned elements as well as requirements concerning the existence of assets; preferential requirements for substance (office and employees) are stipulated for the UAE holding companies, and for high-risk IP companies additional criteria to comply with are established. In Belize, it is required to confirm the existence of employees, expenses and management. In Seychelles, the key elements are employees and expenses. In Mauritius, additional requirements concerning the number of local expenses to be incurred, are established.

Then, the legislative regulations establish the time limits, within which the companies should comply with the economic substance requirements and provide the evidence to authorized persons and liability for the violation of these requirements. The time limits mainly depend on whether the company is new or old, but in any case, the deadline for substance confirmation is the end of 2020.

The liability for violation is different: denial of registration, denial of applying preferential tax treatment, warning, demand for an audit, fines ranging from tens to hundreds of thousands of US dollars and even imprisonment. Despite the fact that the extent of liability looks impressive, the issue of bringing to liability remains open as in any case accountability measures would apply to a company through its directors. In most companies, directors are provided by administrative providers (registration agents), part of which are located in these jurisdictions and the other part — in other countries. The matter of applying a fine to a company with its director and account located in the third country is not idle, especially the matter of applying a fine to a director provided by a registration agent who would say at the earliest moment that he/she is not the director. In these circumstances, in practice, non-compliance with the economic substance requirements will, most likely, result in directors, secretaries and shareholders of shelf companies resigning from their positions (including unilaterally through court action), and the companies becoming uncontrollable.

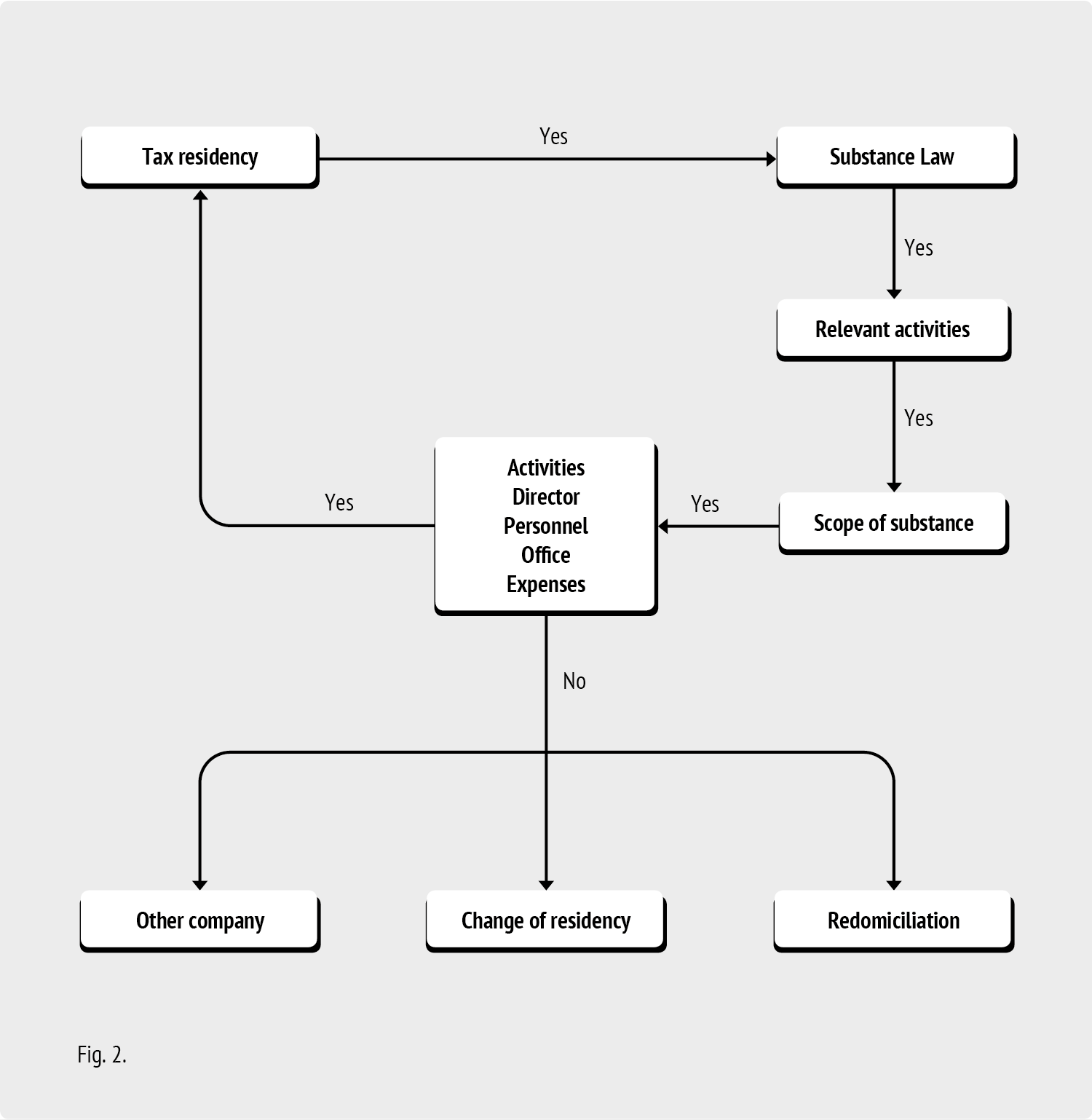

Test for compliance

Given widespread dissemination of economic substance legislation, considerable fines imposed for its violation, clarifications that have appeared, elaborated reporting forms, requirements for the organization of economic substance seem no longer phantom. They are more than real. In this regard, all companies registered in classic offshore jurisdictions should pass the test for compliance with the requirements for the organization of economic substance. In passing this test, it is necessary to ask yourself the following questions (fig. 2):

- Are you planning to identify the company as a tax resident in this jurisdiction?

- If yes, has the jurisdiction adopted economic substance legislation?

- If yes, are the company’s activities (key activities aimed at generation of profit) associated with the relevant activities specified in the legislation?

- If yes, which substance level is required for these activities?

- If yes, are you planning to carry out actual management and control in this jurisdiction?

- If yes, are other elements of substance, the set of which depends on the relevant activities, complied with?

- Employees;

- Address;

- Expenses;

- Other.

If any requirement mentioned above is not and cannot be complied with, you need to think about changes in the structure of the company, its management, and functionality, or about the need to take more radical measures, such as change of tax residence, redomiciliation of the company or transfer of assets/activities to other companies of the group. In any case, the issue should be resolved in view of the analysis of expenses that the company has to incur to comply with all requirements and benefits that the taxpayer using an offshore company will eventually receive. Moreover, it is also important to take into account requirements of legislation concerning CFCs, actual income recipients, standards concerning automatic disclosure of information and other provisions of regulations that can and should affect the choice of the taxpayer when assessing the cost-effectiveness of substance. It is no longer possible to remain a silent observer of this problem; there is also no use to look for ways to circumvent the direct requirement of the legislation. This is the case when the only way to not comply with the law is to not fall within it, that is, to change the company, jurisdiction or tax residency. Otherwise, you can lose if not the assets, then at least access to them.

Other Articles on Topics